ETF Creation Fees: The Hidden Costs Investors Miss

ETF creation fees, bid-ask spreads, and premiums can quietly erode returns. Here is a clear breakdown of every cost layer Singapore ETF investors should understand.

TL;DR: Exchange Traded Funds (ETFs) are widely praised for their low costs, but several fees beyond the headline expense ratio can quietly erode your returns. Understanding ETF creation fees, bid-ask spreads, and the role of authorised participants may be useful in helping you make cost-aware investment decisions.

When evaluating an ETF, most investors look at one number: the expense ratio. It is clean, easy to compare, and sits right at the top of the fund factsheet. However, the total cost of owning an ETF can extend beyond that single figure. ETF creation fees, redemption charges, bid-ask spreads, and premiums or discounts to net asset value (NAV) can all affect your actual returns. For Singapore-based investors accessing markets in the US, Hong Kong, and locally, understanding these costs can help investors understand ETF cost structures for building a cost-efficient portfolio.

How the ETF Creation and Redemption Process Works

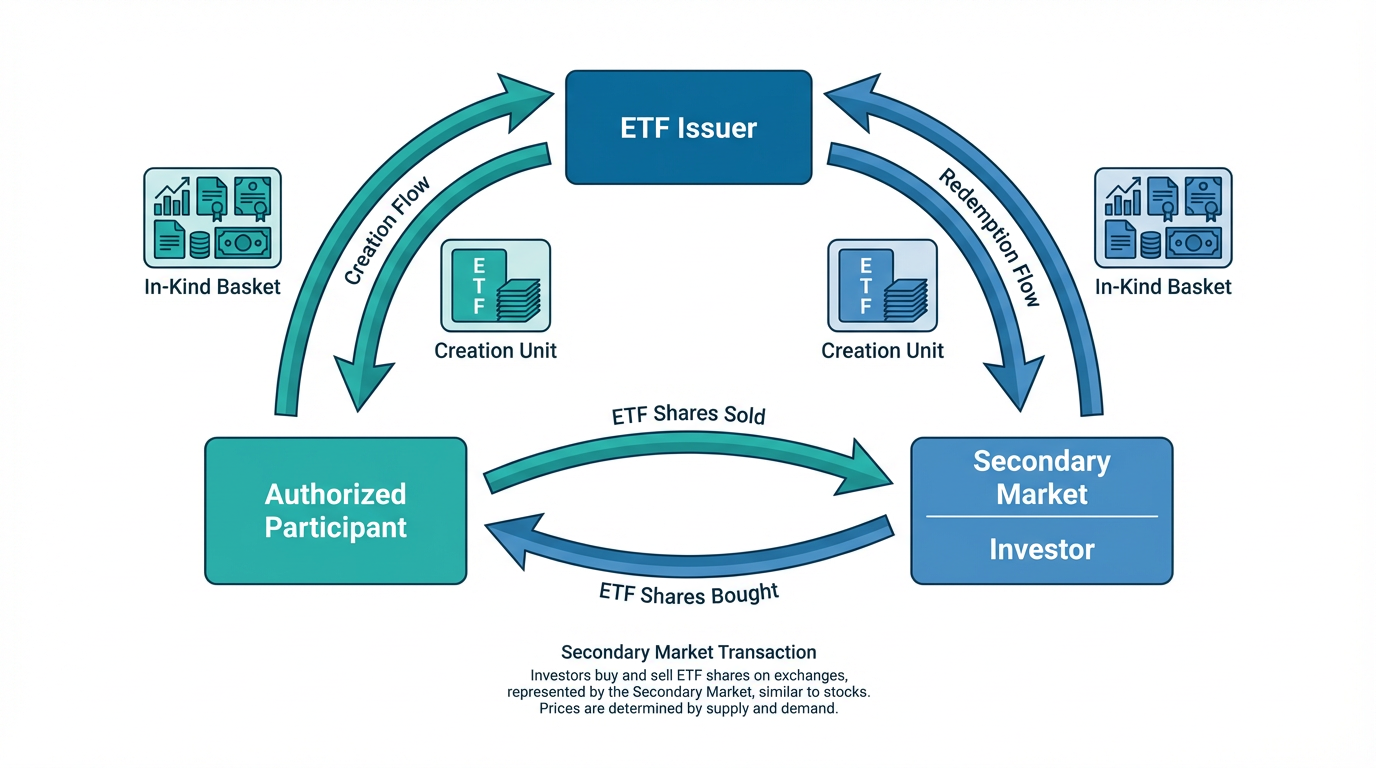

Before unpacking the fees, it helps to understand the mechanism behind ETF share supply. Unlike individual stocks or unit trusts, ETFs use a unique system to keep their market price closely aligned with the value of their underlying holdings.

The Role of Authorised Participants

Authorised Participants (APs) are large financial institutions, typically major banks or broker-dealers, that have formal agreements with ETF issuers. They are the only parties who can create or redeem ETF shares directly at the fund level, in large batches called creation units, which typically represent between 25,000 and 200,000 shares per unit, according to the Investment Company Institute.

When an ETF's market price rises above NAV, an AP assembles the underlying securities, delivers them to the ETF issuer, and receives a creation unit in return. Those shares are then sold on the secondary market, pushing the price back toward NAV. The reverse happens when the price falls below NAV. This arbitrage keeps ETF prices efficient, but it also comes with fees.

In-Kind vs. Cash Creation

Most ETF creation is done in-kind: APs deliver the actual underlying securities rather than cash. This is more cost-efficient and preserves the ETF's tax efficiency, since the fund avoids selling holdings to accommodate flows. Cash creation is also permitted, particularly for fixed-income ETFs or during volatile markets, but it requires the fund to purchase the underlying securities itself, generating additional transaction costs that are typically passed on via the creation fee.

Understanding ETF Creation Fees

ETF creation fees are charges levied by the ETF issuer on APs when creation units are established or redeemed. These fees can range from approximately 0.01% to as high as 3.00% depending on the fund's asset class, basket complexity, and whether the transaction is in-kind or cash-based.

Fixed vs. Variable Creation Fees

Creation fees typically come in two forms:

-

Fixed fees: A flat per-transaction charge applied to every creation or redemption event, regardless of transaction size.

-

Variable fees: A percentage-based charge that may apply for larger transactions, particularly those above a stated asset threshold. Some fund managers waive variable fees entirely until a fund surpasses USD 50 million in assets under management.

For cash-based creation specifically, fees tend to run higher because the fund must execute trades on behalf of the AP. A low-turnover index ETF might have an expense ratio of 0.04%, while a single cash creation event could add a transaction fee of 0.12% to 0.15%, in some cases.

Do Creation Fees Affect Retail Investors?

Retail investors do not pay ETF creation fees directly. You are not an AP; when you buy ETF shares on a stock exchange, you are purchasing them on the secondary market from other investors, not from the fund issuer.

However, creation fees can affect you indirectly. If creation and redemption costs are high, APs factor this into their pricing, which can widen the bid-ask spread you see when you trade. Higher operational costs at the fund level may also be reflected in the overall expense ratio over time.

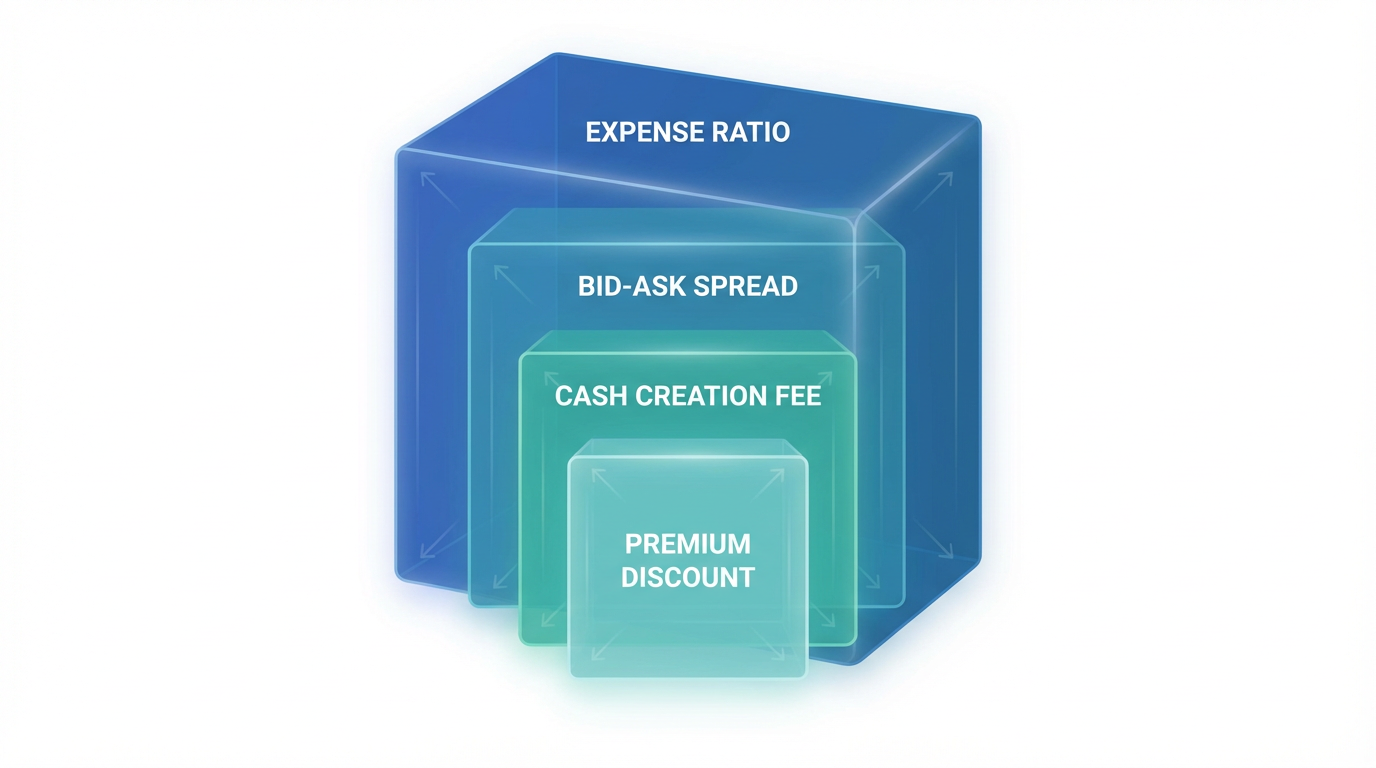

The Fees That Do Affect You Directly

While creation unit fees are primarily an institutional concern, several costs directly impact every ETF investor.

The Expense Ratio

The expense ratio, also known as the Total Expense Ratio (TER) or Operating Expense Ratio (OER), is the annual fee charged by the fund to cover management and administrative costs. It is deducted daily from the fund's assets and reflected in your net returns rather than charged as a separate bill.

As of 2025, index equity ETFs average approximately 0.14% in expense ratios and index bond ETFs around 0.09%, according to the Investment Company Institute. For example, for every USD 10,000 invested, a 0.20% expense ratio costs USD 20 per year.

Tip: The expense ratio compounds over time. A 0.5% annual difference on a USD 100,000 portfolio can reduce accumulated value by roughly USD 20,000 over 20 years, based on a hypothetical 4% annual return scenario.

Bid-Ask Spreads

The bid-ask spread is the difference between what a buyer will pay (the bid) and what a seller will accept (the ask). This cost is invisible on your brokerage statement but embedded in every trade you execute.

Highly liquid ETFs tracking major US indices often have spreads below 0.01%, while niche thematic ETFs can carry spreads of several basis points or more. For short-term traders, the bid-ask spread may matter more than the expense ratio. To keep this cost low, some investors may use limit orders to manage execution price uncertainty during the opening and closing minutes of the session when spreads typically tend to widen.

Premium and Discount to NAV

ETFs can trade above (at a premium) or below (at a discount) their NAV during the trading day. Buying at a premium means paying more than the underlying assets are worth; selling at a discount means receiving less. The AP arbitrage mechanism keeps these differences small for most liquid ETFs, but premiums and discounts can widen during market stress or for funds tracking less accessible underlying markets.

You can check premium and discount data on ETF providers' websites or through market data platforms. Longbridge's market data service allows you to track live ETF prices and monitor trading conditions in real time.

Brokerage Commissions

The commission charged by your broker is a separate, direct cost. For investors making small, frequent investments, commissions can represent a meaningful proportion of each transaction. Reviewing your platform's pricing before establishing a regular investment programme is a practical step. You can review Longbridge's pricing page for the fee structure across Singapore, US, and Hong Kong markets.

How These Costs Add Up: A Practical Perspective

Consider a Singapore investor who regularly allocates funds to a US-listed ETF. Each purchase involves a brokerage commission, the bid-ask spread at execution, and the ongoing expense ratio. For a less liquid ETF using market orders, combined transaction costs may exceed the advertised expense ratio on that particular trade.

For long-term investors, the expense ratio carries the most weight as it compounds over time. For active traders, the bid-ask spread is often the dominant cost. Understanding your own investment behaviour helps you prioritise which fees matter most.

Tip: When comparing two ETFs tracking the same index, look beyond the expense ratio. Factor in average trading volume, the typical bid-ask spread, and whether the fund tends to trade near its NAV.

ETFs vs. Other Investment Structures

ETFs generally carry lower ongoing costs than unit trusts (mutual funds) in Singapore. A unit trust's total expense ratio often ranges from 0.50% to 1.50% or higher, and many carry sales charges of up to 5% at the point of purchase. That said, tax treatment differences exist between ETF structures, and Singapore investors holding US-domiciled ETFs should be aware that US estate tax applies to assets above a USD 60,000 threshold, which can affect the true total cost of ownership.

Note: This article is for general educational purposes only and does not constitute financial or tax advice. Consult a qualified professional for guidance specific to your situation.

The Longbridge products overview page covers the full range of asset classes accessible to Singapore investors on the platform.

Frequently Asked Questions

What is a creation unit in an ETF?

A creation unit is a large block of ETF shares, typically between 25,000 and 200,000 shares, that can only be created or redeemed directly with the ETF issuer by authorised participants. Retail investors cannot access the primary creation or redemption process and instead trade ETF shares on the secondary market through a stock exchange.

Do ETF creation fees apply to regular investors?

Not directly. Creation fees are charged to authorised participants. However, these fees can indirectly affect retail investors by influencing bid-ask spreads and, over time, the ETF's overall cost structure.

What is the difference between an expense ratio and a creation fee?

The expense ratio is an annual fee charged by the fund to all investors for management and operational costs, deducted daily from fund assets. A creation fee is a one-time transaction charge levied on authorised participants when they create or redeem large blocks of ETF shares at the fund level.

How can I reduce the total cost of owning an ETF?

ETF ownership costs can be influenced by factors such as expense ratios, trading liquidity, and how closely an ETF’s market price tracks its net asset value (NAV). Trading costs may also vary depending on order type and the fee structure of the chosen brokerage.

Are ETFs still cost-effective despite these fees?

For most long-term investors, yes. Even accounting for bid-ask spreads and commissions, ETFs generally remain more cost-efficient than actively managed unit trusts. The key is awareness of the full cost picture, not just the headline expense ratio.

Conclusion

ETFs offer genuine cost advantages for investors seeking diversified market exposure. However, the complete fee picture extends beyond the expense ratio. ETF creation fees shape the behind-the-scenes economics that keep fund prices efficient; bid-ask spreads represent a real cost at every trade; and premiums, discounts, and brokerage commissions all contribute to your total cost of ownership.

For Singapore investors, building awareness of these layered costs allows for more informed fund selection and portfolio management over the long term. Whether you are exploring ETFs available on Longbridge or comparing investment structures, a clear understanding of how fees work at every level of the ETF ecosystem supports informed decision-making.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.