Currency-Hedged ETFs: A Guide to Managing FX Risk

Currency-hedged ETFs shield international investments from exchange rate fluctuations using forward contracts. Learn when hedging makes sense for your portfolio.

TL;DR: Currency-hedged ETFs use forward contracts to neutralise foreign exchange fluctuations, letting you capture the pure return of international assets without currency volatility. They work well for short-term investors or during high FX volatility, but the added costs may erode gains over longer holding periods.

When you invest in international markets, your returns depend on two factors: how your chosen assets perform, and how exchange rates move. A Singapore investor buying US stocks, for example, faces both the ups and downs of American equities and the fluctuations between the Singapore dollar and US dollar. Currency-hedged Exchange-Traded Funds (ETFs) address the second variable by stripping out exchange rate movements, so your results reflect the underlying investment rather than currency swings.

For investors with exposure to Singapore, US, and Hong Kong markets, understanding when currency hedging adds value is an essential part of building a resilient portfolio. This guide explains how currency-hedged ETFs work, what they cost, and how to decide whether they fit your investment approach.

What Is a Currency-Hedged ETF?

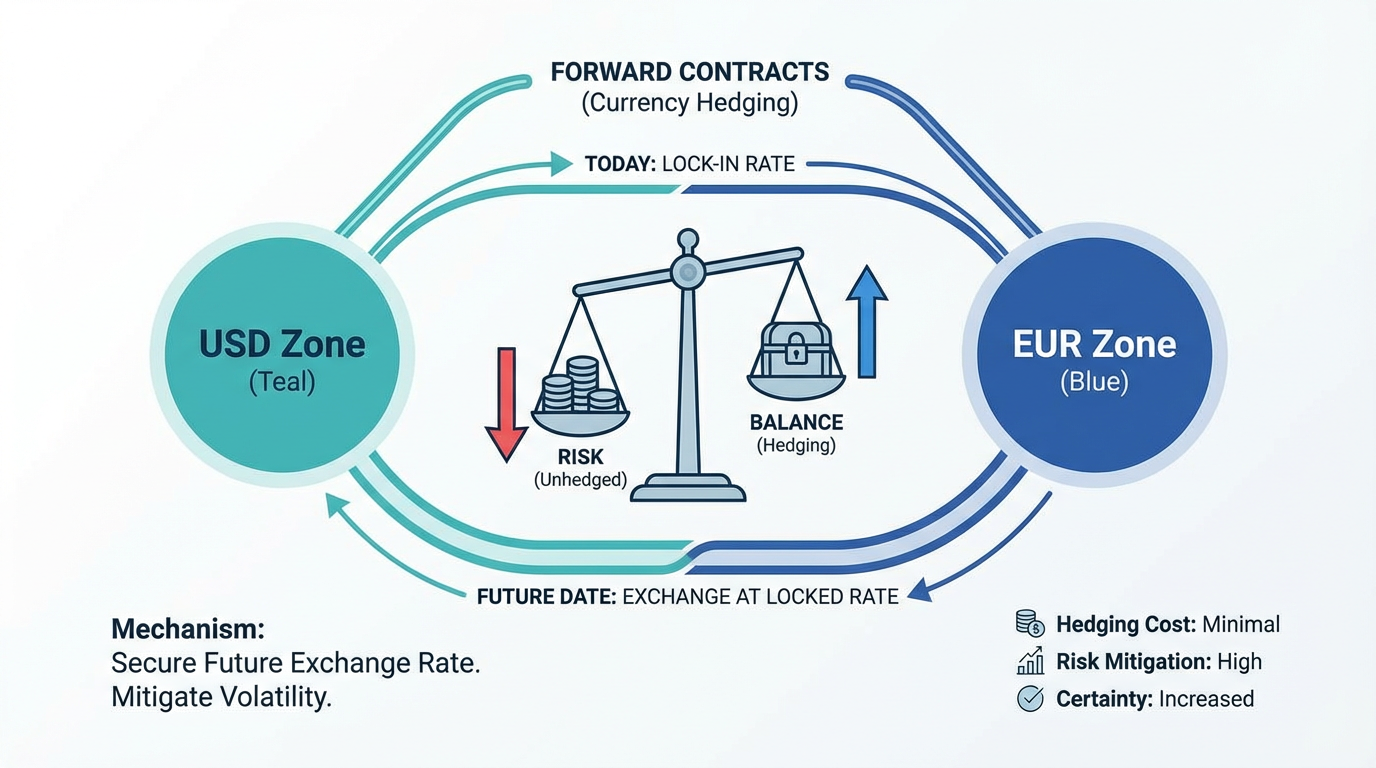

A currency-hedged ETF holds the same underlying assets as its unhedged counterpart but adds a layer of foreign exchange (FX) protection. The fund manager enters into forward contracts that lock in exchange rates for a set period, typically one month. These contracts are then rolled forward at each month's end.

Here is how the protection works:

-

If your home currency strengthens against the foreign currency, your international holdings lose value when converted back. The forward contracts gain value to offset this loss.

-

If your home currency weakens, your international holdings gain value on conversion. The forward contracts lose value, cancelling out that currency-driven gain.

The net effect is a smoother return profile. You capture the performance of the underlying index, sector, or asset class without the added volatility from exchange rate movements.

Static vs Dynamic Hedging

Not all hedged ETFs operate the same way. There are two main approaches:

Static hedging maintains a consistent hedge regardless of market conditions. The fund continuously holds forward contracts that cover 100% (or a fixed percentage) of the foreign currency exposure. This is the most common approach and provides predictable protection.

Dynamic hedging adjusts the hedge based on market signals. The fund manager, or an algorithm, determines when to increase or decrease the hedge ratio. This approach attempts to capture some currency upside while still providing downside protection, though it introduces additional complexity and potential tracking error.

How Currency-Hedged ETFs Work

The mechanics of currency hedging rely on forward contracts in the foreign exchange market. A forward contract is an agreement to exchange a specific amount of one currency for another at a predetermined rate on a future date.

The Monthly Rebalancing Process

Most currency-hedged ETFs follow a monthly cycle:

-

At the start of each month, the fund calculates its foreign currency exposure based on the value of its holdings.

-

The manager enters forward contracts to sell the foreign currency and buy the base currency at a locked-in rate.

-

At month's end, these contracts settle, and new contracts are established for the following month.

This process introduces a concept called the "cost of carry," which is primarily driven by interest rate differentials between the two currencies. When you hedge from a low-interest-rate currency into a higher-interest-rate currency, the forward contracts create a drag on returns. Conversely, hedging from a high-rate currency into a lower-rate currency can generate a small positive carry.

Hedge Ratios Explained

The hedge ratio refers to what percentage of foreign currency exposure the ETF covers:

-

100% hedge ratio: The fund attempts to eliminate all currency exposure. This is the most common approach for straightforward currency-hedged ETFs.

-

Partial hedge ratio (such as 80%): The fund hedges most of the exposure but allows some currency movement to affect returns. This reduces hedging costs while still providing substantial protection.

The Cost of Currency Hedging

Currency hedging is not free. Understanding the costs helps you evaluate whether hedging makes sense for your situation.

Expense Ratio Differences

Currency-hedged ETFs typically carry higher expense ratios than their unhedged equivalents. Hedged ETFs may cost an estimated 0.1% to 0.3% more per year in expense ratios. This covers the administrative costs of managing the forward contracts and any fees associated with developing the hedging strategy.

Interest Rate Differentials

The larger cost factor is often the interest rate differential between currencies. When hedging from a currency with low interest rates into one with higher rates, the forward contracts trade at a discount, creating a "negative carry." This can add meaningful drag over time.

For example, a Singapore investor hedging USD exposure would face costs influenced by the difference between Singapore and US interest rates. When US rates are substantially higher, the cost of hedging increases.

Total Cost Considerations

According to UBS research, hedged ETFs add roughly 0.10% in expense and forward-roll costs that can erode long-term gains. While this seems modest, the cumulative effect over a decade or more can be significant, particularly during periods of large interest rate differentials.

Tip: Before selecting a hedged ETF, review the fund's total expense ratio and consider the current interest rate environment between your home currency and the foreign currency you are hedging against.

When to Consider Currency-Hedged ETFs

The decision to hedge depends on your investment horizon, risk tolerance, and market outlook.

Short-Term Investors

If you have a time horizon of less than two years, currency-hedged ETFs often make sense. Currency swings can be substantial over short periods and may overwhelm the returns from your underlying investments. Hedging smooths out this volatility and provides more predictable outcomes.

High Volatility Periods

When currency market volatility is elevated, hedging can help reduce the impact of sudden exchange rate swings on your investments. During such periods, evaluating currency-hedged options may provide more stable outcomes, particularly for investors who are sensitive to short-term fluctuations. You can track market performance and volatility indicators to monitor these conditions.

Fixed Income and Stability-Focused Portfolios

Hedged share classes are particularly popular within fixed income investments. Hedged share classes have seen significant adoption, particularly in fixed income and commodity ETFs. The rationale is straightforward: when the underlying asset offers modest, stable returns, currency fluctuations can easily overwhelm those returns. Hedging preserves the stability investors sought in the first place.

Long-Term Investors: A Different Calculation

For investors with horizons of five years or more, the case for hedging is less clear. Research from Morningstar suggests that over extended periods, the benefits of hedging versus not hedging tend to balance out. Currencies do not move in one direction permanently; upswings and downswings often cancel each other.

Additionally, the cumulative cost of hedging compounds over long periods. A 0.2% annual drag may seem small, but over 20 years, it meaningfully reduces your portfolio value.

Key Selection Criteria for Hedged ETFs

When evaluating currency-hedged ETFs, focus on four primary metrics:

Expense Ratio

Compare the expense ratio of the hedged version to its unhedged counterpart. The smaller the differential, the more cost-effective the hedging. Consider choosing funds where the additional cost of hedging is relatively low compared with similar options.

Hedge Ratio

Understand whether the ETF employs full (100%) or partial hedging. Full hedging eliminates more currency risk but may cost more. Partial hedging (such as 80%) reduces costs while still providing substantial protection.

Tracking Error

Review how closely the hedged ETF follows its target index. Currency hedging can introduce tracking error due to rebalancing timing and basis risk.

Liquidity

Ensure the ETF has sufficient trading volume. More liquid ETFs have tighter bid-ask spreads, reducing transaction costs.

Blended Approaches to Currency Exposure

You do not need to choose exclusively between hedged and unhedged investments. More sophisticated investors may adopt a blended approach, hedging a portion of their foreign exposure while leaving the rest unhedged.

J.P. Morgan Personal Investing notes that their portfolios hedge approximately 30% of foreign equity exposure, adjusting based on market outlook. This captures some potential currency gains while providing a buffer against sharp adverse moves.

Consider hedging differently across asset classes. Fixed income investments, where returns are more modest and predictable, often benefit more from hedging. Equities, with their higher volatility and return potential, may warrant less hedging to avoid cost drag.

Frequently Asked Questions

What is the main purpose of a currency-hedged ETF?

A currency-hedged ETF delivers the performance of foreign assets without volatility from exchange rate movements. It uses forward contracts to neutralise currency fluctuations, letting investors capture the pure return of the underlying index.

Do currency-hedged ETFs eliminate all currency risk?

Not entirely. Factors like basis risk and rebalancing timing can create small residual currency effects. A fully hedged ETF may still experience minor tracking differences due to these technical factors.

When should I choose a hedged ETF over an unhedged one?

Hedged ETFs suit investors with shorter time horizons (under two years), those seeking stability in fixed income allocations, or those investing during elevated currency volatility. Long-term equity investors may find the hedging costs outweigh the benefits.

How do interest rate differentials affect hedging costs?

When your home currency has lower interest rates than the foreign currency you are hedging, forward contracts trade at a discount, creating a cost. The wider the interest rate gap, the higher the hedging cost.

Can I hedge currency risk without using hedged ETFs?

Yes, through currency futures or options. However, this requires more active management and may involve higher transaction costs for smaller portfolios. For most retail investors, currency-hedged ETFs offer a simpler solution.

Conclusion

Currency-hedged ETFs provide a practical tool for managing foreign exchange risk in international investments. They use forward contracts to neutralise currency movements, delivering smoother returns that reflect the underlying assets rather than exchange rate swings.

The key trade-off is cost. Hedged ETFs carry higher expense ratios and may face interest rate-driven drag over extended periods. For short-term investors or those focused on fixed income stability, this cost is often worthwhile. Long-term equity investors may find the cumulative expense reduces the benefit.

Consider your investment horizon and tolerance for currency volatility when deciding between hedged and unhedged options. A blended approach offers a middle path that balances cost control with risk management.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.