ETF Portfolio Rebalancing: How to Maintain Your Target Allocation

Portfolio drift can silently increase your investment risk. Learn the essentialstrategies to rebalance your ETF holdings and maintain your target allocation effectively.

TL;DR: ETF portfolio rebalancing involves adjusting your holdings to maintain your target asset allocation. Regular rebalancing helps manage risk, prevents portfolio drift, and may help support long-term portfolio management by systematically selling high and buying low.

When you first build an investment portfolio, you carefully select your target allocation. Perhaps you chose 60% stocks and 40% bonds based on your risk tolerance and financial goals. But markets move constantly, and over time, your carefully planned allocation can shift dramatically without any action on your part. This silent change is called portfolio drift, and addressing it through ETF portfolio rebalancing is essential for maintaining your intended risk level.

This guide walks you through the fundamentals of portfolio rebalancing, practical methods to implement it, and common considerations that affect your approach.

What Is ETF Portfolio Rebalancing?

ETF portfolio rebalancing is the process of adjusting your investment holdings to restore your original target asset allocation. When certain assets outperform others, they naturally grow to represent a larger portion of your portfolio. Rebalancing involves selling some of your winners and buying more of your underperformers to return to your planned mix.

For example, if you started with a 70/30 split between stock ETFs and bond ETFs, strong equity performance might shift your allocation to 80/20. Rebalancing would involve selling some stock ETFs and purchasing more bond ETFs to restore the 70/30 balance.

Why Rebalancing Matters for Risk Management

The primary purpose of rebalancing is risk management, not return maximisation. When your portfolio drifts from its target allocation, your risk profile changes. A portfolio that was appropriate for your risk tolerance when you created it may no longer be suitable after significant market movements.

Rebalancing helps investors maintain their intended risk exposure and avoid being caught off-guard by market volatility. When you allow your portfolio to drift, you may unknowingly take on more risk during bull markets, potentially facing larger losses during corrections.

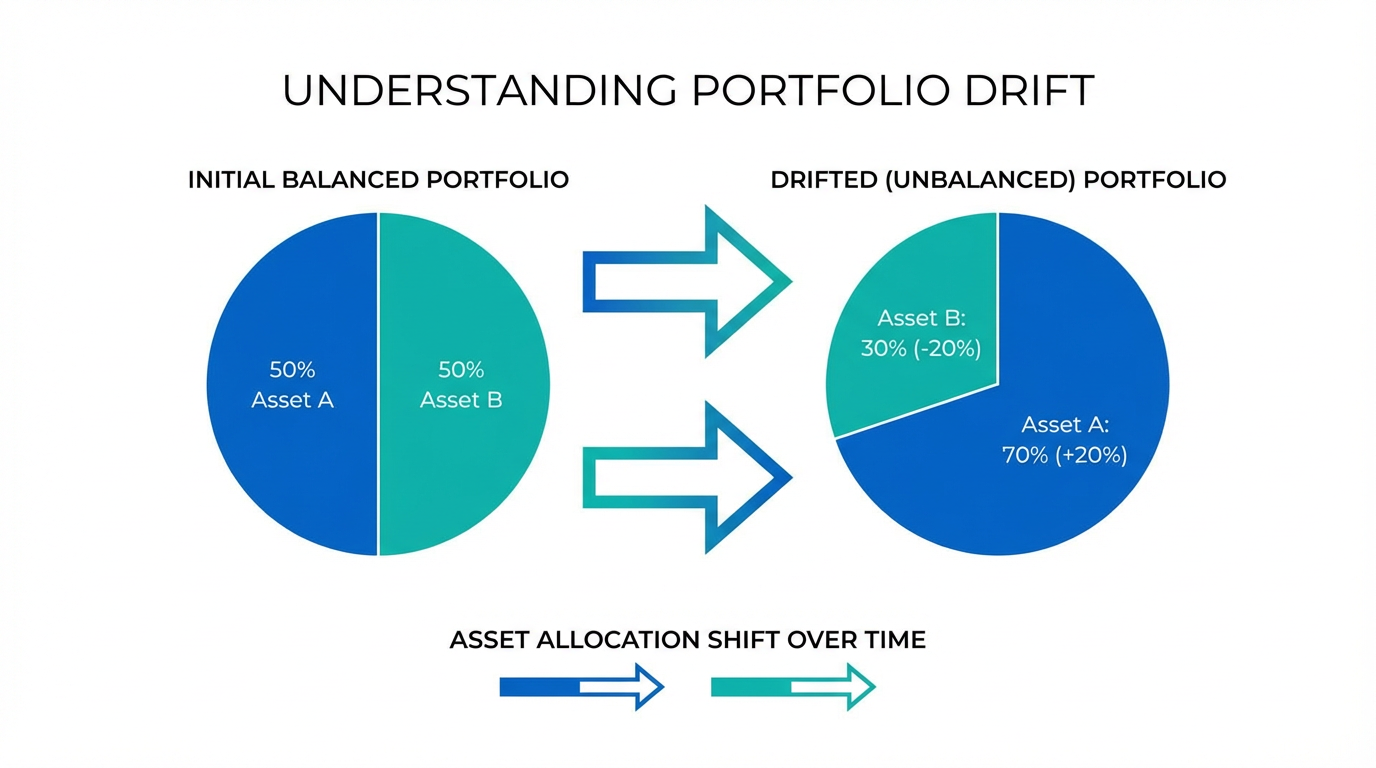

Understanding Portfolio Drift

Portfolio drift occurs naturally as different asset classes generate different returns over time. During periods of strong equity performance, stock-heavy portfolios grow faster than bond allocations, shifting your overall mix.

Consider this practical example: if you invested SGD 100,000 with a 60/40 stock/bond allocation, you would have SGD 60,000 in stocks and SGD 40,000 in bonds. If stocks gained 20% while bonds gained 5%, your portfolio would grow to SGD 114,000. But your new allocation would be roughly 63/37, meaning you now hold more equity risk than originally planned. (This example is for illustration purposes only and does not constitute investment advice.)

The Compounding Effect of Drift

Small allocation shifts may seem insignificant, but they compound over time. During prolonged periods of strong equity performance, portfolios can drift significantly from their target allocations, representing a meaningful increase in unintended risk exposure.

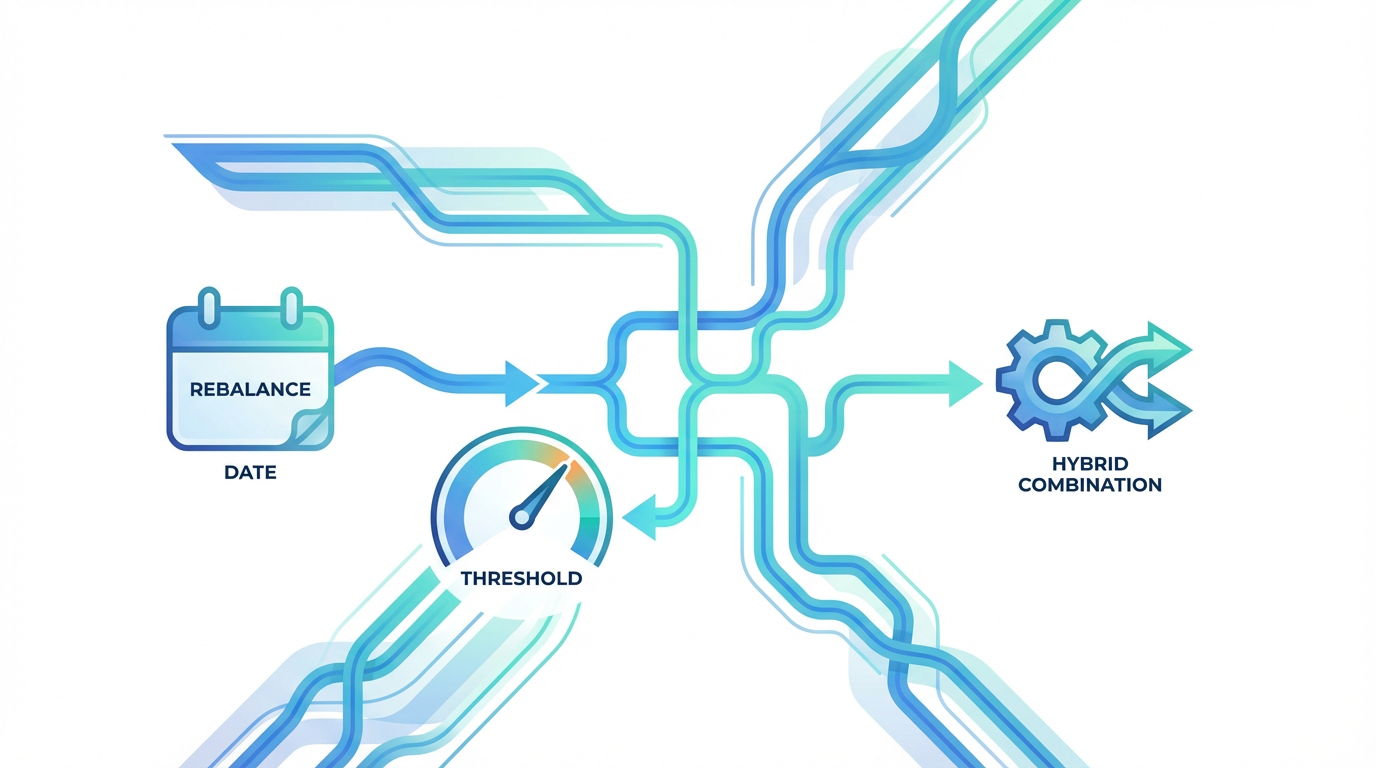

Three Methods for Rebalancing Your ETF Portfolio

There are three primary approaches to rebalancing, each with distinct advantages depending on your situation and preferences.

Calendar-Based Rebalancing

This approach involves reviewing and adjusting your portfolio at regular intervals, regardless of market conditions. Common frequencies include quarterly, semi-annually, or annually.

The advantage of calendar-based rebalancing is simplicity. You set a reminder and check your allocations on predetermined dates, removing emotion from the decision-making process. Annual or semi-annual rebalancing typically provides sufficient risk control without excessive trading.

Threshold-Based Rebalancing

With threshold-based rebalancing, you act when your allocation drifts beyond a predetermined limit. For instance, you might rebalance whenever any asset class moves more than 5% from its target weight.

This method requires more regular monitoring but ensures you only trade when necessary. It can be more responsive during volatile markets while avoiding unnecessary transactions during stable periods.

Combined Approach

Many investors use a hybrid method that combines both approaches. You check your portfolio at regular intervals but only rebalance if the drift exceeds your threshold. This provides the discipline of a schedule while avoiding unnecessary adjustments when your allocation remains close to target.

How Often Should You Rebalance?

The right rebalancing frequency balances maintaining your target allocation against minimising costs and complexity. Rebalancing too frequently may not improve outcomes and could reduce returns through increased transaction costs.

Tip: Annual or semi-annual rebalancing typically provides the right balance between maintaining your allocation and minimising costs. Consistency matters more than precise timing.

Some investors find that rebalancing every one to three years balances risk management with cost efficiency. Rebalancing more frequently than quarterly may not provide additional benefit and can expose portfolios to greater losses during sustained market downtrends as you continuously buy into declining assets.

Factors Affecting Rebalancing Frequency

Your ideal frequency depends on several factors:

Portfolio size: Larger portfolios may benefit from more frequent attention

Market volatility: Volatile periods create faster drift

Transaction costs: Higher costs favour less frequent rebalancing

Tax situation: Tax-advantaged accounts allow more flexibility

Tax Considerations When Rebalancing

Rebalancing in taxable accounts triggers capital gains when you sell appreciated assets. Understanding these implications helps you develop a tax-efficient approach.

Tax-Efficient Rebalancing Strategies

Consider tax-advantaged accounts: Where possible, conducting rebalancing within retirement accounts or other tax-sheltered vehicles may help reduce immediate tax impact.

Use new contributions strategically: Direct new investments toward underweighted asset classes rather than selling overweighted ones. This gradually restores your target allocation without triggering sales.

Redirect dividends and distributions: Instead of reinvesting dividends automatically, direct them toward underweighted positions.

Consider tax-loss harvesting: If you need to sell an asset at a loss, you may be able to offset gains elsewhere in your portfolio. When replacing a sold position, using an ETF can help avoid wash-sale rule complications.

Why ETFs Are Well-Suited for Portfolio Rebalancing

Exchange-traded funds, or ETFs, offer several characteristics that make them particularly suitable for rebalancing.

ETFs provide diversified exposure to specific asset classes, allowing you to adjust your allocation efficiently. Rather than buying or selling individual securities, you can shift entire asset class exposures with single transactions. This simplifies the rebalancing process and reduces the number of trades required.

ETFs generally feature low expense ratios and tax-efficient structures. Their structure typically results in fewer capital gains distributions, which can be advantageous for taxable accounts. You can explore the range of investment products available to build a diversified ETF portfolio.

Practical Advantages

Liquidity: ETFs trade throughout the day, allowing precise execution

Transparency: Holdings are disclosed daily

Low minimums: You can purchase single shares

Broad coverage: ETFs exist for nearly every asset class

Practical Steps to Rebalance Your Portfolio

These steps illustrate a typical process investors might follow for rebalancing:

Step 1: Review your target allocation

Confirm your intended asset mix still reflects your goals and risk tolerance. Life changes may warrant adjusting your targets before rebalancing.

Step 2: Calculate current allocation

Determine the current percentage each asset class represents in your total portfolio. You can track market performance of your holdings to understand current values.

Step 3: Identify gaps

Compare your current allocation to your target. Note which asset classes are overweighted and which are underweighted.

Step 4: Determine your approach

Decide whether to rebalance through selling overweighted assets, directing new contributions to underweighted ones, or a combination.

Step 5: Execute trades

Make the necessary transactions to restore your target allocation.

Step 6: Document and schedule

Record your actions and set a reminder for your next review date.

Common Rebalancing Considerations

Several factors can complicate rebalancing decisions. Being aware of these helps you develop a practical approach.

Behavioural Challenges

Rebalancing requires selling assets that have performed well and buying those that have lagged. This runs counter to natural instincts. Many investors find it psychologically difficult to sell winners, even when doing so is the rational choice for risk management.

Having a systematic approach removes emotion from the decision. When you commit to rebalancing at predetermined intervals or thresholds, you bypass the temptation to second-guess your strategy.

Transaction Costs and Partial Rebalancing

Each trade incurs costs through commissions, bid-ask spreads, or potential tax consequences. These costs can erode the benefits of rebalancing if you trade too frequently. Consider setting a minimum threshold and focusing on the most significantly overweighted or underweighted positions first. Partial rebalancing can reduce costs while still improving your risk profile.

Frequently Asked Questions

How much drift is acceptable before rebalancing?

A common guideline is to rebalance when any asset class drifts more than 5% from its target weight. For example, if your target stock allocation is 60%, you would rebalance when it exceeds 65% or falls below 55%. Some investors use tighter thresholds of 3%, while others prefer wider bands up to 10%.

Can regular contributions replace rebalancing?

Regular contributions can reduce the need for rebalancing by naturally directing money toward underweighted positions. This approach works well during accumulation phases when you are adding to your portfolio. However, larger portfolios or significant market movements may still require traditional rebalancing through sales.

Should I rebalance during market downturns?

Maintaining your rebalancing discipline during downturns is important, though emotionally challenging. Rebalancing during corrections means buying assets that have declined, which positions you for potential recovery. However, some investors choose to rebalance less frequently during sustained downtrends to manage transaction costs.

What is the difference between ETF rebalancing and portfolio rebalancing?

ETF rebalancing can refer to two things: the internal rebalancing that ETF managers perform to track their indices, or the rebalancing an investor does within their own ETF portfolio. This article focuses on the latter, which involves adjusting your personal holdings of various ETFs to maintain your target allocation.

Conclusion

ETF portfolio rebalancing is a fundamental practice for maintaining your intended investment strategy. By periodically restoring your target allocation, you manage risk effectively and avoid the gradual drift that can expose you to more volatility than you intended.

The key principles are straightforward: establish a clear target allocation, monitor your portfolio regularly, and adjust when drift exceeds your comfort level. Whether you choose calendar-based, threshold-based, or a combined approach, consistency is often emphasized in portfolio management practices.

Investors may begin with an annual review and adjust their approach over time. The discipline of regular rebalancing, combined with patience and a long-term perspective, supports sustainable portfolio management.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.