Money Market Funds: Low-Risk Cash Alternatives Explained

Money market funds provide a secure parking spot for cash while earning better returns than traditional savings accounts. Learn how these low-risk investments work and whether they fit your portfolio.

TL;DR: Money market funds are mutual funds that invest in high-quality, short-term debt securities, offering investors a low-risk option to preserve capital while earning competitive returns. They provide greater liquidity than fixed deposits and higher returns than traditional savings accounts, making them suitable for emergency funds, short-term goals, or temporary cash holdings within investment portfolios.

When cash sits idle in low-yield savings accounts, you miss opportunities for better returns. Yet riskier investments may not suit your need for stability and quick access. Money market funds bridge this gap, offering a low-risk option that typically outperforms traditional bank accounts while maintaining liquidity.

A money market fund invests in short-term, high-quality debt securities, providing stability and modest returns. Understanding how these funds work helps Singapore investors make informed decisions about managing cash holdings effectively.

What Are Money Market Funds?

Money market funds (often abbreviated as MMFs) are mutual funds that invest exclusively in short-term debt instruments with very low credit risk. These instruments typically include Treasury bills (T-bills), commercial paper issued by corporations, certificates of deposit (CDs) from banks, and repurchase agreements.

These funds focus on capital preservation and liquidity, aiming to maintain a stable net asset value (NAV) of one dollar per share. Securities mature within months, minimizing interest rate risk and maintaining price stability.

How Money Market Funds Differ from Bank Accounts

Money market funds differ from bank money market accounts. Bank accounts are insured by the Singapore Deposit Insurance Corporation (SDIC) up to SGD 100,000 per depositor per bank, while money market funds are investment products without deposit insurance protection. The trade-off is typically higher returns, with yields often exceeding traditional savings accounts.

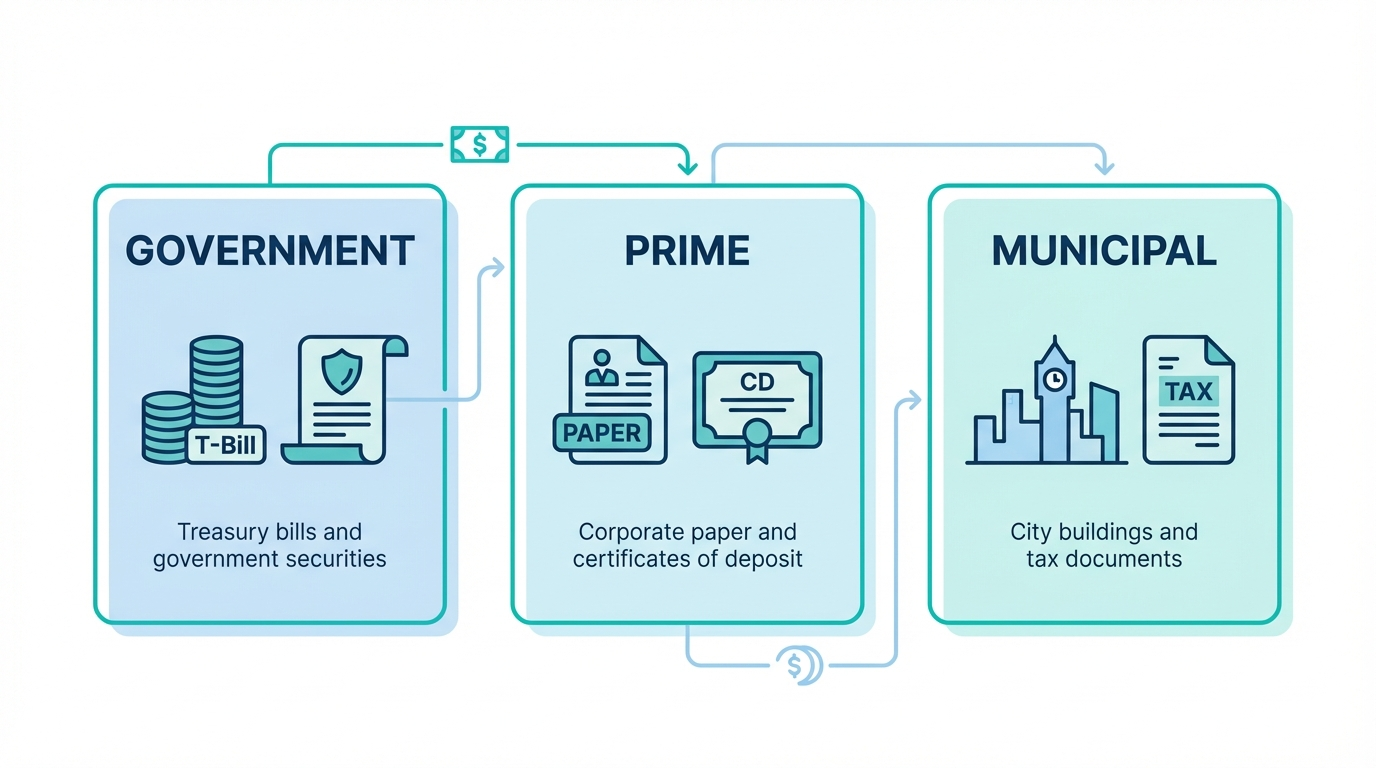

Types of Money Market Funds

Money market funds fall into three main categories based on their holdings and tax treatment.

Government Money Market Funds

These funds invest primarily in Treasury bills, government agency securities, and repurchase agreements backed by government securities. They represent the safest category due to highly creditworthy government issuers, making them ideal for risk-averse investors prioritizing capital preservation.

Prime Money Market Funds

Prime funds (also called general money market funds) have broader mandates, investing in government securities plus high-quality corporate commercial paper, bank certificates of deposit, and other corporate short-term debt. By taking slightly more credit risk, they typically offer higher yields than government funds.

Municipal Money Market Funds

These funds invest in short-term debt from state and local governments, popular in markets offering tax advantages. For Singapore investors, municipal funds are less relevant as they're structured for specific jurisdictional tax benefits.

Benefits of Money Market Funds

Competitive Returns

Money market funds typically generate returns exceeding traditional bank savings accounts.They adjust quickly to monetary policy changes, allowing investors to benefit from rising rate environments faster than bank savings products.

High Liquidity

Most funds allow share redemption on any business day, with proceeds available within one to three business days. Unlike fixed deposits with early withdrawal penalties, money market funds provide accessible cash storage for emergency funds or short-term needs.

Professional Management and Diversification

Money market funds provide instant diversification across dozens or hundreds of securities, mitigating single-issuer default risk. Professional managers continuously monitor credit quality, adjust holdings, and reinvest maturing securities without requiring investor attention.

Low Volatility

Short-term, high-quality securities mean minimal price fluctuations. The stable NAV objective keeps principal steady while account value grows through dividends, making these funds psychologically easier to hold than stocks or long-term bonds.

Understanding the Risks

Money market funds are low-risk but not risk-free. A balanced understanding of both benefits and risks supports informed investment decisions.

Not Covered by Deposit Insurance

Unlike bank deposits, money market funds lack Singapore Deposit Insurance Corporation coverage. Theoretically, you could lose money if investments perform poorly. However, the Monetary Authority of Singapore (MAS) sets strict diversification requirements across short-term, high-quality debt from governments, banks, and corporates. Events where funds "broke the buck" (dropped below one dollar per share NAV) remain extremely rare historically.

Inflation Risk

When inflation outpaces fund returns, purchasing power erodes. If a fund yields two percent but inflation runs at three percent, real returns are negative. This makes money market funds better suited for short-term goals rather than long-term wealth accumulation.

Interest Rate Sensitivity

While less sensitive than long-term bonds, money market funds respond to rate changes. Declining rates reduce yields; rising rates increase them as holdings mature and reinvest at higher rates.

Credit Risk

Prime funds investing in corporate debt carry default risk, though managers evaluate credit quality carefully and regulations limit holdings to high-grade securities. Government funds largely avoid this by investing in government-backed securities, explaining their slightly lower yields.

Who Should Consider Money Market Funds?

Emergency Fund Storage

Financial advisors usually recommend three to six months of living expenses in emergency funds. Money market funds provide better returns than savings accounts while maintaining quick access for unexpected expenses.

Short-Term Savings Goals

For purchases within one to two years—cars, home down payments, weddings—money market funds grow savings modestly without significant market risk. Their stability suits defined near-term objectives.

Temporary Cash Holdings

When holding cash from investment sales, bonuses, or inheritances, money market funds earn returns while you determine next steps, rather than leaving cash idle in low-interest accounts.

Conservative Portfolio Allocation

Investors nearing or in retirement often maintain cash equivalents for conservative allocation. Money market funds provide stability and income without stock or long-term bond volatility.

Getting Started with Money Market Funds

Selecting the Right Fund

When evaluating funds, determine whether you prefer government funds for maximum safety or prime funds for potentially higher yields. Review historical performance (though past results don't guarantee future outcomes), examine expense ratios, check minimum investment requirements, and verify availability through your brokerage platform.

Using a Digital Brokerage Platform

Platforms like Longbridge provide access to money market funds alongside other products. You can explore the range of investment products suitable for various risk tolerances.

Understanding Costs and Fees

While money market funds have lower expense ratios than actively managed equity funds, costs impact net returns. Evaluate platforms' pricing structure to understand all investing costs.

Money Market Funds in Your Overall Strategy

View money market funds as one component of comprehensive financial strategy, providing stability, liquidity, and modest returns for cash equivalent allocations. They complement rather than replace other vehicles like stocks, ETFs, and bonds.

Appropriate allocation depends on individual circumstances: time horizon, risk tolerance, income needs, and financial goals. A balanced approach includes money market funds for emergencies, additional cash for near-term goals, and growth-oriented assets for long-term objectives.

Frequently Asked Questions

Are money market funds safe investments?

Money market funds are low-risk but not risk-free. They invest in high-quality, short-term securities aiming for stable NAV, but lack deposit insurance coverage. While losses are extremely rare, they remain possible. Singapore's Monetary Authority of Singapore enforces strict credit quality and diversification standards.

How do money market fund returns compare to savings accounts?

Money market funds typically offer higher yields than bank savings accounts, with exact differences varying by interest rates and holdings. In exchange for potentially higher returns, investors accept lack of deposit insurance coverage.

Can I lose money in a money market fund?

While designed for capital preservation with rare historical losses, losing money remains theoretically possible through investment defaults or "breaking the buck" (NAV dropping below one dollar per share). Strict regulations and high-quality holdings make such events extremely uncommon. Government funds carry lower risk than prime funds.

How quickly can I access my money from a money market fund?

Redemptions process on any business day, with proceeds typically available within one to three business days depending on fund and platform processing times.

What is the difference between a money market fund and a money market account?

Money market accounts are bank deposit accounts covered by SDIC insurance up to SGD 100,000 per depositor per bank. Money market funds are mutual funds without deposit insurance but typically offering higher returns and access to institutional-grade securities with professional management.

Conclusion

Money market funds offer effective low-risk cash alternatives, balancing safety, liquidity, and modest returns through high-quality, short-term debt securities. They bridge bank deposit security and higher-risk investment growth potential.

For Singapore investors, these funds serve valuable roles—housing emergency funds or temporarily parking cash awaiting deployment. Understanding different fund types, benefits, and limitations enables informed decisions about incorporation into investment strategies.

Consider personal circumstances, time horizon, and risk tolerance with any investment decision. Money market funds complement rather than replace other vehicles within diversified financial approaches.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.