Target Date Funds: Set-and-Forget Retirement Investing

Target date funds automatically adjust your investment mix as you approach retirement, offering a simple set-and-forget solution for long-term wealth building with professional management.

TL;DR: Target date funds are retirement investment vehicles that automatically adjust their mix of stocks and bonds as you approach retirement. By selecting a fund matching your target retirement year, you gain instant diversification and professional management without needing to rebalance your portfolio manually—making them a relatively simple way to invest for retirement.

Retirement planning can feel overwhelming. With countless investment options, complex asset allocation strategies, and the ongoing need to rebalance your portfolio, many investors struggle to know where to start. This is where target date funds offer a simplified approach to a complicated problem.

Target date funds offer a streamlined approach to retirement investing that can help reduce some common challenges. Rather than juggling multiple investments and constantly adjusting your portfolio, you make one decision: choose the fund matching your expected retirement year. Professional fund managers handle everything else, automatically shifting from growth-focused investments to more conservative options as you near retirement.

What Are Target Date Funds?

A target date fund (TDF), also known as a lifecycle fund or target retirement fund, is a diversified mutual fund or exchange-traded fund (ETF) that automatically adjusts its investment mix over time. The fund's name typically includes a target year—such as "2040 Fund" or "2050 Fund"—representing the approximate year investors plan to retire.

These funds operate on a straightforward principle: younger investors with decades until retirement can tolerate more risk and benefit from higher potential returns through stock-heavy portfolios. As retirement approaches, the need to protect accumulated wealth becomes more important, justifying a shift toward more stable investments like bonds.

According to research from Morningstar, target date strategies held over USD 4 trillion in assets at the end of 2024, making them one of the most popular retirement savings vehicles worldwide.

How Target Date Funds Work

When you invest in a 2045 target date fund, the fund managers construct a portfolio appropriate for someone planning to retire around 2045. In the early years, the fund might allocate 90% to stocks and 10% to bonds, maximizing growth potential.

As time passes, the fund automatically rebalances, gradually reducing stock exposure and increasing bond holdings. By your target retirement date, the allocation might be 30% stocks and 70% bonds, prioritizing capital preservation over aggressive growth. This automatic rebalancing helps you avoid emotional decisions during market volatility.

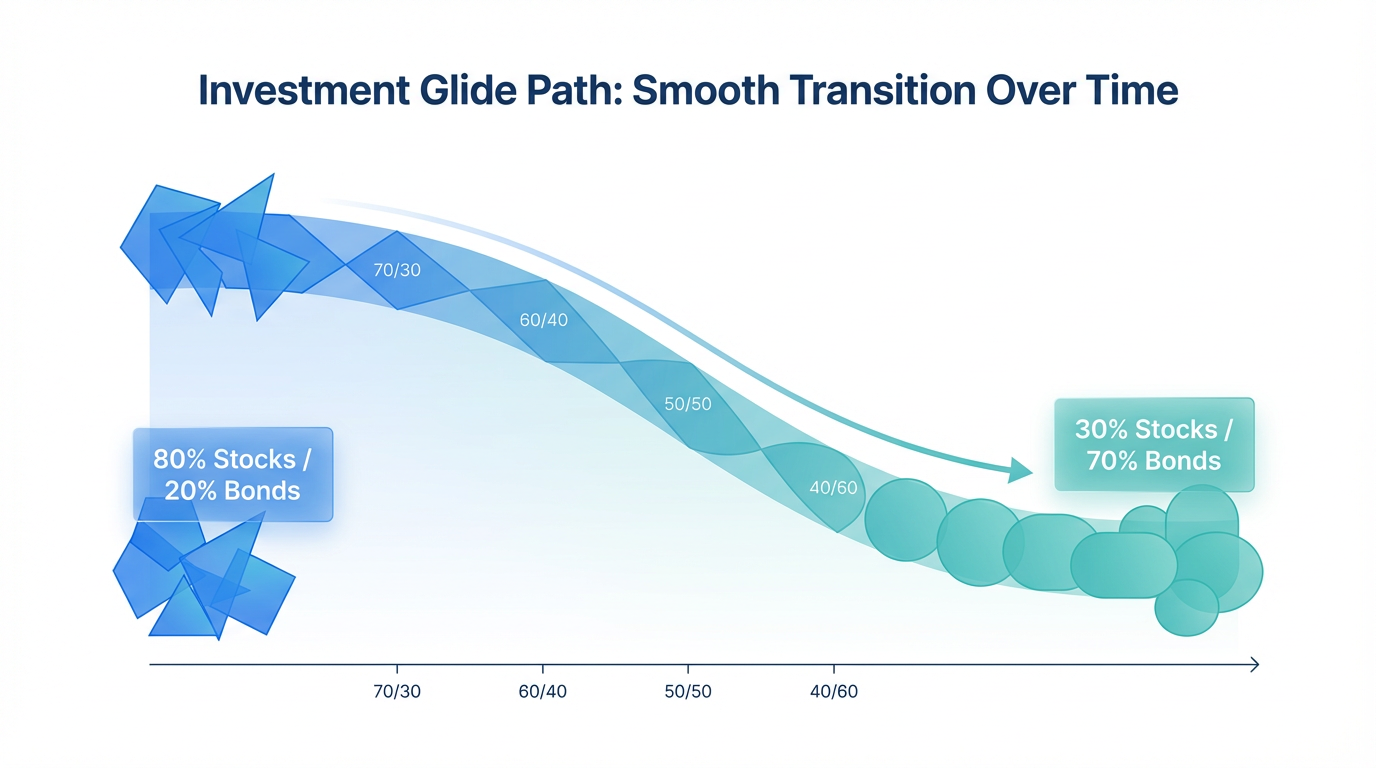

Understanding the Glide Path

The glide path represents the heart of any target date fund's strategy. This term describes how the fund's asset allocation shifts over time, typically visualized as a descending curve showing the gradual transition from stocks to bonds.

Different fund providers design different glide paths based on their investment philosophy and risk assumptions. Understanding these variations helps you choose a fund aligned with your personal circumstances.

"To" Retirement vs "Through" Retirement Funds

One crucial distinction separates target date funds into two categories:

"To" retirement funds reach their most conservative asset allocation at the target date and typically maintain that allocation afterward. These funds assume you will withdraw your money at retirement or shortly thereafter.

"Through" retirement funds continue adjusting their allocation for 10 years or more past the target date, assuming you will draw down your retirement savings gradually over many years.

Neither approach is inherently better—the right choice depends on your retirement plans and risk tolerance.

Key Benefits of Target Date Funds

Target date funds address several challenges that often derail retirement investors.

Automatic Diversification

Target date funds provide instant diversification by investing in a mix of stocks, bonds, and sometimes other assets like real estate investment trusts (REITs). Rather than researching individual securities, you gain exposure to hundreds or thousands of investments through one fund. This broad diversification would be difficult and expensive to replicate independently.

Professional Management

Target date funds are managed by professional investment teams with extensive experience and research resources. These managers monitor market conditions, rebalance the portfolio as needed, and ensure the fund stays on its intended glide path. For investors without the time or expertise to actively manage their portfolios, this professional oversight provides valuable peace of mind.

Behavioral Advantages

Perhaps the most underappreciated benefit is how target date funds protect investors from behavioral mistakes. Some research suggests that individual investors may buy during market highs and sell during downturns. Target date funds remove these temptation points by automatically maintaining your target allocation.

Important Considerations and Limitations

While target date funds offer compelling benefits, they are not perfect solutions for everyone.

One-Size-Fits-All Approach

Target date funds assume all investors retiring in the same year have similar needs and risk tolerance. In reality, circumstances vary dramatically. If you have particularly high or low risk tolerance, substantial assets elsewhere, or unique financial circumstances, a customized portfolio might serve you better.

Fee Considerations

Target date funds charge expense ratios—annual fees expressed as a percentage of your investment. These fees vary considerably between providers, with lower-cost options generally producing better long-term outcomes.

Since target date funds typically invest in other underlying funds, you may effectively pay fees at two levels. When evaluating options, traders may typically prioritize those with expense ratios below 0.50% annually. Many index-based target date funds may typically charge 0.15% or less, while actively managed options may typically charge 0.50% to 1.00% or more.

Limited Customization

By design, target date funds offer little flexibility. You cannot adjust the glide path, select different underlying investments, or modify allocations based on market conditions. However, this constraint also prevents costly mistakes and keeps your strategy on track.

No Guaranteed Outcomes

Target date funds do not guarantee returns or protect against losses. During market downturns, your account value will decline. While the glide path reduces risk as you near retirement, it does not eliminate risk entirely.

How to Choose the Right Target Date Fund

Selecting a target date fund requires more than matching the target year to your planned retirement date.

Selecting Your Target Date

Start with your expected retirement age. Most target date funds are offered in five-year increments, so select the fund closest to your target year. Some investors choose a later target date if they have higher risk tolerance, or an earlier date for more conservative positioning.

Evaluating Glide Path Design

Review the fund's glide path to understand its planned allocation at retirement. Does the fund hold 30%, 50%, or 70% in stocks at the target date? Compare this design to your expected needs. If you plan to draw income from your portfolio throughout retirement, a more aggressive glide path might be appropriate.

Comparing Expense Ratios

Fees directly reduce returns, so lower expense ratios generally produce better outcomes. A difference of 0.50% annually compounds to significant amounts over decades of investing. Index-based target date funds typically charge lower fees than actively managed ones.

Target Date Funds for Singapore Investors

For Singapore investors, target date funds offer a convenient way to save for retirement while accessing global markets. Through platforms like Longbridge, investors can access a range of investment products including exchange-traded funds (ETFs) that employ target date strategies.

While Singapore's Central Provident Fund (CPF) provides a foundation for retirement savings, many investors supplement their CPF through self-directed investing. Target date funds can serve as core holdings in Supplementary Retirement Scheme (SRS) accounts, providing automatic diversification across international markets.

The CPF already provides a conservative, guaranteed return component, which may influence how some investors approach risk in their broader portfolio. Singapore investors should also consider tax implications—gains from fund investments in SRS accounts are tax-deferred until withdrawal, making them particularly efficient for long-term retirement investing.

Frequently Asked Questions

What is a target date fund and how does it work?

A target date fund automatically adjusts its mix of stocks and bonds based on a target retirement date. The fund starts with higher stock allocation when retirement is distant, then gradually shifts toward bonds as the target date approaches. This automatic rebalancing requires no action from investors.

Are target date funds guaranteed to provide income in retirement?

No, target date funds do not provide guaranteed income or returns. They are subject to market risk and can lose value, even after reaching the target date. While they aim to reduce risk through systematic rebalancing, they remain exposed to market fluctuations.

How do I know which target date to choose?

Select the target date fund that most closely matches your expected retirement year. For example, if you plan to retire in 2043, choose either a 2040 or 2045 fund. You can adjust based on risk tolerance—selecting a later date for more aggressive positioning or an earlier date for conservative positioning.

What fees do target date funds charge?

Target date funds charge expense ratios ranging from as low as 0.10% for index-based funds to 1.00% or more for actively managed options. Always compare expense ratios when evaluating options, as even small fee differences significantly impact long-term returns.

Conclusion

Target date funds represent a practical solution to maintaining appropriate asset allocation throughout your career while gradually reducing risk as retirement approaches. By automating the rebalancing process, these funds help investors stay on track toward their retirement goals without constant portfolio management.

The simplicity of target date funds makes them particularly valuable for investors seeking professional management without complexity. As you plan your retirement strategy, consider whether a target date fund aligns with your investment philosophy, risk tolerance, and financial goals.

Explore the Longbridge app to access investment products across multiple markets. Learn more about retirement planning through our educational resources.