Unit Investment Trust vs ETF: Key Differences for Singapore Investors

Discover how Unit Investment Trusts and ETFs differ in structure, costs, and tax treatment, with practical insights for Singapore investors navigating the U.S. market opportunities.

TL;DR: Unit Investment Trusts (UITs) are fixed-portfolio investments with predetermined termination dates (typically 15 months to 30 years), while Exchange-Traded Funds (ETFs) offer continuous trading with flexible portfolios. For Singapore investors accessing U.S. markets, ETFs generally provide lower costs and greater liquidity, but both face a 30% dividend withholding tax. Ireland-domiciled ETFs can reduce this to 15%.

When exploring investment options in U.S. markets, Singapore investors often encounter two distinct investment vehicles: Unit Investment Trusts and Exchange-Traded Funds. While both offer pathways to diversified portfolios, they differ fundamentally in structure, costs, flexibility, and tax treatment. Understanding these differences is particularly important because Singapore lacks a tax treaty with the United States, affecting how your investment returns are taxed. This guide breaks down the unit investment trust vs ETF comparison for Singapore-based investors through a comprehensive range of investment products.

What is a Unit Investment Trust?

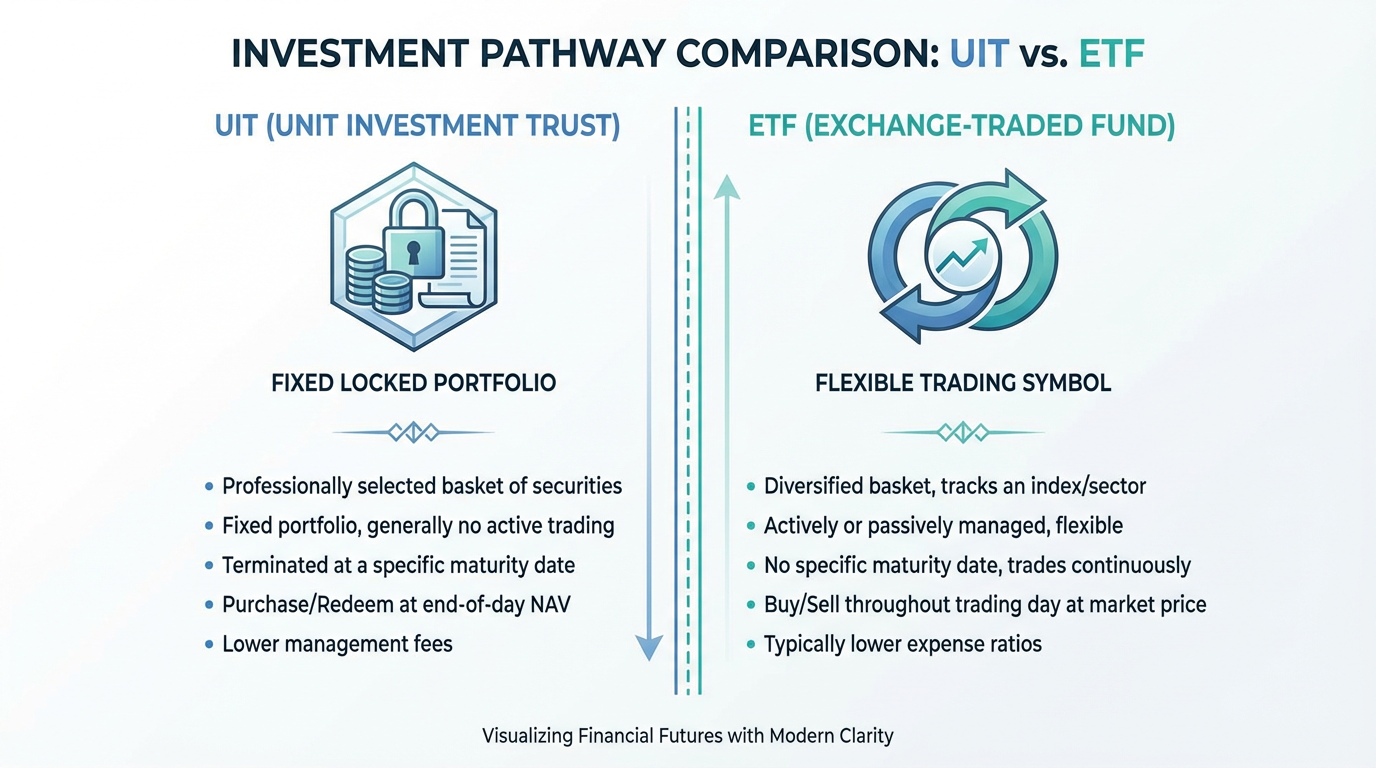

A Unit Investment Trust (UIT) is a unique investment structure that differs from the actively managed unit trusts popular in Singapore. In the U.S. market, a UIT is an investment company that offers a fixed portfolio of securities as redeemable units to investors for a specific period.

Key Characteristics of UITs

UITs follow a strict buy-and-hold investment strategy. Once the portfolio is assembled, those securities remain unchanged throughout the life of the trust. There is no active trading or rebalancing based on market conditions.

Every UIT has a predetermined termination date, typically ranging from 15 months to more than 30 years. At termination, the securities are sold and proceeds distributed to unit holders.

Investors purchase units during an initial offering period, after which no new units are created. Liquidity is generally lower than actively traded securities. Investors can typically redeem units at net asset value before termination, though redemption fees may apply.

What is an Exchange-Traded Fund?

An Exchange-Traded Fund (ETF) is an investment fund that trades on stock exchanges throughout the trading day, similar to individual stocks. ETFs are structured as open-ended funds, meaning new shares can be created or redeemed based on investor demand.

Key Characteristics of ETFs

Most ETFs track a specific market index, sector, or asset class, such as the S&P 500, MSCI World, or technology sectors. This passive approach mirrors the underlying index with minimal intervention.

ETFs trade continuously during market hours at prices determined by supply and demand. Investors can buy or sell shares anytime the market is open, providing flexibility to respond to market movements or adjust portfolio allocation.

Unlike UITs, ETFs have no expiration date and operate indefinitely, making them suitable for long-term strategies without forced liquidation.

Core Structural Differences Between UITs and ETFs

Portfolio Management Approach

UITs maintain a static portfolio from inception to termination. Securities remain in place regardless of market conditions, providing complete transparency throughout the investment period.

ETFs allow periodic rebalancing to maintain alignment with their target index. When an index adds or removes companies, the ETF adjusts accordingly.

Liquidity and Trading Flexibility

ETFs trade continuously during market hours at prevailing market prices, providing intraday liquidity valuable for quick capital access or capitalizing on market movements.

UITs offer less flexibility. Investors typically redeem units at end-of-day NAV. Secondary markets have limited liquidity with potentially wider bid-ask spreads.

Investment Time Horizon

UITs have predetermined termination dates, creating defined investment timelines. ETFs operate with indefinite lifespans, suitable for flexible timelines without forced liquidation.

Cost Considerations: Fees and Expenses

UIT Cost Structure

UITs typically charge an initial sales charge ranging from 0.5% to 6% of the investment amount. Annual operating expenses generally range from 0.75% to 2%, covering trustee fees and administrative costs. The combination of initial sales charges and ongoing fees can significantly impact overall returns, particularly for shorter-term UITs.

ETF Cost Structure

ETFs are widely recognized for their cost efficiency. Most broad-market index ETFs typically have expense ratios below 0.5% annually, with many popular offerings typically charging 0.1% or less. There are no initial sales loads when purchasing ETFs.

For Singapore investors, Longbridge provides access to U.S. market ETFs with a transparent pricing structure. The absence of sales loads and lower ongoing expenses make ETFs particularly attractive for cost-conscious investors.

Tax Implications for Singapore Investors

The 30% Dividend Withholding Tax Challenge

Singapore investors face a 30% dividend withholding tax on U.S.-listed securities. Because Singapore does not maintain a tax treaty with the United States, the Internal Revenue Service withholds 30% of all dividend payments from U.S. stocks, ETFs, bonds, and UITs before they reach your account.

If a U.S. ETF or UIT distributes USD 100 in dividends, you actually receive only USD 70. This substantial tax drag can materially impact investment returns, particularly for dividend-focused strategies.

Capital Gains Treatment

While dividend taxation poses challenges, Singapore investors benefit regarding capital gains. The U.S. government does not tax capital gains earned by foreign investors on U.S. securities. Any profits you realize from selling U.S. ETFs or UITs are yours to keep, with no U.S. tax liability. Singapore itself does not impose capital gains tax on individuals, creating a favorable environment for growth-oriented strategies that prioritize capital appreciation.

Alternative: Ireland-Domiciled ETFs

A tax-efficient strategy involves considering Ireland-domiciled ETFs rather than U.S.-listed equivalents. Thanks to the tax treaty between the United States and Ireland, these ETFs face only a 15% withholding tax on U.S. dividend income, half the rate on U.S.-listed funds.

For a USD 5,000 investment with a 2% dividend yield:

-

U.S.-listed ETF: USD 30 in dividend withholding tax (30%)

-

Ireland-domiciled ETF: USD 15 in dividend withholding tax (15%)

While Ireland-domiciled ETFs may have slightly higher expense ratios, the tax savings often more than compensate, particularly for dividend-generating portfolios.

Suitability for Different Investor Profiles

When UITs May Be Appropriate

UITs suit investors seeking a truly passive buy-and-hold approach with a defined time horizon. If you are saving for a goal with a specific target date, such as a child's education expense in three years, a UIT maturing at that time provides a disciplined approach. The fixed portfolio also offers complete transparency, with no surprises from management changes or rebalancing decisions.

When ETFs Are Generally Preferred

For most Singapore investors accessing U.S. markets, ETFs present compelling advantages. Lower costs, superior liquidity, continuous trading, and indefinite investment horizons make them highly versatile. ETFs particularly benefit investors who value flexibility in adjusting asset allocation or responding to market opportunities. Cost-conscious investors appreciate ETF fee structures that often result in total annual costs below 0.2%, compared to UIT expenses exceeding 2% annually.

Practical Investment Strategies for Singapore Investors

Minimizing Tax Impact

Given the 30% dividend withholding tax on U.S. securities, Singapore investors may consider the following strategies when evaluating tax impact:

Focus on growth-oriented ETFs: Some investors may consider companies that reinvest earnings rather than paying dividends to avoid triggering withholding taxes. Technology-focused ETFs often emphasize growth over income, reducing tax drag.

Consider Ireland-domiciled alternatives: For dividend-focused portfolios, Ireland-domiciled ETFs tracking the same indices provide 15-percentage-point tax savings on dividend withholding.

Evaluate total return expectations: Calculate whether the liquidity of U.S.-listed ETFs justifies the higher withholding tax, or whether Ireland-domiciled alternatives better serve your strategy.

Portfolio Construction and Management

Broad-market ETFs are often used by investors seeking diversified exposure to U.S. equities, while sector-specific ETFs allow targeted allocations. Rather than viewing unit investment trust vs ETF as an either-or decision, assess each vehicle against your specific goals, time horizon, liquidity needs, and tax situation. ETFs facilitate regular monitoring and rebalancing, allowing quick adjustments when allocations shift.

Frequently Asked Questions

What is the main difference between a Unit Investment Trust and an ETF?

UITs maintain fixed portfolios that remain unchanged from creation to termination, with predetermined end dates typically ranging from 15 months to 30 years. ETFs trade continuously on exchanges with flexible portfolios that can be rebalanced to track their target indices, with no expiration dates.

Are UITs or ETFs more cost-effective for Singapore investors?

ETFs generally offer superior cost efficiency with expense ratios often below 0.5% and no initial sales charges. UITs typically charge upfront fees of 0.5% to 6% plus annual expenses of 0.75% to 2%. Combined with trading flexibility and tax planning opportunities, ETFs usually present a more cost-effective choice.

How does the 30% U.S. dividend withholding tax affect my returns?

The 30% withholding tax significantly reduces dividend income from U.S. securities. For every USD 100 in dividends, you receive only USD 70. This particularly impacts high-dividend portfolios, making growth-focused strategies or Ireland-domiciled ETFs (with 15% withholding) more attractive alternatives.

Can I trade UITs as easily as ETFs?

No, UITs offer substantially less trading flexibility. ETFs trade continuously throughout market hours like stocks, allowing you to buy or sell at any time at prevailing market prices. UITs typically only allow redemptions at end-of-day NAV, with limited secondary market trading.

Should Singapore investors choose U.S.-listed or Ireland-domiciled ETFs?

The decision depends on your portfolio strategy. For dividend-focused investments, Ireland-domiciled ETFs provide significant tax advantages with 15% withholding versus 30% on U.S.-listed ETFs. For growth-focused strategies where dividends are minimal, the lower expense ratios of U.S.-listed ETFs may outweigh the tax difference. Evaluate total costs to determine which option best serves your needs.

Do UITs have any advantages over ETFs?

UITs offer specific benefits for certain situations. The fixed portfolio provides complete transparency and a truly passive buy-and-hold approach. The predetermined termination date can align with specific financial goals requiring capital at a known future date. For investors who value these characteristics and accept higher costs and lower liquidity, UITs may serve a niche role.

Conclusion

When evaluating unit investment trust vs ETF for accessing U.S. market opportunities, Singapore investors will generally find ETFs offer compelling advantages. Lower costs, superior liquidity, continuous trading, and flexibility make ETFs suitable for most investment strategies. The ability to employ tax-efficient structures through Ireland-domiciled alternatives further enhances their appeal.

UITs serve a more specialized role for investors seeking fixed portfolios with defined termination dates aligned to specific financial goals. However, higher fees, limited liquidity, and identical dividend withholding tax treatment make them less attractive for most situations.

Understanding the 30% U.S. dividend withholding tax remains essential for Singapore investors. Incorporating this tax consideration into your investment planning ensures realistic return expectations and may guide you toward growth-oriented strategies or Ireland-domiciled alternatives that minimize tax drag.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.