Black Swan Protection with Options: A Portfolio Hedging Guide

Black swan events can devastate unhedged portfolios in days. Discover how options — from protective puts to VIX strategies — may provide a structured defence against rare but severe market crashes.

TL;DR: A black swan event is a rare, unpredictable market shock that can devastate portfolios built on normal risk models. Options, specifically put options and volatility-linked instruments, can reduce downside exposure in certain extreme scenarios. This guide explains how these strategies work, what they cost, and how to apply them as part of a broader risk management plan.

When the 2008 financial crisis unfolded, or when global markets fell sharply in early 2020 during the COVID-19 pandemic, investors without hedges in place suffered severe losses within days. These events are what financial thinker Nassim Nicholas Taleb called "black swans": rare occurrences that carry extreme consequences and appear obvious only in hindsight. For investors trading options on US markets, understanding black swan protection with options is practical risk management, not just theory.

This article explains what black swan events are, how options function as a protective instrument, the main strategies available, and their real trade-offs.

What Is a Black Swan Event?

Nassim Nicholas Taleb introduced the black swan concept in his 2007 book The Black Swan: The Impact of the Highly Improbable. A black swan event has three defining features: it is extremely rare, it has a severe impact, and in hindsight people tend to rationalise it as foreseeable.

In financial markets, black swan events include the 1987 stock market crash, the collapse of Lehman Brothers in 2008, and the COVID-19-driven market plunge in March 2020. Traditional risk frameworks typically assume returns follow a normal distribution, underestimating extreme events at the edges — what statisticians call "fat tails."

Why Diversification Alone May Not Be Enough

During a black swan shock, assets that normally move independently tend to crash together. Asset correlations with broad equity indices spike sharply when volatility rises, meaning diversification across equities can offer limited protection precisely when you need it most. This is why options-based hedges are used as a complementary layer of defence.

How Options Work as Portfolio Insurance

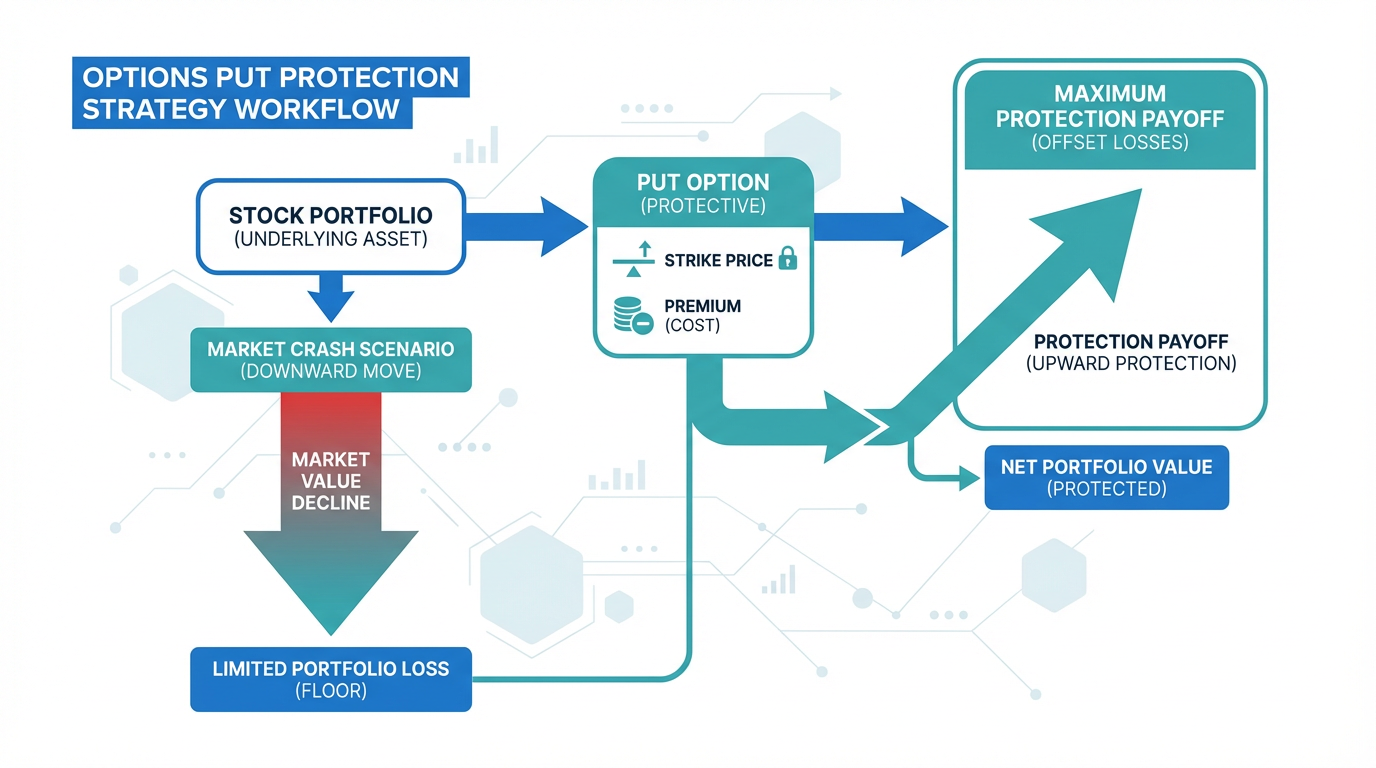

An option is a contract that gives the buyer the right, but not the obligation, to buy or sell an underlying asset at a set price (the strike price) on or before an expiration date. For black swan protection, the most relevant instruments are put options.

A put option gains in value when the price of the underlying asset falls below the strike price. If you hold a portfolio of US stocks and buy put options on a broad index such as the S&P 500, those puts can offset some of your portfolio losses if the market drops sharply.

The key principle here is asymmetry: the maximum loss on a long put option is limited to the premium paid, while the potential gain can be substantial if the market falls dramatically. This asymmetric payoff is what makes options particularly suited for tail risk hedging.

Note: Options involve risk and are not suitable for all investors. Before trading options, ensure you fully understand how they work, including the impact of time decay, implied volatility, and leverage. You can explore foundational investment concepts at the Longbridge Academy.

Key Options Strategies for Black Swan Protection

Several approaches exist for constructing options-based black swan hedges, each with different cost profiles and protection levels.

Far Out-of-the-Money Put Options

The simplest approach involves buying put options with strike prices well below the current market level — often 15% to 25% lower, known as out-of-the-money (OTM) puts. Because the probability of such a large decline in a short timeframe is statistically low, OTM puts are relatively inexpensive.

The trade-off is significant: these options expire worthless most of the time, as extreme crashes are rare. The ongoing cost of renewing these positions, known as the "carry cost," is a real drag on portfolio returns during calm markets. For example, during the prolonged market decline of 2022, where the S&P 500 declined gradually over the year rather than in a sudden drop, far OTM puts provided limited benefit because the decline was too gradual.

Put Spreads and Ratio Spreads

To reduce the premium cost of holding put protection, some traders use put spreads: buying a put option at a higher strike price and simultaneously selling a put at a lower strike price. This approach lowers the net cost but also caps the maximum payout if the market falls far enough.

Ratio spreads, such as buying one put and selling two at a lower strike, can sometimes be structured to collect a small credit upfront, though they carry additional risk if the market falls beyond the short put strikes.

Volatility Index (VIX) Options

The CBOE Volatility Index (VIX) measures near-term volatility expectations based on S&P 500 option prices. During black swan events, the VIX spikes dramatically — surging above 80 during the 2008 crisis and above 65 during the March 2020 COVID shock, according to CBOE data.

Buying call options on the VIX provides exposure to this volatility surge. Unlike index put options that target a specific market level, VIX options hedge against volatility itself, providing protection regardless of which direction prices move — though they are most effective when markets fall sharply and quickly.

The 90/10 Strategy

One structure that has been discussed in academic and institutional literature involves allocating a portion of capital to defensive assets while using derivatives for asymmetric exposure. Some institutional investors may use what is called the 90/10 approach: allocating roughly 90% of the portfolio to government bonds and 10% to long call options on equities. The bonds provide stability, while the calls provide upside participation. The result is a structure where severe equity crashes have limited impact on the overall portfolio, though some upside is sacrificed and effectiveness depends on interest rates and option pricing at the time.

Weighing the Costs and Limitations

No hedging strategy is without trade-offs. Understanding the limitations of options-based black swan protection is as important as understanding how it works.

Ongoing premium costs: Buying put options requires paying a premium. During calm markets, these expire worthless repeatedly, creating a recurring cost that reduces overall returns.

Timing and expiration: Options have fixed expiration dates. A black swan event that occurs after your options expire leaves you unprotected. Maintaining rolling positions requires active management and ongoing capital commitment.

Moderate declines are less protected: Far OTM puts and VIX options are designed for extreme events. A gradual bear market or correction of 10% to 20% may not trigger meaningful gains from these instruments, yet still causes notable portfolio damage.

Volatility pricing: When market stress increases, implied volatility rises and options become more expensive. If you wait until risk is visibly elevated to buy protection, premiums may already reflect much of the anticipated danger.

Tip: Implementing hedges during periods of lower market volatility — when premiums are relatively inexpensive — may be more cost-effective depending on market volatility conditions than purchasing during periods of heightened fear.

Investors can stay informed on market conditions using tools like Longbridge's market data services and latest news coverage, which can help identify shifts in volatility regimes.

Building a Layered Risk Management Approach

Options-based black swan protection works best as one component of a broader risk management framework, not as a standalone solution.

Position Sizing

Keeping individual positions appropriately sized — a common approach is to keep individual positions within 1% to 5% of total portfolio value per trade — limits the damage any single event can cause, even before options protection kicks in.

Diversification Across Asset Classes

While equity correlation spikes during crises, other asset classes can behave differently. Government bonds, gold, and certain alternative strategies have historically shown lower correlation with equities during periods of acute stress. Combining these with options hedges can create a more resilient portfolio structure. You can explore the range of investment products available through Longbridge's products overview to understand your diversification options.

Regular Review and Adjustment

Hedging positions require ongoing monitoring. Options should be reviewed regularly considering portfolio changes, market conditions, and time to expiration. If conditions shift materially, positions may need to be rolled to new strikes or expiration dates.

Frequently Asked Questions

What is a black swan event in investing?

A black swan event is a rare, highly unpredictable occurrence that causes severe disruption to financial markets. The term was popularised by Nassim Nicholas Taleb and is characterised by three features: extreme rarity, severe impact, and the appearance of being predictable in hindsight. Market examples include the 2008 financial crisis and the March 2020 COVID-19 market crash.

Can options fully protect a portfolio against a black swan event?

Options may provide protection during a black swan event, but they cannot guarantee full protection. Far out-of-the-money put options and VIX options provide the strongest protection in sudden, severe crashes. However, they may provide limited benefit during gradual declines and have carrying costs that reduce returns during normal market conditions.

How much should I allocate to black swan protection strategies?

There is no universal answer, as allocation depends on your overall portfolio size, risk tolerance, and investment objectives. One common approach is to allocate 1% to 3% of portfolio value to tail risk hedging instruments at any one time. The goal is to balance the cost of protection against its benefit, not to eliminate all risk.

When is the right time to buy put options as a hedge?

Options are generally less expensive during periods of lower market volatility. Buying protection when volatility is calm tends to be more cost-effective than purchasing during periods of heightened fear, when premiums are already elevated. Maintaining ongoing, rolling hedge positions is one approach used to avoid timing dependency.

Are there simpler alternatives for retail investors?

Some exchange-traded funds (ETFs) incorporate tail risk hedging strategies directly within their structure, providing exposure to protection without requiring active options management. However, investors should assess the fees, structure, and specific approach of any such product, and understand whether it suits their risk profile and objectives.

Conclusion

Black swan events are a permanent feature of financial markets. While predicting them is not possible, preparing for them is. Options, particularly put options and VIX-linked instruments, can be used as part of a risk management framework when extreme events occur. The key is understanding the costs, when these tools work best, and how to integrate them within a broader risk management approach.

Effective black swan protection is not about eliminating risk — it is about managing it so you remain invested and can recover when extreme volatility subsides.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.