Box Spread Risk-Free Arbitrage: The Retail Reality

Box spreads promise risk-free arbitrage profits, but retail traders face transaction costs, execution challenges, and fierce institutional competition. Learn the reality behind the theory.

TL;DR: Box spread options combine four options positions to create what appears to be risk-free arbitrage, but retail traders face significant practical barriers. Transaction costs, execution delays, institutional competition, and assignment risks often eliminate theoretical profits, making box spreads more suitable for professional traders than individual investors.

The promise of "risk-free" profits sounds too good to be true in financial markets—and for retail traders attempting box spread arbitrage, it usually is. While box spread options represent an elegant application of put-call parity that can theoretically lock in returns, the reality differs dramatically from textbook scenarios.

According to the Chicago Board Options Exchange (CBOE), institutional traders execute box spread trades worth hundreds of millions of dollars regularly. However, the same opportunities often prove unprofitable for retail traders facing wider spreads, higher commissions, and slower execution speeds.

Whether exploring advanced strategies or curious about options strategies, understanding the gap between theoretical and practical arbitrage is essential for informed decision-making.

What Are Box Spread Options?

A box spread is a complex options strategy that combines four positions on the same underlying asset with identical expiration dates. The strategy creates a synthetic long position and a synthetic short position simultaneously, effectively neutralising directional market risk while locking in a predetermined payout at expiration.

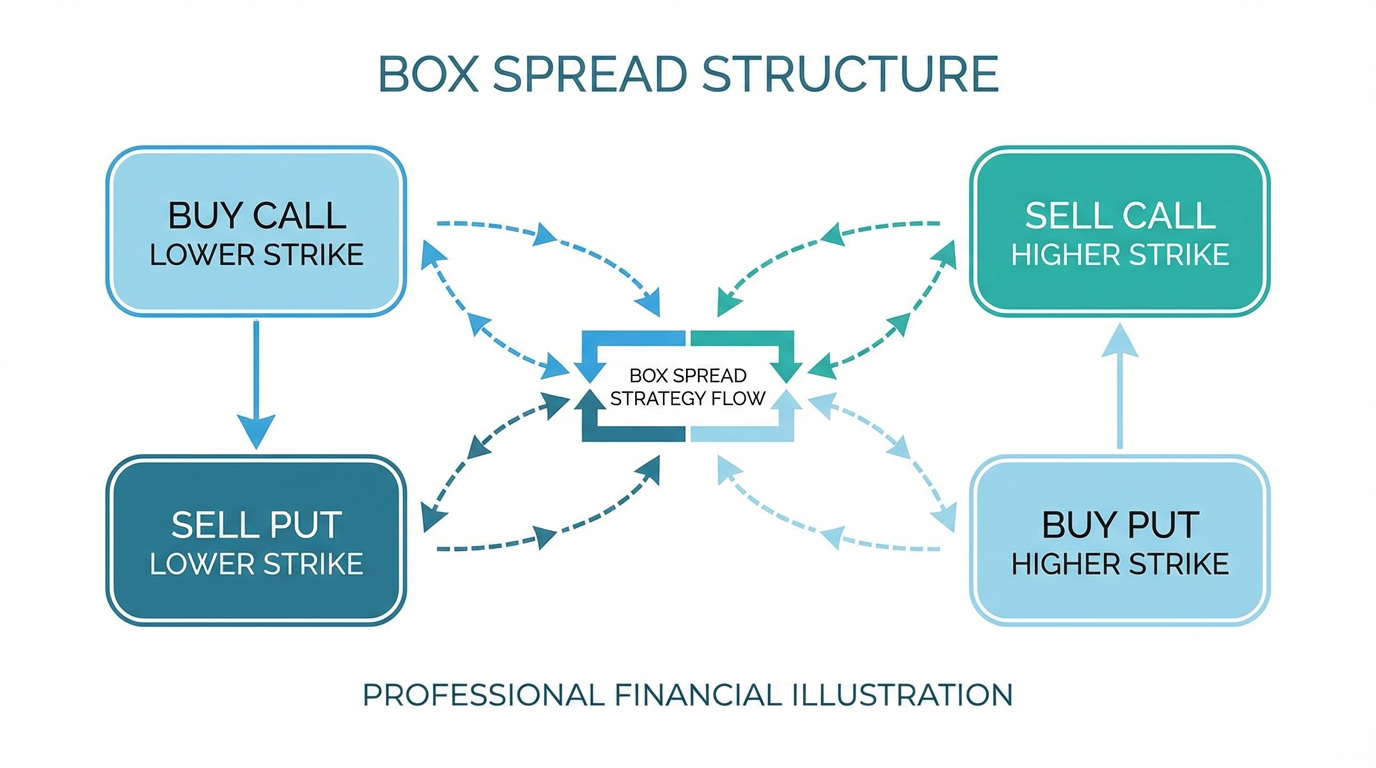

The four components of a long box spread are:

Buy a call at a lower strike price (Strike A)

Sell a call at a higher strike price (Strike B)

Buy a put at the higher strike price (Strike B)

Sell a put at the lower strike price (Strike A)

This combination forms two vertical spreads: a bull call spread (long lower strike call, short higher strike call) and a bear put spread (long higher strike put, short lower strike put). When properly structured, these spreads work in tandem to theoretically guarantee a fixed payout equal to the difference between the two strike prices.

Put-Call Parity and Synthetic Positions

Box spreads exploit put-call parity, a fundamental principle establishing the relationship between call prices, put prices, and strike prices. The long call and short put at one strike create a synthetic long position, while the short call and long put at another strike create a synthetic short position. The result converges to the difference between strikes regardless of the underlying price at expiration.

Understanding Box Spread Structure

To illustrate how box spreads function, consider a practical example using options on a stock trading at $100.

Example Setup:

Strike A (lower): $95

Strike B (higher): $105

All options expire on the same date

The Four Positions:

Buy the $95 call for $8

Sell the $105 call for $3

Buy the $105 put for $7

Sell the $95 put for $2

Net Cost: (8 - 3) + (7 - 2) = $10 per share, or $1000 per contract

Target Payout: The difference between strikes = 105 - 95 = $10 per share, or $1000 per contract

In this theoretical example, the net cost equals the expiration value, representing the fair value with no arbitrage opportunity. However, pricing inefficiencies occasionally create situations where the net cost falls below the expiration value, generating a risk-free profit—at least in theory.

When Box Spreads Create Arbitrage Opportunities

Arbitrage opportunities emerge when options are mispriced relative to their theoretical values. Establishing a long box spread for less than the strike price difference locks in guaranteed profit, while a short box spread becomes profitable when collecting more premium than the difference.

These mispricings typically occur during high volatility or temporary market inefficiencies. However, sophisticated algorithms constantly scan for such opportunities, which rarely persist for more than seconds.

The Retail Reality: Why Box Spreads Rarely Work for Individual Traders

While the mathematics of box spreads appear straightforward and the profits seemingly guaranteed, retail traders face substantial practical obstacles that institutional traders can largely avoid.

Transaction Costs: The Profit Killer

Box spreads are often called "alligator spreads" because commissions can devour the entire profit. Since the strategy requires four separate options transactions, commission costs multiply quickly.

Consider a theoretical arbitrage profit of fifty cents per share. If your broker charges $1 per contract per leg, the total commission bill becomes $4—eight times the theoretical profit.

Beyond commissions, bid-ask spreads represent another hidden cost. When executing four positions simultaneously, you pay the ask for long positions and receive the bid for short positions. A bid-ask spread of just ten cents on each leg adds forty cents of slippage per share, eroding profitability.

Execution Speed and Slippage

Box spread arbitrage requires precise, simultaneous execution of all four legs. Even slight delays can expose you to market movement that eliminates arbitrage profit.

Institutional traders use sophisticated algorithms and direct market access to execute multi-leg strategies in microseconds. Retail traders experience slower execution on standard platforms. Market makers and high-frequency trading firms identify and eliminate arbitrage opportunities almost instantaneously—most disappear in less than one second.

Early Assignment Risk

American-style options can be exercised anytime before expiration, creating early assignment risk. If one short option is assigned early—particularly on stocks going ex-dividend or deeply in-the-money options—you suddenly hold an unhedged stock position, transforming risk-free arbitrage into a directional bet. The cost of managing this unexpected position often exceeds any arbitrage profit.

European-style options eliminate this risk but are primarily available on broad indices where arbitrage opportunities are rarer due to intense institutional competition.

Box Spreads as Synthetic Loans

Beyond arbitrage, box spreads serve as synthetic financing tools. A long box spread involves paying cash upfront and receiving a predetermined amount at expiration—similar to lending money. A short box spread collects cash upfront and pays a fixed amount at expiration—similar to borrowing.

According to the CBOE's analysis, institutional traders use box spreads on the S&P 500 Index as financing tools, sometimes achieving implied interest rates close to Treasury rates. However, this application remains inaccessible to retail traders due to execution and cost barriers.

Comparing Box Spreads with Other Options Strategies

A bull call spread involves buying a lower strike call and selling a higher strike call, profiting when the underlying rises. Box spreads combine a bull call spread with a bear put spread at the same strikes, creating a market-neutral position that eliminates directional risk.

Iron condors combine bull put and bear call spreads at different strikes, profiting from low volatility but carrying significant risk if prices move sharply. Box spreads differ fundamentally because they theoretically guarantee a fixed payout regardless of price movement, making them an arbitrage tool rather than a volatility strategy.

Regulatory Considerations

Regulatory position limits may also restrict the number of options contracts on a single underlying asset. Box spreads involve four positions, quadrupling the contracts required compared to simple positions.

Getting Started with Options Trading

Retail investors often prioritize foundational approaches when comparing box spreads . Simple strategies like covered calls, protective puts, and basic vertical spreads offer clearer risk-reward profiles without execution complexity and cost challenges.

Longbridge provides Options trading in United States markets, giving Singapore-based investors access to liquid options on major indices and individual stocks.

Tip: Before attempting complex strategies like box spreads, gain experience with simpler options trades. Understanding how calls and puts behave provides the foundation necessary to evaluate multi-leg strategies.

Frequently Asked Questions

Is box spread arbitrage truly risk-free?

Box spread arbitrage is theoretically risk-free if held to expiration with European-style options and executed at favorable prices. However, practical risks include early assignment (with American-style options), execution delays, transaction costs, and the possibility of legs not filling at expected prices. These factors can turn theoretical risk-free profits into actual losses for retail traders.

Can retail traders profit from box spreads?

While not impossible, retail traders face significant disadvantages compared to institutional traders. Transaction costs, slower execution speeds, wider bid-ask spreads, and intense competition from sophisticated algorithms make consistent box spread profits extremely difficult for individual investors. Most arbitrage opportunities disappear in less than one second.

How much capital do you need for box spread trading?

Capital requirements depend on strike prices and broker margin requirements. A box spread with a ten-dollar strike difference requires approximately $1000per contract at fair value. However, given minimal profit potential and high execution costs, substantial capital is needed to generate meaningful returns.

What are the best alternatives to box spreads for retail traders?

Retail traders typically benefit more from directional or volatility-based strategies like bull call spreads, bear put spreads, iron condors, or covered calls. These strategies offer clearer risk-reward profiles, lower transaction costs, and fewer execution challenges compared to arbitrage strategies. They also align better with the analytical and market timing skills that retail traders can develop through experience.

Do any brokers specialize in box spread execution?

Most major brokers support multi-leg options strategies including box spreads, but few optimize for arbitrage execution. Institutional traders use specialized firms with direct market access and sophisticated algorithms. Retail traders should carefully evaluate commission structures and execution quality before attempting complex strategies.

The choice of which tool to utilize depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.