SPX vs SPY Options: Which Should You Trade?

SPX and SPY options both track the S&P 500 but differ in exercise style, settlement, contract size, and tax treatment. Learn which suits your strategy.

TL;DR: SPX (S&P 500 Index options) and SPY (SPDR S&P 500 Exchange-Traded Fund options) both give exposure to the same index but differ significantly in contract size, settlement, exercise style, and tax treatment. SPX is often used by traders seeking capital efficiency and no early assignment risk; SPY offers smaller contract sizes with tighter spreads, which some smaller accounts prefer. Understanding these differences helps you match the instrument to your strategy.

If you trade options on the S&P 500 index, you will inevitably face the same question: should you use SPX or SPY options? Both instruments track the same benchmark, yet they behave differently in ways that directly affect your position sizing, execution costs, risk management, and potential tax obligations. This article breaks down the key differences so you can make an informed decision based on your own circumstances.

Whether you are new to US options markets or refining an existing strategy, these distinctions are worth understanding before you trade. Explore the full range of investment products available on Longbridge, including US options, to see how these instruments fit within a broader portfolio.

What Are SPX and SPY Options?

Before comparing the two, it helps to understand exactly what each instrument represents.

SPX: S&P 500 Index Options

SPX refers to options written directly on the S&P 500 index itself. Because you cannot buy or sell an index like a stock, SPX options are always cash-settled — there is no underlying share to deliver. These contracts are listed on the Chicago Board Options Exchange (CBOE) and are among the more heavily traded index derivatives.

SPY: SPDR S&P 500 ETF Options

SPY is an exchange-traded fund (ETF) that tracks the S&P 500. Unlike SPX, SPY can be bought and sold like a regular share. Options on SPY follow American-style exercise rules and, if exercised or assigned, result in the physical delivery of SPY shares. SPY trades at roughly one-tenth of the SPX index level, making individual contracts significantly smaller in notional value.

Key Structural Differences

The structural differences between SPX and SPY options are the foundation of every other comparison. Getting these right matters before you place your first trade.

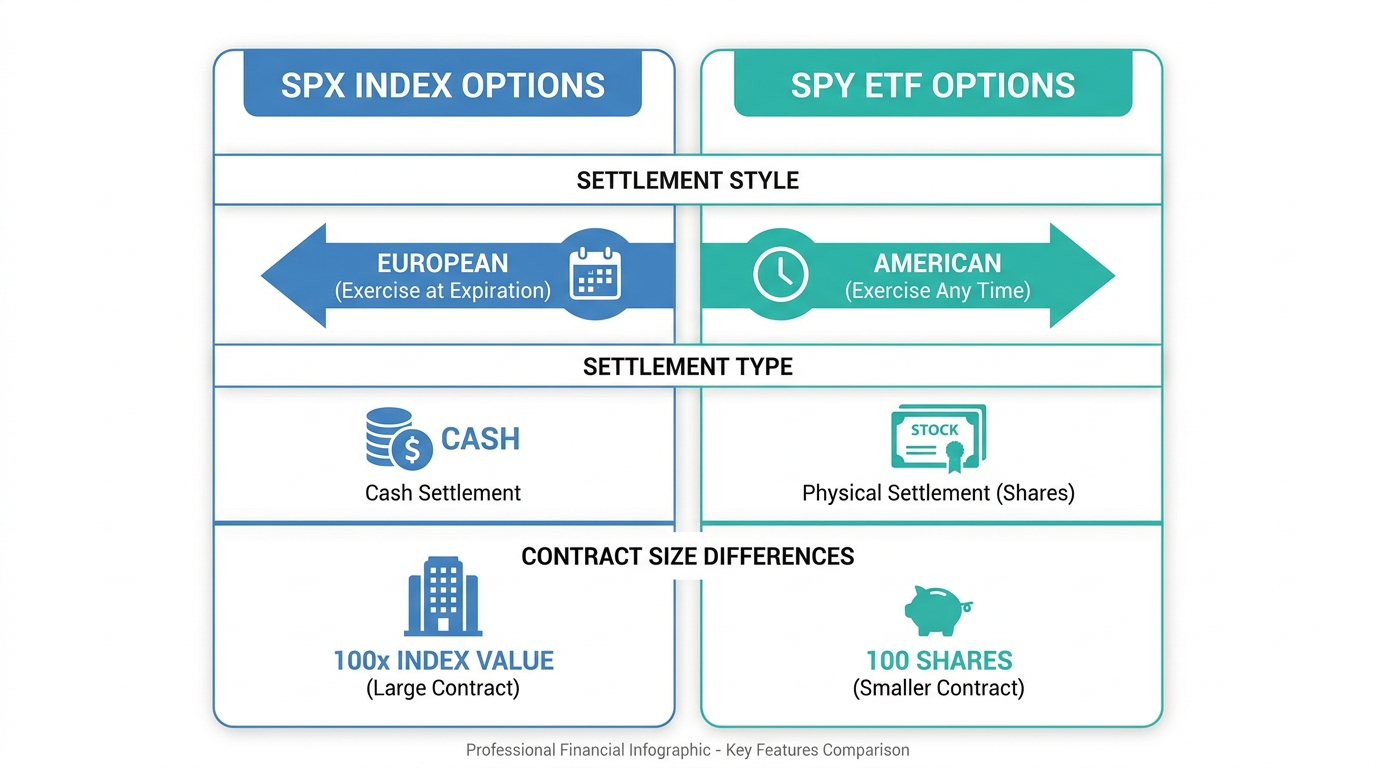

Exercise Style: European vs American

SPX options follow European-style exercise rules. This means the option can only be exercised at expiration — not before. Because there is no early exercise, there is also no early assignment risk for the option seller.

SPY options use American-style exercise. The holder can exercise at any point before expiration. For traders who sell options or run multi-leg strategies, this introduces early assignment risk on in-the-money options — particularly around ex-dividend dates, when SPY call holders may exercise early to capture the upcoming quarterly dividend.

Settlement: Cash vs Physical Shares

When an SPX option expires in the money, the difference between the strike price and the settlement value is paid in cash. No shares change hands. For SPY options, in-the-money contracts at expiration (or upon early exercise) result in the actual delivery of SPY shares. Being unexpectedly assigned 100 shares — or more — can affect your margin, buying power, and overall position management, especially in volatile markets.

Contract Size and Capital Requirements

One SPX contract represents a notional value approximately 10 times that of one SPY contract. For larger portfolios, SPX offers capital efficiency: the same market exposure requires fewer contracts, reducing commission costs. For smaller accounts or those new to options, SPY's lower notional value per contract provides more granular position sizing.

Tip: SPY's reduced contract size allows for more granular position sizing, as exposure can be adjusted without committing to the larger notional value of a single SPX contract.

Tax Considerations: The Section 1256 Advantage

Tax treatment is one of the more significant differences between SPX and SPY options, and it is often overlooked by newer traders.

SPX and Section 1256 Contracts (US Tax Rules)

In the United States, SPX options are classified as Section 1256 contracts under the Internal Revenue Code. Gains and losses are subject to a blended tax rate: 60% treated as long-term capital gains and 40% as short-term, regardless of holding period. For active traders turning over positions frequently, this blended treatment can produce a lower effective tax rate than standard short-term rates. Section 1256 contracts also carry a loss carryback provision and are exempt from wash-sale rules.

SPY and Standard Capital Gains Rules

SPY options do not qualify for Section 1256 treatment. Short-term gains are taxed at the holder's ordinary income rate, and wash-sale rules apply. For traders who actively turn over positions, particularly those using zero days to expiration (0DTE) strategies, this distinction can result in a meaningfully different tax outcome over a full year.

Important: Tax rules differ between countries. Singapore-based investors trading US options should consult a qualified tax adviser regarding their obligations under both US and Singapore tax rules. The above reflects general US tax principles as reported by US-based financial sources.

Liquidity and Execution Quality

Both instruments are highly liquid, but they differ in ways that matter during execution.

Bid-Ask Spreads

SPY options are among the more actively traded options contracts, with very tight bid-ask spreads that reduce the cost of entering and exiting positions. SPX options are also liquid, but spreads tend to be wider, particularly on complex multi-leg structures. Limit orders are generally advisable when trading SPX.

Volume and Open Interest

For shorter-dated options, both instruments attract substantial volume. For longer-dated options, SPY consistently records higher open interest, making it easier to find counterparties. Institutional participants are more active in SPX, while retail traders tend to concentrate more in SPY.

Dividend Impact on Options Pricing

SPX, as a pure index, does not pay dividends, so dividend events have no direct effect on SPX options pricing.

SPY, as an ETF, distributes quarterly dividends to shareholders of record. Around ex-dividend dates, the SPY share price typically drops by the dividend amount. Market makers price this into options in advance: call options on SPY tend to be cheaper and put options more expensive in the period before an ex-dividend date. Traders who are short SPY calls also face an elevated risk of early exercise around these dates, as call holders may exercise to capture the dividend rather than selling the option.

Choosing the Right Instrument for Your Strategy

The decision depends on your account size, trading strategy, tax circumstances, and tolerance for assignment risk. The table below summarises the key trade-offs:

| Factor | SPX | SPY |

|---|---|---|

| Exercise Style | European (no early assignment) | American (early assignment possible) |

| Settlement | Cash | Physical shares |

| Contract Size | ~10x SPY | Smaller, more accessible |

| Tax Treatment (US) | Section 1256 (60/40 blended rate) | Standard capital gains |

| Bid-Ask Spreads | Wider | Tighter |

| Dividend Effect | None | Quarterly impact |

| Commonly Used By | Larger accounts, tax-conscious traders | Smaller accounts, flexible positioning |

Experienced traders frequently use both. SPX is often used for high-volume premium selling strategies where tax efficiency and cash settlement are factors. SPY is often used for smaller tactical positions or accounts where lower notional value per contract is a meaningful constraint.

Staying informed about US market movements, including US trading hours in Singapore time, can help you monitor relevant activity in real time.

Risk Considerations

Options trading, whether using SPX or SPY, involves significant risk. The value of options can decline rapidly, and traders can lose the entire premium paid. Selling options introduces potentially uncapped risk on uncovered positions, and leverage magnifies both gains and losses.

Before trading, you should understand the mechanics of the instrument, the maximum potential loss of your strategy, and how the position fits within your overall risk management framework. A stock screener and broader market insights can support this analysis.

Important: Past performance is not indicative of future results. Options involve complex risks including time decay, volatility changes, and market gaps. Always maintain a clearly defined risk management plan.

Frequently Asked Questions

Is SPX or SPY better for 0DTE options trading?

SPX is commonly preferred for zero-days-to-expiration (0DTE) strategies because of its cash settlement and European exercise style, which eliminate early assignment risk at expiration. SPY can also be used for 0DTE trading, particularly by traders with smaller accounts, due to its tighter spreads and lower contract notional value. Both carry substantial risk in short-dated options.

Can Singapore-based investors trade both SPX and SPY options?

Yes, Singapore-based investors with access to US options markets can trade both instruments, subject to account eligibility and their broker's product availability. Longbridge provides options trading in US markets. Tax treatment for Singapore residents may differ from US residents, so consulting a qualified adviser is strongly recommended.

What does cash settlement mean for SPX options?

When an SPX option expires in the money, the intrinsic value is paid in cash to the holder, and no shares are exchanged. For example, if a call option expires with 20 index points of intrinsic value, the holder receives the cash equivalent (20 × USD 100 multiplier = USD 2,000) without any stock transaction occurring.

What is early assignment risk and why does it matter for SPY options?

Early assignment occurs when an option buyer exercises their contract before the expiration date. With American-style SPY options, a trader who has sold a call or put can be assigned unexpectedly, resulting in an obligation to deliver or purchase shares. This risk is particularly relevant near SPY ex-dividend dates. SPX options, being European-style, cannot be exercised before expiration, eliminating this risk entirely.

Conclusion

SPX and SPY options both provide exposure to the S&P 500, but they are not interchangeable. The choice involves genuine trade-offs across contract size, exercise style, settlement, liquidity, dividend sensitivity, and tax treatment. Neither is universally superior; the right choice depends on your account size, strategy, and circumstances.

Smaller accounts and traders prioritising tight spreads may find SPY more practical. Larger accounts focused on tax efficiency, cash settlement, and reduced assignment risk will often lean towards SPX. Many experienced traders use both, matching each instrument to the specific strategy at hand.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.