Currency Hedging for Multi-Market Investors in Singapore

Currency hedging helps Singapore investors protect multi-market portfolios from exchange rate volatility. Explore the instruments, costs, and practical steps to manage FX risk across SGD, USD, and HKD.

TL;DR: Currency hedging helps Singapore investors protect their multi-market portfolios from exchange rate volatility when trading across Singapore, US, and Hong Kong markets. This guide explains the key hedging instruments, their costs, and practical considerations for retail investors managing foreign currency exposure.

When you invest across multiple markets — Singapore, the United States, and Hong Kong — your returns are not driven solely by how well your stocks or exchange-traded funds (ETFs) perform. Exchange rate movements between the Singapore dollar (SGD), US dollar (USD), and Hong Kong dollar (HKD) can significantly affect what you receive when converting gains back to SGD. Currency hedging is the practice of managing this foreign exchange (FX) risk so that currency fluctuations do not erode your investment returns.

For Singapore investors actively trading across global markets through platforms such as Longbridge, understanding currency hedging is an increasingly important part of portfolio management. This guide covers the fundamentals, key instruments, and trade-offs you should consider before implementing a hedging strategy.

What Is Currency Risk and Why Does It Matter?

Currency risk — also called FX risk — arises whenever you hold an asset denominated in a currency other than your home currency. For a Singapore-based investor, any position in USD-denominated US stocks or HKD-denominated Hong Kong equities carries inherent currency risk.

The Two-Return Problem

When you invest internationally, your overall return has two components: the performance of the underlying asset, and the movement of the foreign currency relative to SGD. If a US stock rises 10% in USD terms but the USD weakens 8% against SGD over the same period, your net gain in SGD terms is considerably smaller. Conversely, if the USD strengthens, your SGD-denominated returns may exceed the asset's local performance.

This dual-return dynamic means currency movements can amplify or reduce your investment outcome, independently of how well you selected your underlying securities.

Why Singapore Investors Are Particularly Exposed

Singapore investors trading in US and Hong Kong markets face exposure to two foreign currency pairs: SGD/USD and SGD/HKD. While the HKD is pegged to the USD within a narrow band (maintained by the Hong Kong Monetary Authority), USD/SGD can experience meaningful fluctuations driven by US Federal Reserve policy, global risk sentiment, and Singapore's monetary policy managed by the Monetary Authority of Singapore (MAS).

According to DBS Group, as of early 2026, US dollar concentration risk and volatility have made currency hedging a prudent consideration for investors with significant USD exposure, with the bank noting that funding costs in Asian currencies remain relatively low compared to US dollar rates.

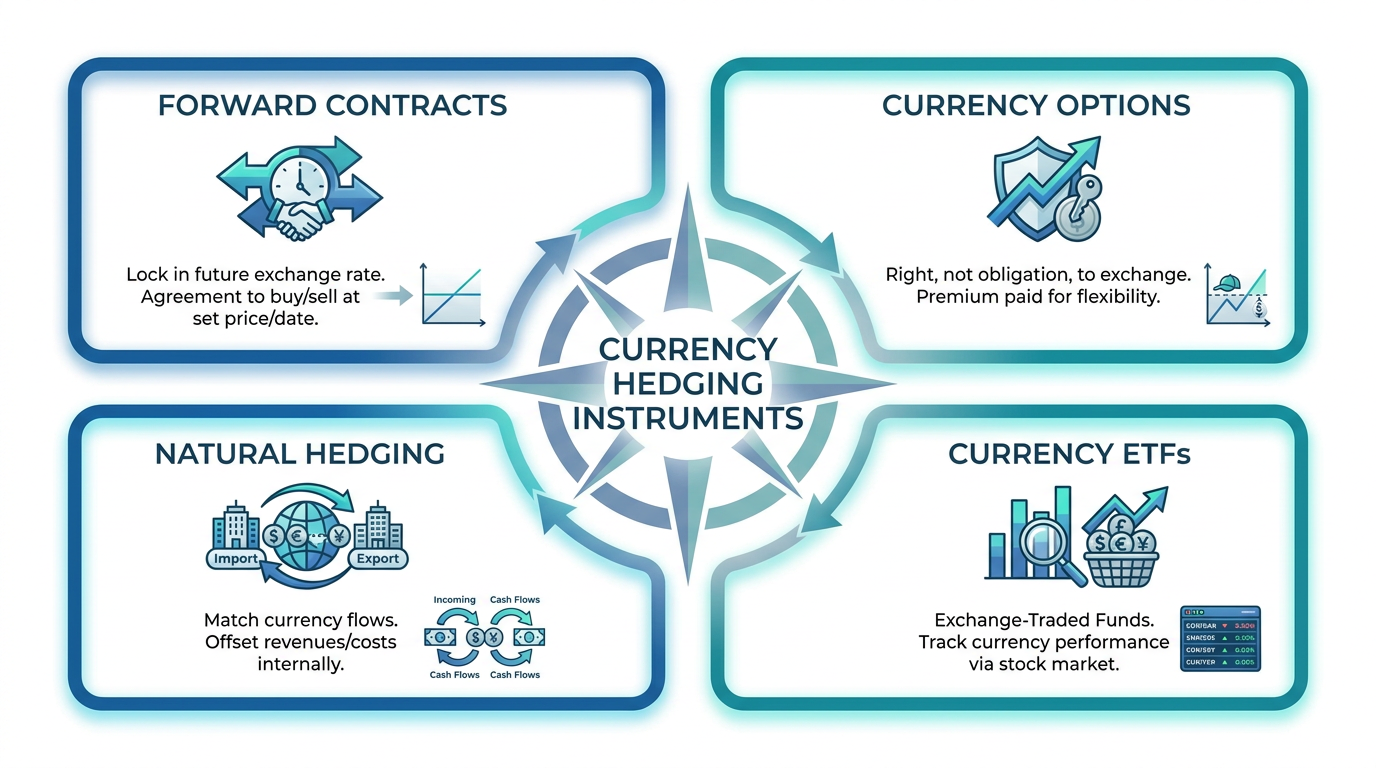

Key Currency Hedging Instruments Explained

Currency hedging can be implemented through several instruments, each with distinct mechanics and costs.

Forward Contracts

A forward contract is an agreement to exchange a specified amount of one currency for another at a predetermined rate on a future date. A Singapore investor expecting to repatriate USD proceeds in three months could lock in today's exchange rate, eliminating uncertainty about what SGD they will receive. Forward contracts are widely used by institutional investors; for retail investors, access depends on the broker and may require minimum transaction sizes.

Currency Options

A currency option gives the holder the right — but not the obligation — to exchange currency at a set rate before a specified expiry date. Unlike forward contracts, options let investors benefit if the exchange rate moves in their favour, while still limiting downside if it moves against them. This flexibility comes at a cost: the option premium paid upfront reduces overall return even if the hedge is not ultimately exercised.

Options are available to investors who trade derivatives through their brokerage account. Longbridge provides options trading for US markets, which opens possibilities for those with the appropriate knowledge and risk appetite.

Note: Options involve significant complexity and carry risks including the potential loss of the full premium paid. They are not suitable for all investors. Ensure you fully understand how options work before using them for hedging purposes.

Currency-Hedged ETFs and Fund Share Classes

For investors who prefer a simpler approach, currency-hedged ETFs and hedged share classes of unit trusts offer a more accessible route. These products incorporate hedging at the fund level, with the fund manager managing FX exposure on your behalf. The hedging cost is typically embedded in the fund's expense ratio or reflected in the performance difference between hedged and unhedged versions.

According to Endowus, hedged share classes seek to minimise the impact of exchange rate movements between the fund's base currency and the investor's home currency, making fund performance more closely reflect underlying asset returns.

Natural Hedging

Natural hedging involves structuring a portfolio so that assets in the same foreign currency naturally offset each other, reducing net exposure without derivatives. For retail investors, opportunities are generally limited, but awareness of existing currency exposures can inform investment decisions and reduce unnecessary hedging costs.

The Real Cost of Currency Hedging

Currency hedging is not free, and understanding the costs involved is essential before implementing any strategy.

Interest Rate Differentials

The primary cost driver is the interest rate differential between the two currencies. When you enter a forward contract or rolling hedge, the locked-in rate is adjusted by "forward points" reflecting this differential. If the currency you are hedging into (SGD) has a lower interest rate than the one you are hedging away from (USD), you may pay a "negative carry" cost that reduces net returns.

As reported by DBS Group, Singapore's overnight rate (the Singapore Overnight Rate Average, or SORA) was approximately 1% to 1.3% per annum in early 2026, while US rates remain higher. For Singapore investors hedging USD exposure back to SGD, this differential may result in a hedging cost that should be weighed against the benefit of reduced FX volatility.

Ongoing Management

Active hedging programmes require periodic rollover of contracts, which adds administrative complexity. This is one reason many retail investors choose hedged fund products rather than managing their own positions. The relevant question: does the reduction in currency volatility justify the hedging cost for your investment horizon?

Hedged Versus Unhedged: Practical Considerations

Whether to hedge is rarely a binary decision. Many investors operate on a spectrum, partially hedging their exposure based on risk tolerance, investment horizon, and market conditions.

Hedging tends to add value when currency volatility is high relative to expected asset returns, or when your investment horizon is short. For fixed income investments in particular, where yields may be modest, a large adverse currency move can turn a positive return into a loss.

Over longer investment horizons, research from Macquarie Asset Management suggests that performance differences between hedged and unhedged global equity investments can diminish over time. Unhedged exposure may also provide a partial diversifier: in some historical periods, the SGD has weakened during global downturns, partially offsetting declines in SGD-denominated assets.

Tip: There is no universally correct hedging ratio. Consider your investment horizon, the proportion of your portfolio in foreign currency assets, and your tolerance for currency-driven fluctuations when deciding how much to hedge.

Rather than evaluating hedging at the individual asset level, consider your total currency exposure across your portfolio. Investors trading Singapore stocks, US equities, and Hong Kong-listed securities can use market data and insights to map aggregate currency exposure and identify natural offsets that reduce the need for active hedging.

Practical Steps to Manage Currency Risk

You do not need to implement complex derivatives strategies to manage currency risk. The following practical steps are accessible to most retail investors.

Step 1: Map Your Currency Exposure. Tally your SGD, USD, and HKD positions to understand total exposure to each currency pair.

Step 2: Assess Your Investment Horizon. For short-term holdings, currency movements can be substantial relative to expected returns. For longer-term investments, short-term FX volatility typically has less impact on overall performance.

Step 3: Evaluate Hedging Costs. Calculate the approximate cost before proceeding. For hedged fund products, compare expense ratios between hedged and unhedged share classes. For forward contracts, understand the forward points applicable to your currency pair and tenor.

Step 4: Consider the Available Instruments. Different approaches vary in expertise required, account type, and cost. Hedged ETFs offer relative simplicity, while options strategies involve greater complexity. Explore the investment products available on Longbridge to see the range of instruments accessible.

Step 5: Review Regularly. Currency hedges are not set-and-forget. Exchange rates, interest rate differentials, and portfolio composition all change over time.

Frequently Asked Questions

What is currency hedging in simple terms?

Currency hedging is a way of protecting the value of your investments from being affected by changes in exchange rates. Think of it as a form of insurance: you give up some potential gains if exchange rates move in your favour, in exchange for protection if they move against you.

Does currency hedging guarantee a fixed return?

No. Currency hedging reduces the impact of exchange rate fluctuations on your portfolio, but it does not guarantee a specific return. The performance of your underlying investments still depends on market conditions, and hedging costs reduce your net return regardless of outcome.

Is currency hedging suitable for all investors?

Currency hedging involves costs and, for some instruments, significant complexity. Its appropriateness depends on your investment horizon, portfolio size, risk tolerance, and the proportion of holdings in foreign currencies. When unsure, consult a licensed financial adviser.

How does the SGD/USD exchange rate affect Singapore investors in US stocks?

When the USD strengthens against SGD, Singapore investors receive more SGD when converting USD profits, enhancing local currency returns. When the USD weakens, even strong stock performance in USD terms may yield diminished SGD returns. Hedging can reduce this variability.

Conclusion

Currency hedging is a meaningful risk management consideration for Singapore investors trading across multiple markets. Understanding forward contracts, currency options, and hedged fund products — alongside their costs — equips you to make more informed decisions about managing foreign exchange exposure.

The key takeaway is that hedging is not a guaranteed return enhancer; it is a tool for managing volatility and improving the predictability of SGD-denominated outcomes. Whether you choose to hedge, how much, and through which instrument should reflect your investment objectives, time horizon, and cost sensitivity.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.