To be clear, I love $Tesla(TSLA.US) the company. I have huge respect for @elonmusk and all he’s accomplished. He has truly changed the world for the better. My issue with TSLA is valuation, which seems excessive relative to future expected growth.

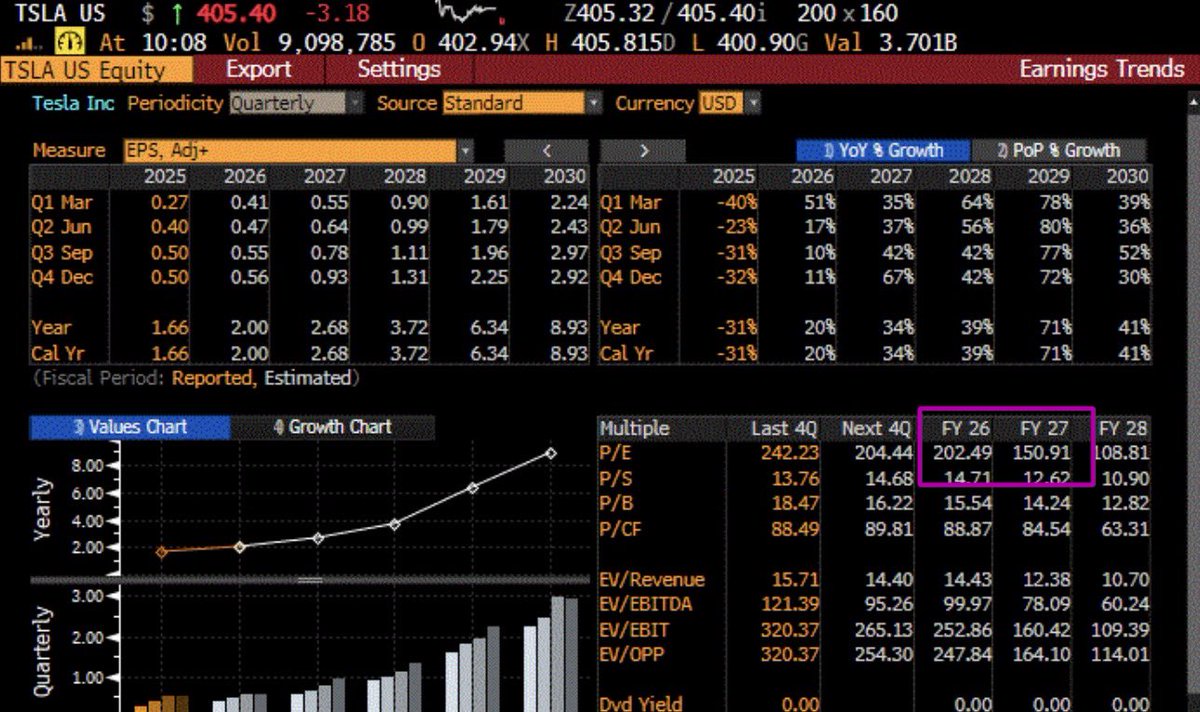

There’s a saying in the investment business: “Love the company. Don’t love the stock.” At 192x 2026 Adj EPS it’s difficult for me to love the stock. I struggle with analysts’ expectations of +40% CGR in Adj EPS between 2026 - 2030 when TSLA EV volume growth (70% of profits) is negative, and there are 5 (soon to be 10) highly credible competitors including $Alphabet - C(GOOG.US) $Amazon(AMZN.US) $NVIDIA(NVDA.US) investing massively in unsupervised autonomy. Many TSLA bulls don’t post their analyses on X so it’s hard to know if they truly believe TSLA will generate excess returns, or are just buying the hype.Probably the #1 question I get is: At what point would we get back into TSLA? We need to see that TSLA will beat its formidable competition in scaling up unsupervised autonomy, so safety monitors need to come out of the cars. We need to see earnings revisions turn positive. And we need valuation to offer at least 2:1 upside/downside. Even using WS 2030 EPS of $9.00, forecasting a 30% earnings growth rate post-2030, applying a 2x PEG we see on other megacap growth names in our universe, and discounting back at a 13.6% cost of equity to reflect TSLA’s 1.6x beta, we get a price target of $325. Great company, but hard to love the stock.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.

Post your comment

No Comments