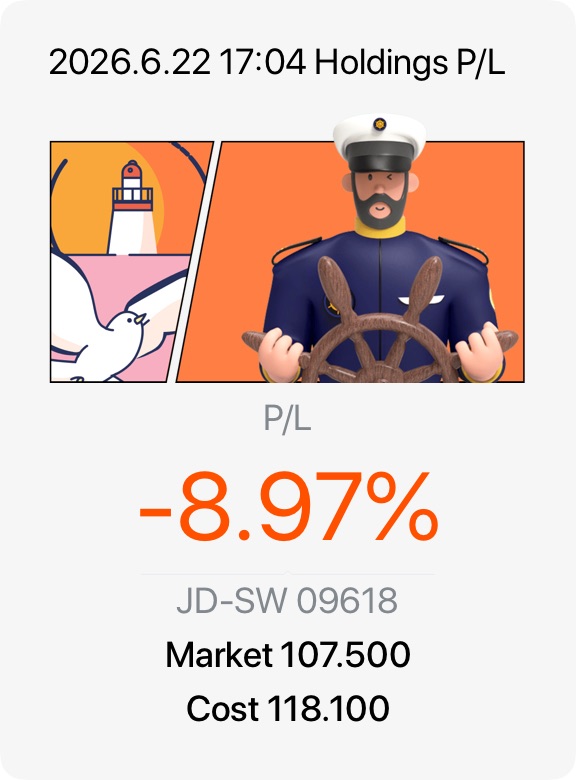

JD is trading at a relatively low forward earnings multiple compared with many large China internet peers. Q1 2026 revenue grew about 5% year-on-year and exceeded analyst expectations.Core retail profitability improved despite intense competition in China’s e-commerce market.JD’s self-owned logistics network remains one of its strongest competitive advantages and is difficult for competitors to replicate. Many long-term investors continue to view this as a key asset.

In short, I see JD as more of a value and recovery play than a high-growth story. The key catalyst to watch over the next few quarters is whether management can continue improving margins while maintaining revenue growth.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.