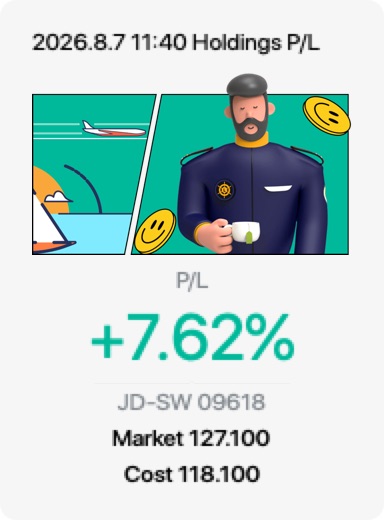

JD.com has officially announced that it will release its second-quarter and first-half 2026 financial results on 13 August 2026, before the U.S. market opens (and after the Hong Kong market closes). Management will also host an earnings conference call to discuss the results and outlook.Analysts continue to highlight JD Logistics and the company's nationwide fulfilment network as one of its strongest competitive moats. Faster delivery and supply chain capabilities remain important differentiators against rivals in China's e-commerce market.JD continues to expand its international business while investing in AI and supply-chain technology to improve operating efficiency. Investors will be looking for updates on these initiatives during the upcoming earnings call.I remain constructive on JD.com over the long term due to its strong balance sheet and healthy cash generation.

Its industry-leading logistics network, which is difficult for competitors to replicate and has reasonable valuation compared with many global internet companies.$JD-SW(09618.HK)