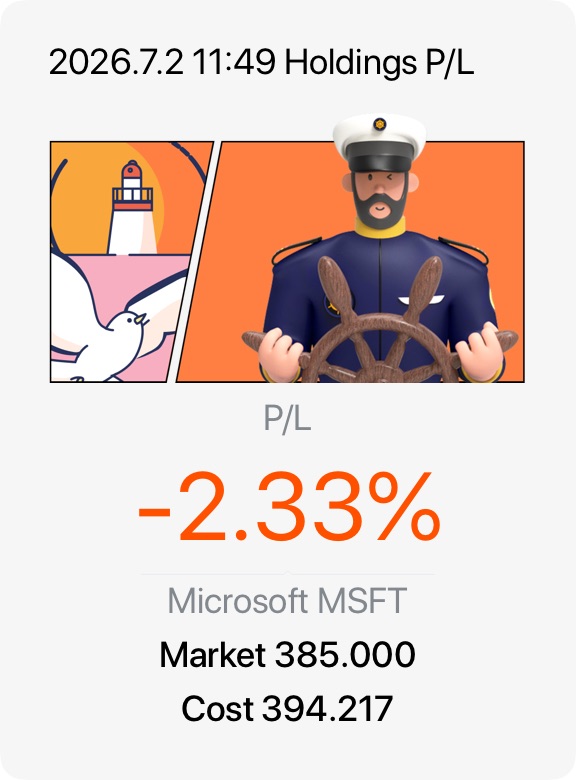

Microsoft ($Microsoft(MSFT.US)) is navigating a stark disconnect between its powerhouse financial performance and a major cooling in investor sentiment. The tech giant recently closed out its worst month since the dot-com era, dragging the stock down roughly 25% over the past year to trade near the $370–$380 range. This sharp correction comes despite stellar fundamentals, including an 18% year-over-year revenue jump to $82.9 billion and a 23% surge in quarterly net income. The primary culprit behind the selloff is Microsoft’s massive capital expenditure, with Wall Street spooked by a staggering $190 billion budget for AI and data center infrastructure that is temporarily squeezing short-term free cash flow.However, long-term investors are increasingly looking at this dip as a prime buying opportunity, as the underlying business engine remains incredibly strong. Microsoft’s actual AI monetization is growing rapidly, with its artificial intelligence segment hitting an annual revenue run rate of $37 billion. More importantly, its commercial remaining performance obligation—essentially its contracted order backlog—has skyrocketed 99% to $627 billion. This massive backlog guarantees highly visible, multi-year revenue streams from enterprises locking in cloud services.Ultimately, the bears are focusing heavily on current data center spending bills, while the bulls are eyeing a historically cheap entry point. At its current valuation, Microsoft is trading at roughly 22x forward earnings, a massive discount compared to its 10-year average of 31x. With Azure cloud growth holding strong at 40% and a heavy backlog already pre-funding its infrastructure buildout, the risk-reward ratio is looking highly attractive for those willing to look past near-term margin anxieties.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.