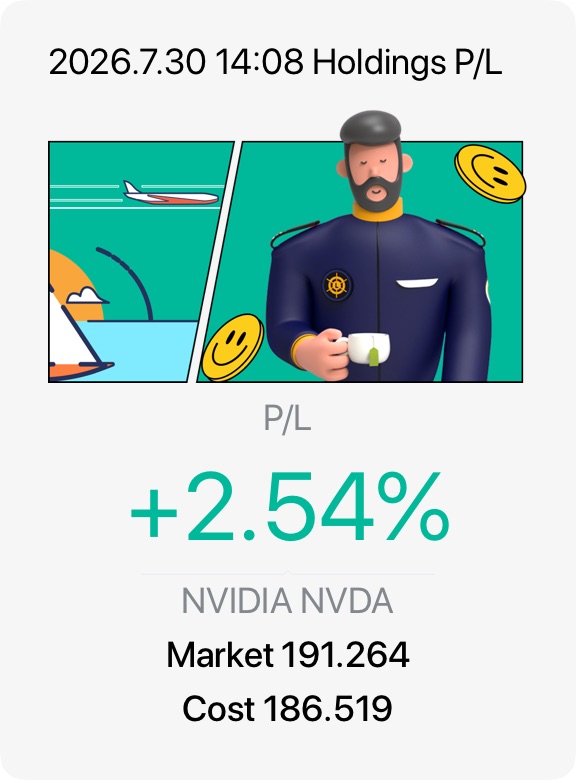

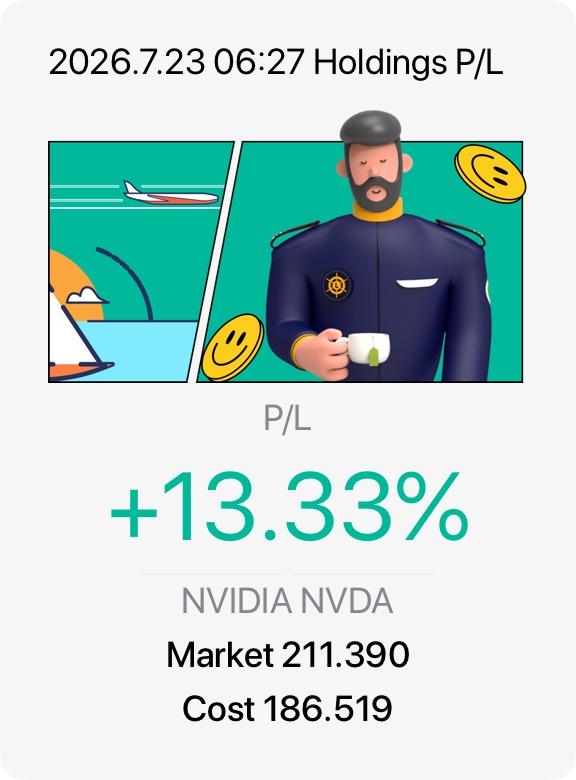

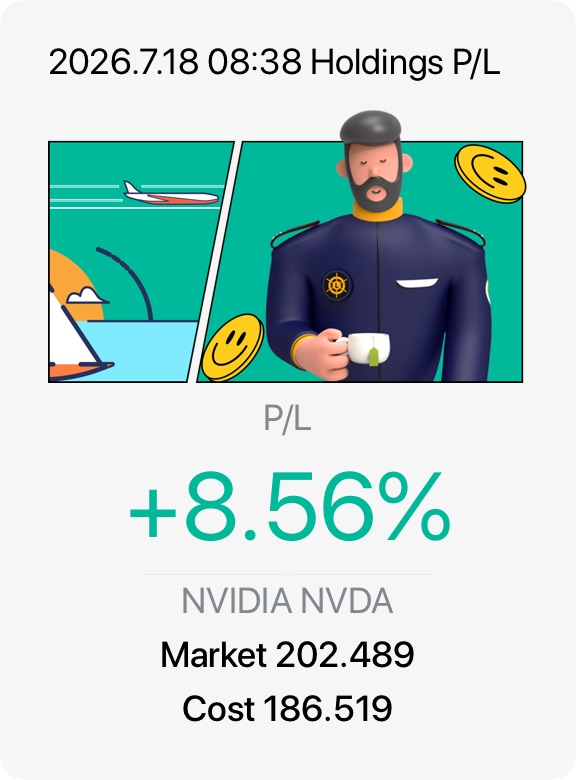

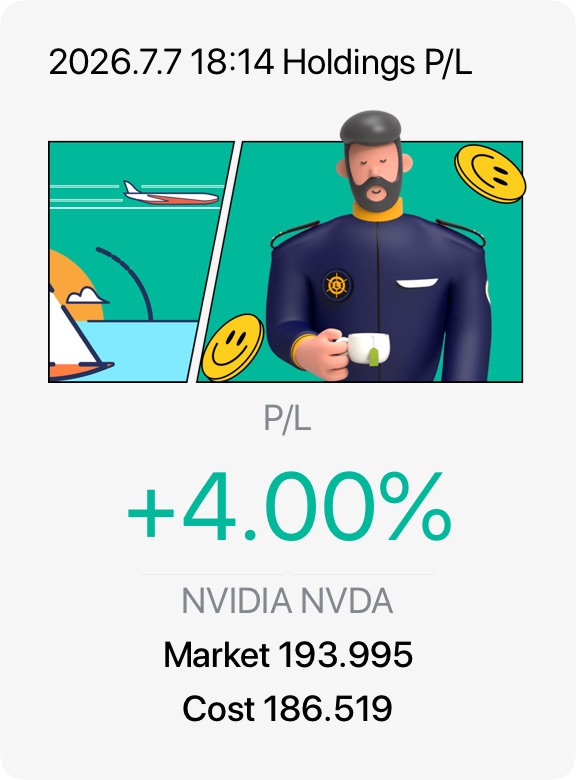

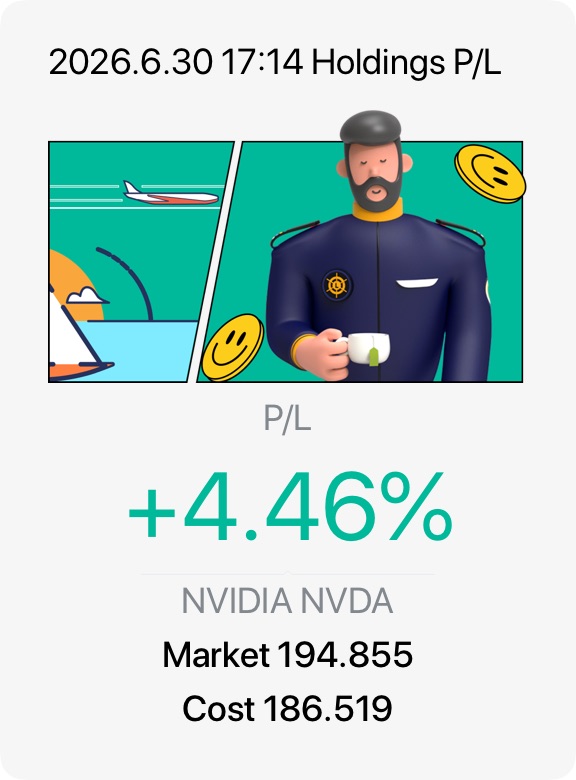

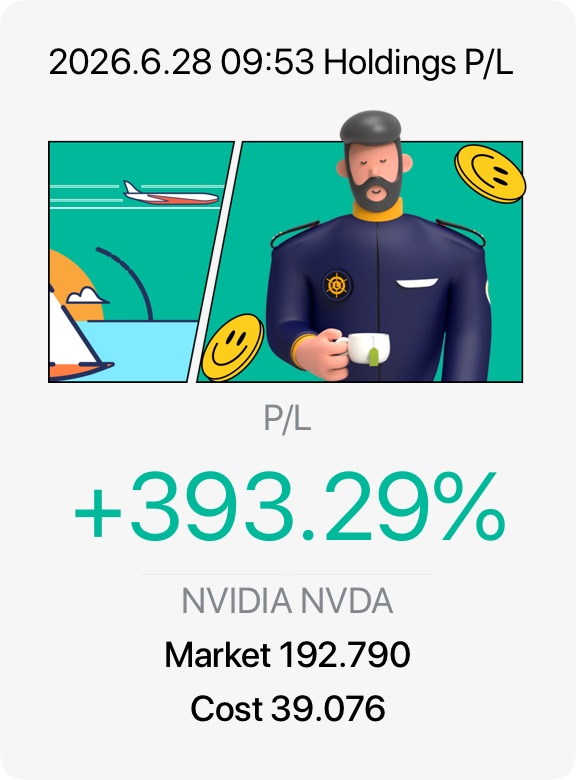

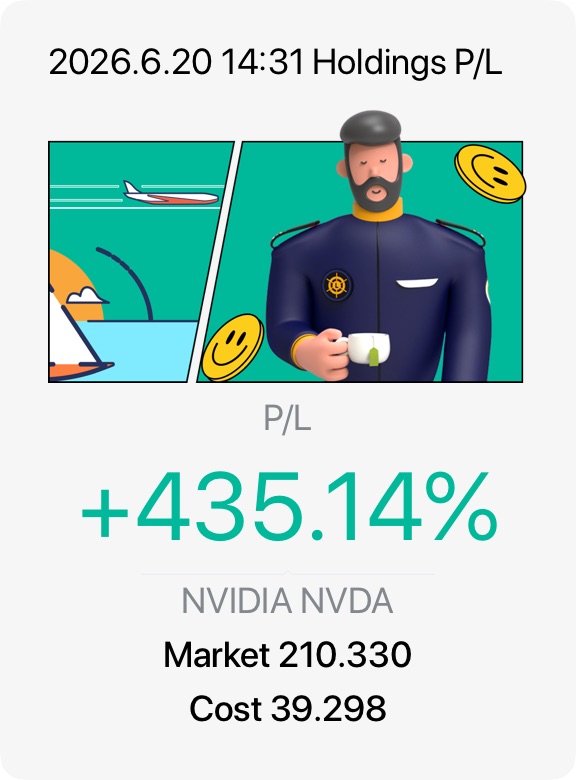

NVIDIA ($NVIDIA(NVDA.US)) continues to dominate the AI chip market, commanding an estimated 80% to 90% market share for enterprise AI hardware. The company’s proprietary CUDA software ecosystem creates a massive competitive moat, locking in developers and making it incredibly difficult for rivals like AMD or Intel to displace them. As tech giants continue their multi-billion-dollar capital expenditure cycles to build out next-generation data centres, demand for NVIDIA’s Blackwell and Hopper architecture remains exceptionally robust.

Financially, NVIDIA remains a powerhouse, though hyper-growth expectations introduce elevated volatility for investors. The company consistently delivers blockbuster revenue growth and exceptional gross margins, driven by its high-margin data centre segment. However, maintaining this parabolic growth trajectory becomes harder as year-over-year comparisons toughen, meaning even slight guidance misses can trigger sharp, short-term stock corrections.

Looking ahead, the main debate centers on the sustainability of global AI infrastructure spending. Bulls argue that we are only in the early innings of a multi-decade technological revolution spanning autonomous vehicles, robotics, and generative AI. Bears caution that if software companies fail to monetize these costly AI features soon, hyperscalers may scale back their hardware orders, leading to a cyclical downturn for chipmakers.