$Oracle(ORCL.US)

High-quality research report, recommended to read through.

Writing a preface for Dolphin Research:

For over a decade, Oracle has been in an awkward position—not in decline, but no longer the best growth asset in the tech industry.

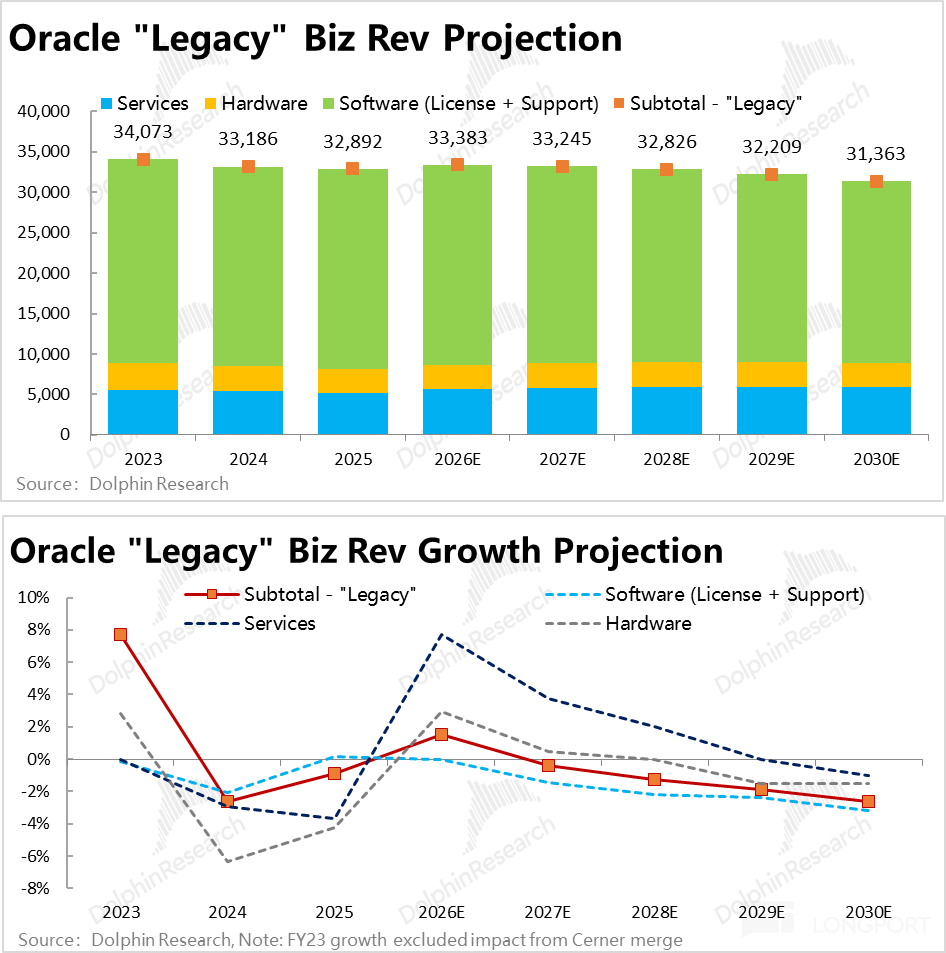

Traditional databases, software licensing, maintenance services, and enterprise backend management still have high customer stickiness, contributing stable high margins and cash flow. However, growth has clearly slowed down.

What changed Oracle's fate is the dual pressure from cloud computing and AI.

In the traditional cloud era, AWS, Azure, and Google Cloud continuously absorbed enterprise IT budgets. If Oracle only defended its databases and software, it could still make money, but its core products would increasingly run on others' infrastructure, with pricing power gradually flowing to hyperscalers.

Therefore, OCI is significant for Oracle. It is an attempt to protect database control, maintain enterprise customer relationships, and regain infrastructure pricing power.

Especially in the AI era, computing power, electricity, data centers, GPU clusters, and long-term contracts are becoming scarce resources. Oracle has finally found a path that doesn't require replicating Azure or AWS but can still tap into the core growth narrative.

This also explains Oracle's extremely divided state today.

On one side is the mature, low-growth, high-cash-flow traditional software base; on the other is the high-growth, high-CAPEX, high-debt, high-uncertainty OCI and AI compute leasing business.

OCI may contribute most of the future incremental revenue but also brings huge balance sheet risks.

The current controversy stems from this division. Bulls can see the explosion in AI compute demand. With major customer contracts, database stock, and multi-cloud partnerships, Oracle is poised to become a key player in AI infrastructure. Bears can see that AI compute leasing heavily relies on a few large customers, with massive upfront investments. Any deviation will put pressure on cash flow and the balance sheet.

Oracle wants to use the cash flow and balance sheet of its traditional software to exchange for a ticket to the AI compute infrastructure era.

The value of this ticket depends on several core questions: Is OCI's AI revenue real and sustainable? Can RPO smoothly convert into revenue and cash flow? Can the gross margin and ROIC of AI compute leasing cover the upfront investments? Can Oracle expand from a few major customer contracts into a scalable, profitable AI cloud platform?

ORCL: Big Bet on AI Compute — Are the Odds Good Enough?

Per Dolphin Research's prior note on Oracle, our core takeaway is that Oracle is essentially a scaled-up CoreWeave. The bull case hinges on explosive AI compute demand that could lift its compute-rental revenue by 10x or more.

The key risk is the mismatch between uncertain AI demand and fixed upfront capex and leverage, which could lead to sizable credit losses if the AI cycle unwinds. Overall, visibility is limited...

+6

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.