I will break down PLTR into two valuation frameworks.

The first framework: the traditional SaaS framework.

Within this framework, PLTR is ridiculously expensive. Over 45 times forward sales, more than 300 times P/E. Any slowdown in growth, decline in margins, changes in contract pace, or government budget disruptions will lead to severe compression. Under this framework, it cannot be called undervalued.

The second framework: AI workflow monopoly.

PLTR is one of the few platforms that can truly deploy AI into government, military-industrial, and enterprise operational systems, and its US commercial revenue continues to grow at over 100%. Its valuation should not be calculated based on SaaS, but rather as the enterprise OS entry point in the AI era. Under this framework, the current pullback is an opportunity for long-term bulls.

The key question is: which framework will the market ultimately use for pricing?

One thing is certain: PLTR is currently in a period of valuation framework contention. Its fundamentals support the second framework, but the market style is still temporarily rewarding visible AI CapEx recipients like hardware, power, storage, and data centers. So, PLTR is not without value; its value just hasn't been recognized yet. Its value realization will have to wait for the market to shift from "who sells the shovels" to "who turns AI into organizational productivity."

It's awkward in the short term, yes, because the stronger the earnings report, the harder it is to explain the valuation. It must continue to use high growth to digest its valuation, not just tell stories.

PLTR's earnings report continued its streak of beating expectations for 10 consecutive quarters, with strong growth in US customers and the launch of AI FDE on the product side, achieving a peak in revenue per employee in the US market. There's nothing to worry about fundamentally. I'd like to discuss the phenomenon I've observed from the perspective of institutional holdings and capital rotation:

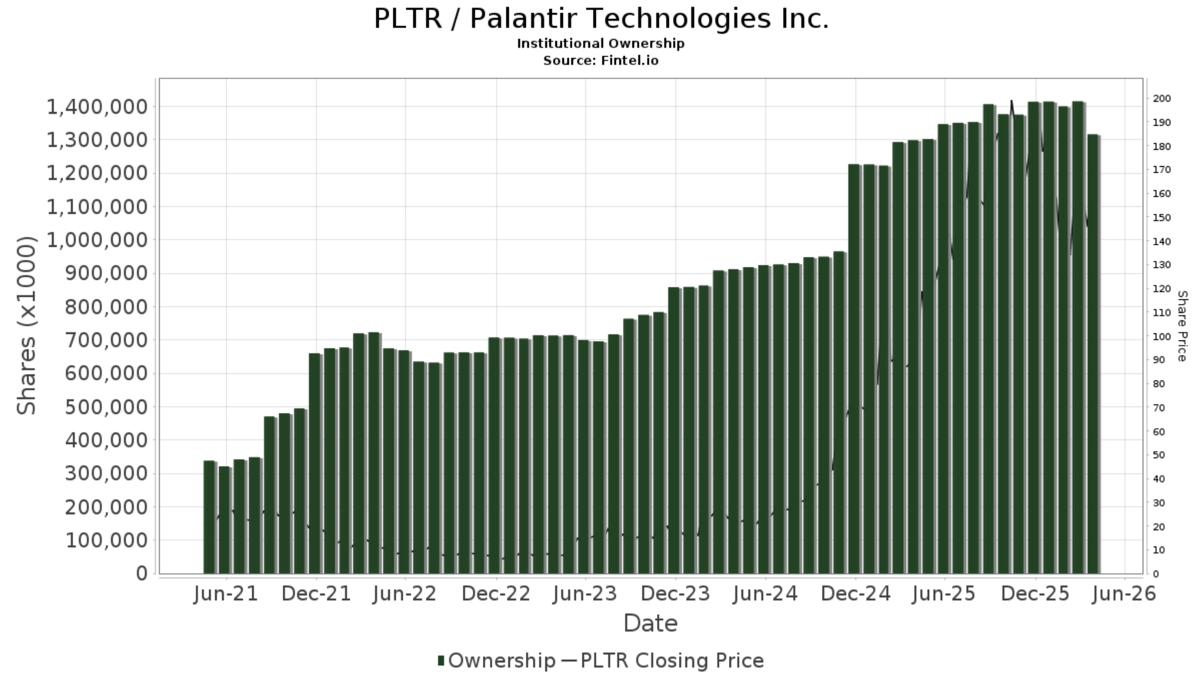

Starting from Q1, PLTR's institutional holding ratio stabilized after nearly five years of growth and saw a significant decline in Q2. This coincided with the suppression of software stock valuations since early '26 and the continuous surge in AI hardware like storage. The decline in PLTR's institutional holdings also represents active funds reducing their weight and allocation to the software sector. In terms of trading volume, last year TSLA, NVDA, and PLTR were regulars in the top 5 for trading volume. Now, the top trading volume spots have become Micron and SanDisk. If the market was still skeptical in Q1, then by Q2 institutions had already started to FOMO. At the same time, as the market capitalization of the storage hardware sector grew, it also increased the companies' weight in the Nasdaq 100 and S&P 500. During the next index rebalancing, this will bring more passive index-following capital inflows. Once this sector trend is established, it won't be easily reversed. Against this backdrop, even the best performance by individual software stocks is placed in a challenging context. This is the awkward current situation for software stocks.

However, PLTR is different from ordinary software stocks. PLTR has unique irreplaceability. Even with the current sector rotation, I have no doubt about PLTR's potential to surge towards a trillion-dollar market cap in the future. Karp once said in the 2024 shareholder letter: "All of the value in the market is going to go to chips and what we call the Ontology." Hardware still needs software to land in commercial scenarios to realize broader business value. In the wave of AI, I believe the two are spiraling upwards. This is the logic behind why I remain bullish on PLTR.

$Palantir Tech(PLTR.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.