$Destiny Tech100(DXYZ.US)$Tema Space Innovators ETF(NASA.US)Close the door🚪, release the dog🐶

我是来挣钱的

ReturnsTop 22%MidBlend

赚钱!

我是来挣钱的Suggestions for you to follow

我

$Porter & Company Porter Portfolio IdxETF(PCPP.US) First check-in 😁

Porter & Company Porter Portfolio IdxETF

USPCPP

我

$Tema Space Innovators ETF(NASA.US) Grateful for your company. May everything remain as beautiful as the first encounter.

Tema Space Innovators ETF

USNASA

我

$Roundhill Memory ETF(DRAM.US) After much hesitation, I've decided to exit. Thanks to the memory stocks for helping me out of my first predicament. Wait for me to come back! Maybe next week!

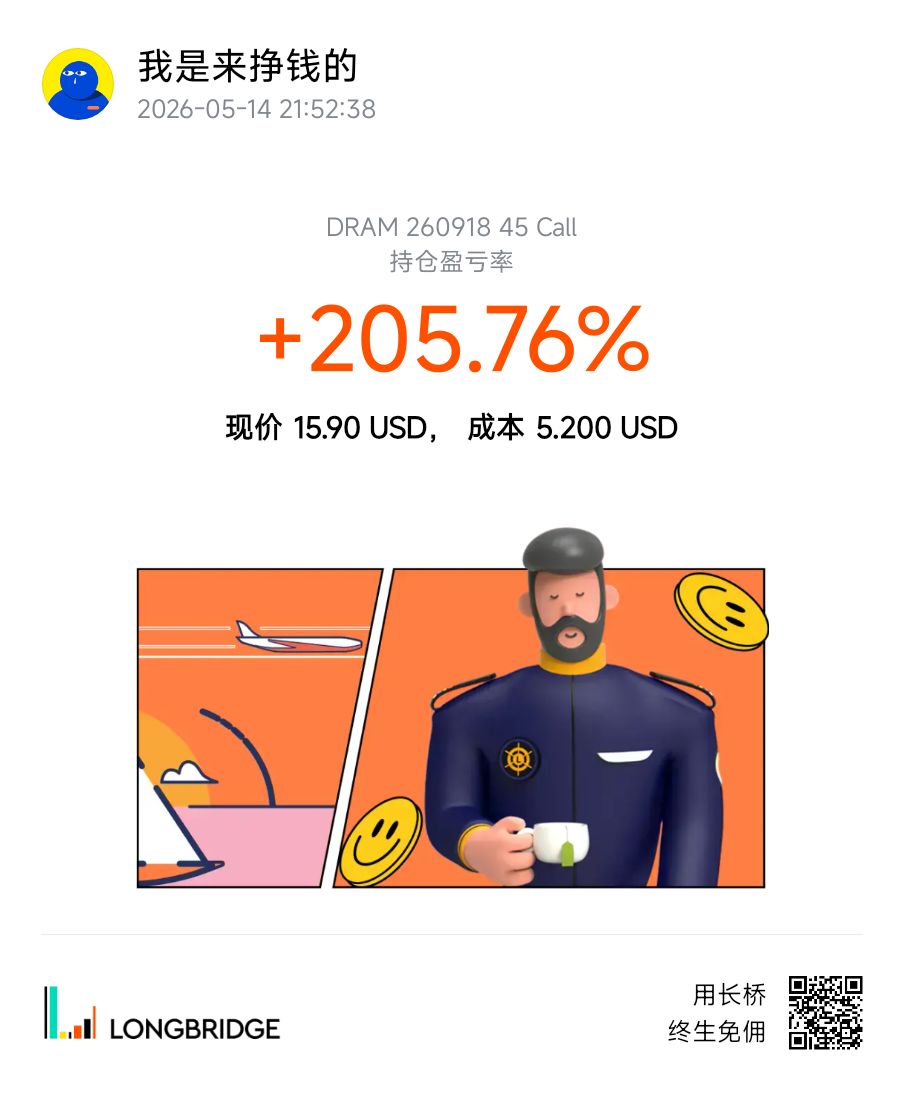

Roundhill Memory ETF

USDRAM

我

$Cerebras(CBRS.US) is indeed an impressive company. You can try out the chatbot on its official website; the token generation speed is mind-blowing: for the same question, deepseek flash streams the answer out word by word, while cerebras almost instantly completes the response. Here are two data points from Cerebras: 485 tokens took only 0.41s, and 1472 tokens took only 1.51s.

What does this mean? It means the company's wafer-scale approach can drastically reduce training and inference times. Large model companies can train models faster (reportedly cutting the time to one-fifth of the original), and users will spend less time waiting for results (or not wait at all).

If the company's solution becomes widely adopted, its market cap and stock price could reach for the stars. The problem lies right here: the competition is too strong (in my opinion). NVIDIA has locked down the upstream and downstream supply chain. NVIDIA's GPUs, Google's TPUs, and others occupy most of TSMC's production capacity. How to convince the supply chain to let core value flow through Cerebras and be captured by the company is a key angle to watch in the medium to long term.

Bullish in the short term, cautious in the medium to long term.

Cerebras

USCBRS

我

$SMIC(00981.HK) Wait for it to drop to 50-60 before bottom-fishing, it can't go any lower. After all, we can't let the state-owned leaders lose money, but we can't let them not make a single cent either.

SMIC

HK00981

我

$MetaLight Inc.(02605.HK)

1. METALIGHT is essentially an advertising company

The company relies on the "Che Lai Le" app as its advertising platform, achieving mobile advertising revenue of 202 million yuan in 2024, accounting for 98.02% of total revenue. The company's overall gross margin level is 76.38%, with advertising mainly sourced from companies such as Tencent, Douyin, Baidu, and Alibaba.

According to the prospectus, the company is the third-largest public transport information service provider in China. The top two are speculated to be Baidu Maps and AutoNavi Maps. The market shares of the top three are 20.4%, 12.4%, and 9.6%, respectively.

2. Financial Analysis

The company's revenue growth has fluctuated, with year-on-year revenue growth of -17.17%, 28.92%, and 18.11% in 2022, 2023, and 2024, respectively.

Due to the existence of preferred shares, there may be an impact on our understanding of the financial statements. The adjusted net profits from 2022 to 2024 were 9.0046 million yuan, 42.6606 million yuan, and 49.7476 million yuan (all converted to RMB), respectively. The company's adjusted net profit margin in 2024 was approximately 24%.

3. Valuation as an Advertising Company

In terms of comparable companies, some believe METALIGHT is a time-series data service or big data service company. Based on its 98.02% revenue share from advertising and considering that "Che Lai Le" is the company's advertising platform, I personally tend to classify it as an advertising company but will give it a slightly higher valuation than the industry average due to its data analysis capabilities.

Among A-share listed advertising companies, Focus Media and Lansheng Co., Ltd. have similar net profit margins, with an average PE of around 20x. In Hong Kong, China Vision Media Group has a PE of around 11x.

Based on this calculation, as of the end of 2024, the company's reasonable stock price per share is estimated to be between 3.87 HKD and 7.03 HKD, with a preference for the 6-7 HKD range. As we are now in June 2025, the price per share can be considered for a slight increase.

The above is only my calculation and is for reference only.

MetaLight Inc.

HK02605

我

$XI2CSOPNVDA(07388.HK) Guys, I'm out first. But I still have a question: why isn't it 2 times the gain of the underlying stock?

XI2CSOPNVDA

HK07388