$Paypal(PYPL.US)Fucking hell, finally broke even.

股神12345

AssetsTop 1%

股神12345Suggestions for you to follow

股

$XIAOMI-W(01810.HK)The comment section is very toxic. Don't be anxious, don't panic. None of you have lost as much as I have. Calm down, okay? Don't curse someone's ancestors just because you lost money.

XIAOMI-W

HK01810

股

$Hims & Hers Health(HIMS.US) A new day, full of anticipation

Hims & Hers Health

USHIMS

股

$Hims & Hers Health(HIMS.US) So much net inflow, what's the situation? @Ouyang

Hims & Hers Health

USHIMS

股

$Hims & Hers Health(HIMS.US) Damn... really starting the weekly deduction mode

Hims & Hers Health

USHIMS

股

$Hims & Hers Health(HIMS.US) Feels like it's going to rise after the earnings report. Hold it.

Hims & Hers Health

USHIMS

股

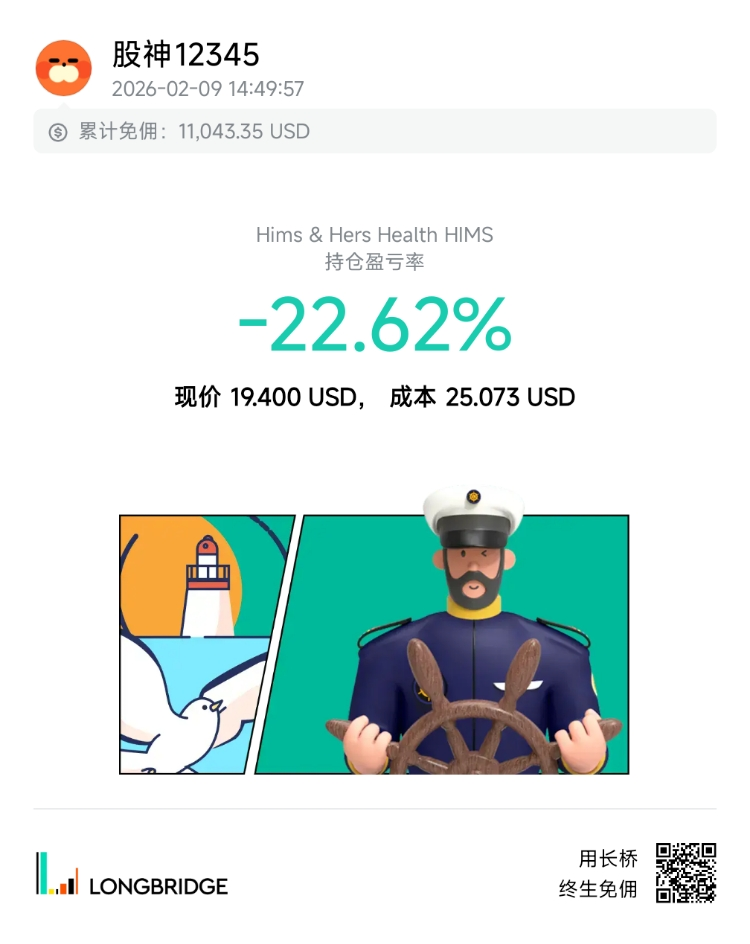

$Hims & Hers Health(HIMS.US) what's wrong with it, falling every day

Hims & Hers Health

USHIMS

股

$XIAOMI-W(01810.HK) It's very painful and agonizing. External forces are all shorting Xiaomi and shorting Hong Kong stocks.

XIAOMI-W

HK01810

股

This Dolphin Research rice black (biased) is damn, not neutral. Could it be on the same front as Yicai?

Xiaomi 4Q25 First Take: results broadly in line with our preview. All revenue growth this quarter came from autos, while legacy segments—smartphones and IoT—were under pressure.

This quarter’s prints point to mounting pressure. Smartphone GPM fell to single digits (8.3%), and IoT revenue declined double digits (-20% YoY). Auto GPM also contracted, with weekly orders trending down meaningfully.

With memory prices still rising, a turnaround in smartphones and IoT looks unlikely, and expectations are low. As for autos, after the YU7 cooled, weekly orders deteriorated, falling to around 4k by early Mar.

With legacy businesses soft, autos will need to carry earnings. The mid-cycle refresh of the new-gen SU7 delivered limited surprises, so investors will look to upcoming models and large-model initiatives for the next set of catalysts. For details, stay tuned for Dolphin Research’s follow-up takes and Trans. $XIAOMI-W(01810.HK) $Xiaomi Corporation(XIACY.US) $XIAOMI-WR(81810.HK)

股

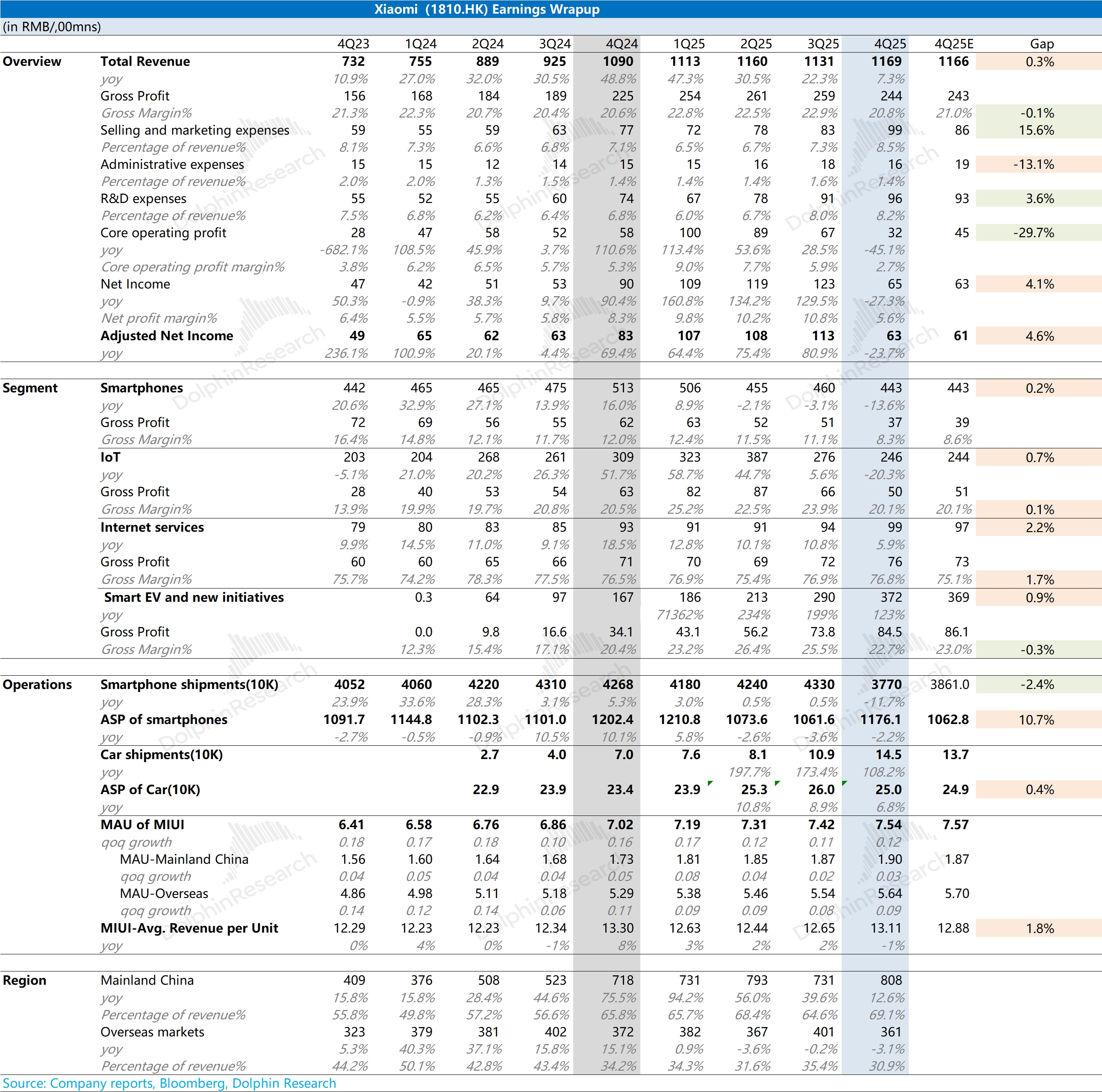

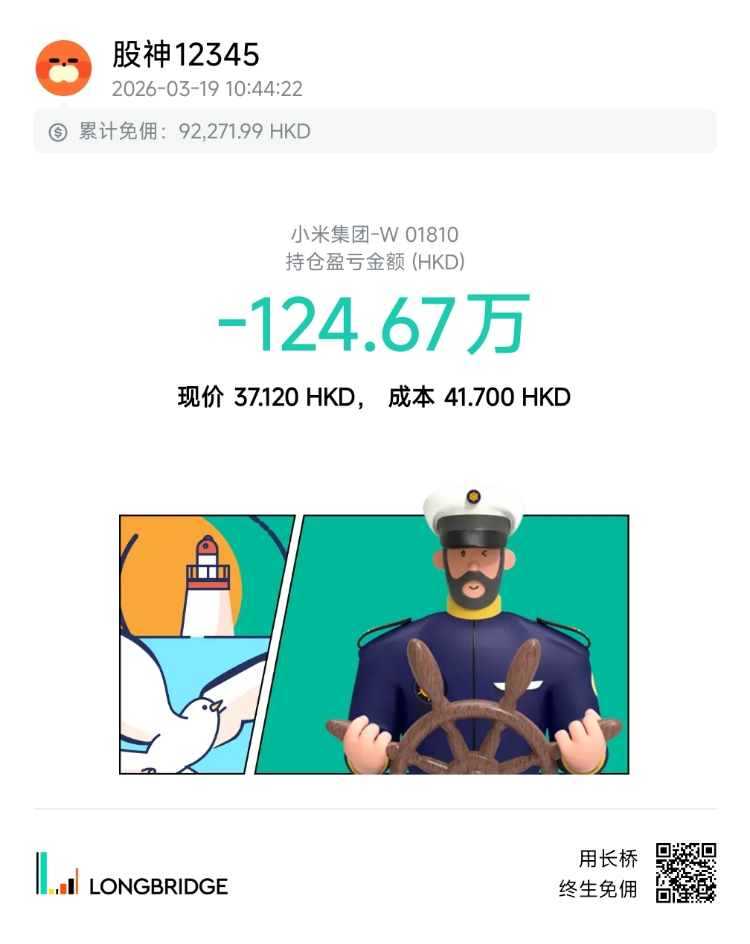

Loss of over 200 turned into over 100

Believe in the power of belief$XIAOMI-W(01810.HK)

股

Write to myself.

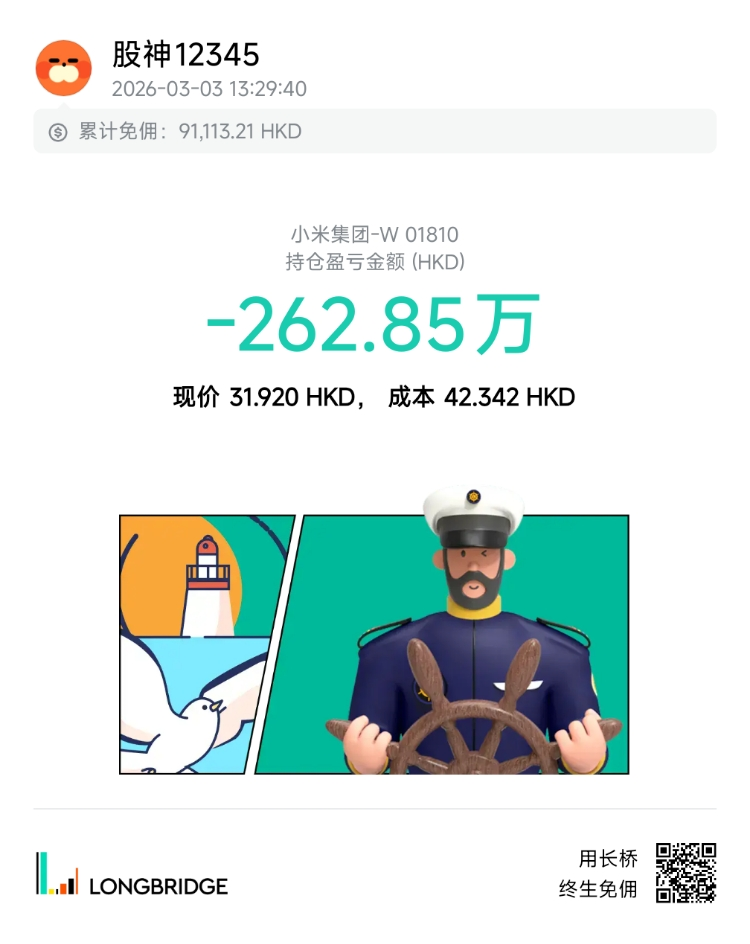

Remember this dark moment

Keep a good mindset

Stay healthy

There will always be opportunities $XIAOMI-W(01810.HK)

股

$XIAOMI-W(01810.HK)

First, the conclusion:

- Hong Kong stock market turnover is indeed low, but it's not 'rotten'; it's a liquidity issue caused by a combination of structure, environment, and mechanisms.

- According to January 2026 data:

- Hong Kong stocks rank 5th to 6th globally in exchange turnover (stock spot)

- Total market cap ranks 4th globally, IPO fundraising ranks 1st globally

I. First, a direct comparison (January 2026, RMB)

- US stocks (NYSE+NASDAQ): Daily average ≈ 7.4 trillion RMB (≈ 1.03 trillion USD)

- A-shares (Shanghai & Shenzhen): Daily average ≈ 3.3 trillion RMB

- Hong Kong stocks (Main Board): Daily average ≈ 240 billion RMB (≈ 272.3 billion HKD)

👉 Hong Kong stocks ≈ 7% of A-shares, 3% of US stocks, a huge gap

II. Core reasons for low Hong Kong stock turnover (not 'rotten', but structural)

1. Investor structure: Institutional dominance, very few retail investors

- Institutions account for ≈80%, low turnover, long-term bias; A-shares have many retail investors, high turnover

- Hong Kong stock turnover rate is only 1/5 of A-shares, naturally low volume

2. High transaction costs

- Stamp duty 0.13% on both sides (relatively high globally), less high-frequency trading

3. Severe liquidity stratification

- Top 10 stocks (Tencent, Alibaba, etc.) account for ≈60% of Main Board turnover

- Many small and mid-cap stocks have daily turnover < 100,000 HKD, even zero turnover

4. Offshore market nature

- Heavily influenced by Fed interest rates, USD liquidity, with large foreign capital inflow/outflow volatility

- Southbound capital is the main force, but net inflows are unstable

5. Traditional industry structure

- High weighting in finance, real estate, limited appeal of new economy sectors

III. Hong Kong stocks' real global ranking (January 2026)

1. Stock spot turnover (daily average, RMB)

1. US stocks (NYSE+NASDAQ): 7.4 trillion RMB

2. A-shares (SSE+SZSE): 3.3 trillion RMB

3. Tokyo Stock Exchange: ≈ 1.2 trillion RMB

4. London Stock Exchange: ≈ 0.8 trillion RMB

5. HKEX: ≈ 0.24 trillion RMB

👉 5th globally

2. Total market cap (end of January 2026)

- HKEX: 50.8 trillion HKD ≈ 44.7 trillion RMB

- Global ranking: 4th (after US stocks, A-shares, Pan-Europe)

3. IPO fundraising (2025)

- Hong Kong IPO fundraising ≈ 280 billion HKD, number one globally

IV. One-sentence summary

- Low turnover and poor liquidity in Hong Kong stocks are facts, but it's not a rotten market; it's the result of institutional dominance + offshore nature + costs + structure.

- It remains a top 5 global exchange, Asia's number one IPO market, and the main offshore listing venue for Chinese companies.

XIAOMI-W

HK01810

股

$Hims & Hers Health(HIMS.US)

Finally broke even. This kind of stock really shouldn't be touched.

Hims & Hers Health

USHIMS

股

Really, I can't say anything.

股

$Hims & Hers Health(HIMS.US) Buying this stock is worse than eating shit

Hims & Hers Health

USHIMS

股

Fully agree. The Hong Kong stock market is done for. Trading volume is very low, deposit and withdrawal requirements are high, and it ranks first globally in IPOs.

$XTALPI(02228.HK) capital pool "dries up": retail investors can't get in, institutions are unwilling to stay

The HK$500,000 threshold for Stock Connect directly blocks 95% of mainland retail investors, and the few remaining qualified investors only dare to test the waters with less than 5% of their positions, far from forming the "national 买单" effect seen in A-shares. Meanwhile, Hong Kong local capital has already flocked to U.S. stocks, turning Hong Kong stocks into a "forgotten market"—despite raising nearly HK$300 billion in IPOs in 2025 (ranking first globally), its average daily trading volume can't even match that of a single Tesla stock in the U.S. This "blood-sucking expansion + exhausted trading" leaves growth stocks like Jingtai Holdings with no capital support. More critically, foreign capital accounts for over 60% of Hong Kong stocks, making them prone to withdrawal at the slightest global disturbance, unlike A-shares with "national team" support—when they fall, there's no bottom.

股

$Adobe(ADBE.US)No, what is this.. Is it going to be delisted?

Adobe

USADBE

股

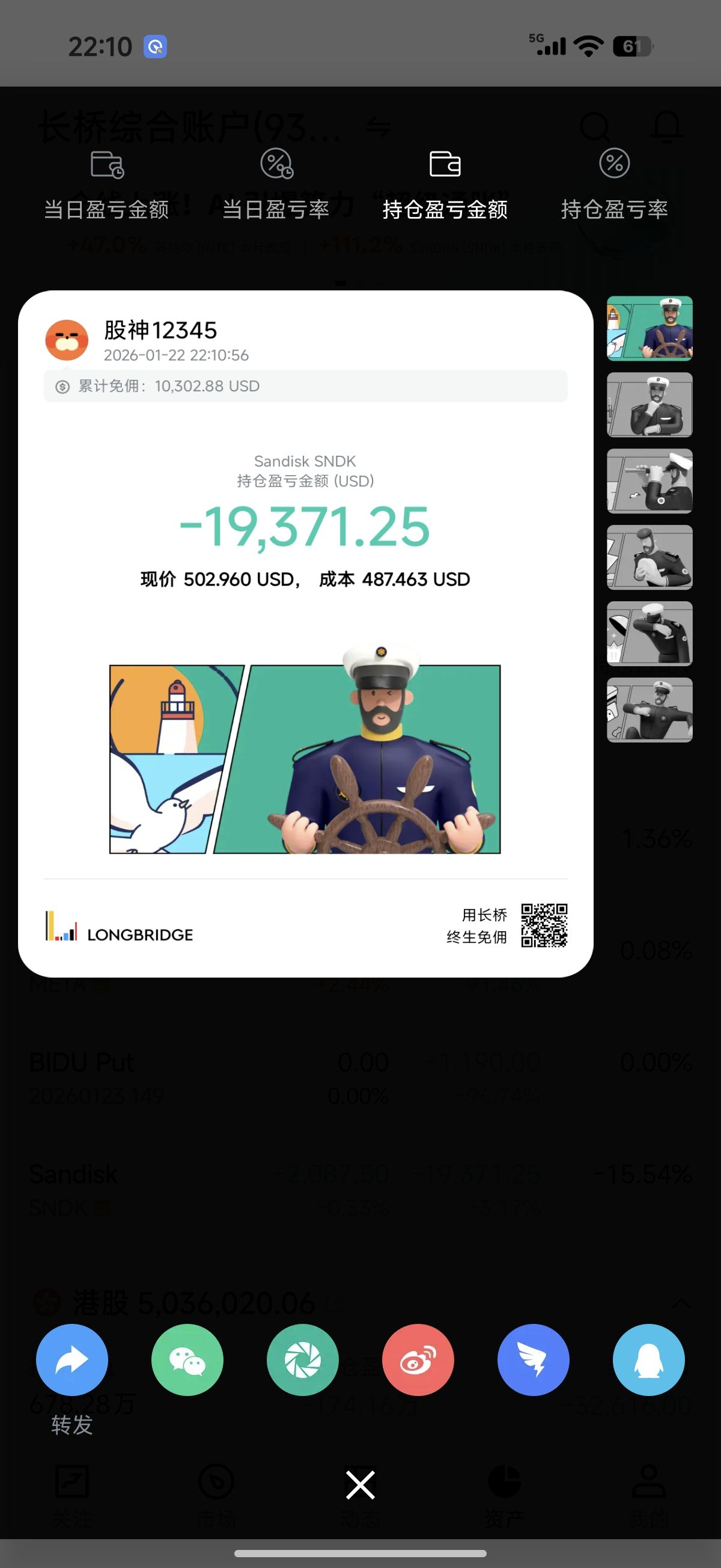

$Sandisk(SNDK.US)Thinking about how I closed my short position quickly the other day, otherwise I would have lost a lot. After the earnings reports of various storage companies are released this week, there should be a period of decline.

$Sandisk(SNDK.US)Yesterday, a short position of 600,000 USD directly lost 35,000 dollars during the day.

股

$XIAOMI-W(01810.HK)Damn it, 180,000 was deducted as soon as I opened my eyes

XIAOMI-W

HK01810

股

$Sandisk(SNDK.US) is too strong. Supported it

Sandisk

USSNDK

股

$Sandisk(SNDK.US)Yesterday, a short position of 600,000 USD directly lost 35,000 dollars during the day.

Sandisk

USSNDK