Be Barrons:

- Wants to write about optical supply supply chains like $Applied Optoelectronics(AAOI.US)- Hiring DPT: who needs engineers to write about this something this simple? Let’s find underpaid political philosophy backgrounds.- proceeds to find a new hire from nonprofit communication consulting- first day on job: gets paid to model revenue ramp/margins projections, CW laser bottlenecks, internal capacity- New hire: “I don’t understand this sht”, “looks like a memestock”Barrons: “Memestock? looks like our next article, I don’t understand either”.

Serenity

AI/Semi Supply Chain Analyst ex. RISC-V FDN, AI research scientist;

SerenitySuggestions for you to follow

S

Now that markets are hosting a laser party again from $SIVE, OE Solutions, $Lumentum(LITE.US), Coherent, to $Applied Optoelectronics(AAOI.US).

There’s a pretty interesting study:Both from Fidelity and a UC Berkeley research paper, that the best investors are the ones who either…- Anecdotally forgot about their account (Fidelity)- Didn’t actively trade/overtrade (18.5% return from infrequent traders vs. 11.4%).Not any advice, but some of these anecdotes might be helpful to retail to read in general…Since I witnessed a lot capitulation off memory, photonics, or thematic volatility, just for retail not have positions on a sharp recovery.Having conviction also usually people in that “not overtrading” camp, since it helps to not overtrade in drops or see opportunities to cost average.

S![图片 1,共 1 张]()

Just some near term events:

- OCP APAC tomorrow (Ayar, Lightmatter, $AMD(AMD.US), $NVIDIA(NVDA.US)) and your CPO players are giving announcements/updates.This should be a catalyst for certain optical players.- Earnings week: with $AST SpaceMobile(ASTS.US), $Rocket Lab(RKLB.US) reporting today (space), $Lumentum(LITE.US) on Tuesday (photonics), $Nebius(NBIS.US) in the middle of the week (Neocloud), and more.- Unitree IPO subscriptions opened up today and Listing is expected this month.Should be a potential catalyst for the humanoid + robotics sector if it opens up well eg. $Churchill Capital XI(CCXI.US).Fun week ahead.

S

Today I'm writing a weekend guide on how to do DD when shorting $Nebius(NBIS.US):

First, you look at hyperscaler earnings for AI cloud read through: > $Alphabet(GOOGL.US): reports record AI cloud demand + backlog + margin increases from earnings> $Amazon(AMZN.US): reports record AI Cloud demand + backlog + margin increases from earnings> $Meta Platforms(META.US): reports higher than expected prices for available capacity from earnings.Now, time to look at Nebius:-> $Nebius(NBIS.US): Growing hundreds of percent to $7-9B ARR by Q4. Growing margins, and guided 4GW+ contracted power. -> Sees Uber/Waymo splitting, putting more focus on Avride-> Sees Clickhouse growing rapidly every quarter. Okay looks bad! But next, you need a hedge?-> Wow! A $NIKE brand executive, after the stock dropped 75% over the past 5 years, went to $Lululemon(LULU.US) to save that brand next? Lululemon seems good.Conclusion: Short Nebius and go long on $Lululemon(LULU.US)

S

I've mapped the entire Wall Street bear playbook on AI names:

Have your favorite institution/media insert one of these name down below:1. < ______ [GPUs, Transcivers, MLCC, Memory...] are a commodity set to crash> 2. < ______ [YMTC, CXMT, Dongshan...] from China will flood the market > 3. < ______ [Micron, Nvidia, ...] from unverifiable channel checks is facing issues > 4. < ______ [Kospi, Sivers, ...] is a bubble like the ____ [2007, 2021] crash> 5. <____ [1,2,3, ...] unexpected rate hikes this year>6. < _____ [Google, Nvidia, Deepseek ...] optimization removes the need of this!> in a new headline, and it's ready to go!S![图片 1,共 2 张]()

![图片 2,共 2 张]()

There we go, White House finally invests in more breath in critical minerals/materials. Amazing policy move, as a TLDR:

- $Westwater Resources(WWR.US) receives $25M (graphite)- $Scully Royalty(SRL.US) (ASX) receives $400M (Scandium)- $5E Advanced Materials(FEAM.US) receives $8M (Boron)- $HREE receives $4.8M (magnet rare earths)out of the public companies. With more private investments from $150 million into Niron Magnetics or $85 million into Standard Bauxite. It's literally spare change to the US gov, for ENORMOUS amount of downstream applications. More should be done with funding amounts to accelerate development and derisk supply chains (don't own any of the above, just support the policy move), but great announcement.S![图片 1,共 3 张]()

![图片 2,共 3 张]()

![图片 3,共 3 张]()

I usually make fun of sellside, but Rosenblatt has pretty goated channel checks on optical names, and their reports are one of the few I like talking about.

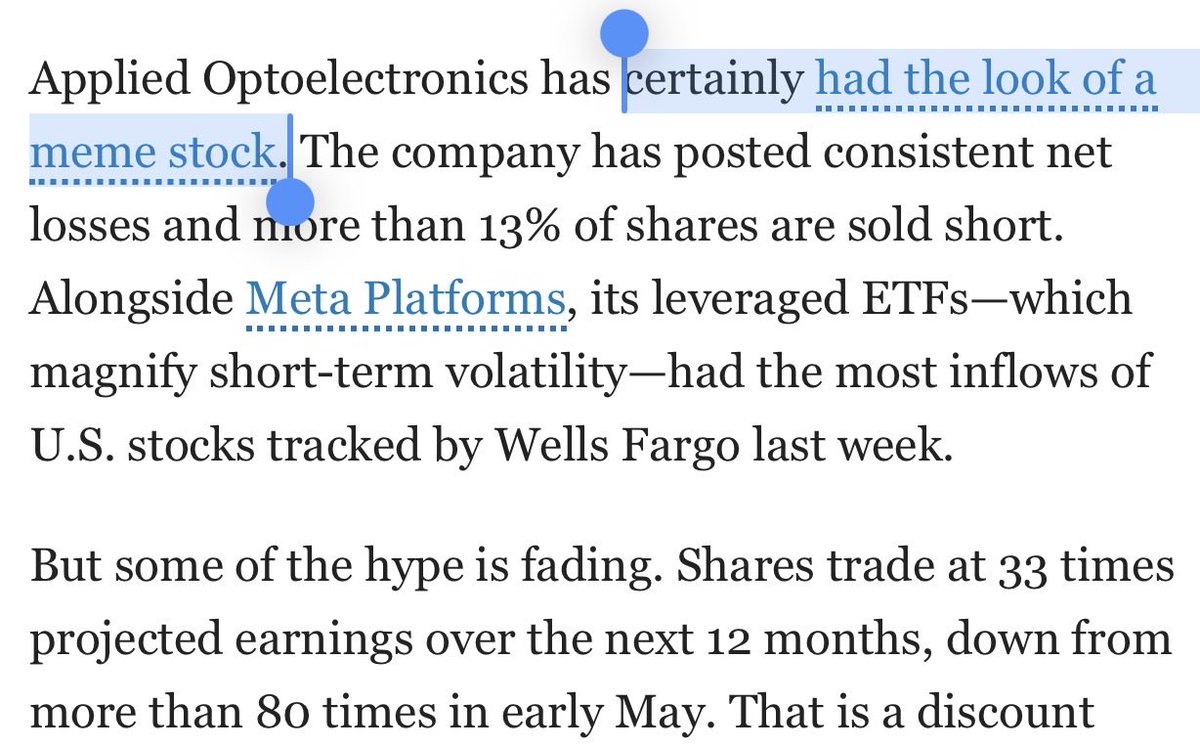

$Applied Optoelectronics(AAOI.US), $Lumentum(LITE.US), $SIVE, and the laser party has started to recover around the est. timing windows. eg. last month: "Multiple short sellers told them they will likely close their positions... late July and early August". They might have missed that they believed $AMD(AMD.US) would be $Applied Optoelectronics(AAOI.US)'s first CPO customer... since AAOI said they would be missing from first-gen CPO (maybe future gen?)But lot of their talking points about China CPO laser positioning (eg. 2-3 years behind) got corroborated word-for-word from AAOI earnings today.S

Unitree, China's humanoid leader, is set to IPO this month at a $9B valuation! (~$6.2B originally per March filing).

Derivative markets are pricing open at an implied $36.04B MC, roughly ~4X listing price. $Churchill Capital XI(CCXI.US) / Agility Robotics, the first US pure-play humanoid company, is also going public later in Q4, at a ~$2.5B pre-money valuation.It will be interesting to see how markets price in America vs. Chinese Humanoid leaders.S![图片 1,共 3 张]()

![图片 2,共 3 张]()

![图片 3,共 3 张]()

Earlier today, optical interconnect company Lumilens "emerges from stealth" at a $5.5B valuation, after raising $700m.

Just as a recap from $POET Tech(POET.US) / $SIVE Linkedin OSINT mapping I shared earlier, Lumilens was supplying a top 3 hyperscaler customer. So we got confirmation of that a month later, along with the material figure that Lumilens has a "multi-billion-dollar customer agreement". And just for reference, $POET Tech(POET.US) has existing contracts with Lumilens ($50m purchase order, up to $500m) + contracts with $SIVE (depending on product lines). I actually took tiny positions in POET again after reading this news, since it finally gives them visibility into extremely well funded hyperscaler suppliers (on top of Poet's really large balance sheet). But TLDR: > Lumilens around similar (or even higher) valuations as Lightmatter/Ayar, bigger than markets thought with hyperscaler customers. > nice read through upstream on $POET Tech(POET.US) (derisking) / $SIVE.> Great for optical valuations in general, seeing a company go to $5.5B in 2 years.

S![图片 1,共 1 张]()

$Macom Tech(MTSI.US) earnings transcript:

"Customers are coming to us with urgency due to the general supply shortage of indium phosphide DFB lasers"Emphasis on "Urgency", CW "DFB lasers", "coming to us".CW DFB names, such as like $SIVE and $Lumentum(LITE.US) should be happy to hear about this laser bottleneck getting validated.S![图片 1,共 2 张]()

![图片 2,共 2 张]()

Just some TLDR notes on $Applied Optoelectronics(AAOI.US) earnings:

- Expects full qualification of 1.6T products by their hyperscaler customer within next couple of weeks (helpful revenue ramp #2, timelines)- Continues to believe that AOI will have the largest AI DC transceiver production capacity in the US (reiterating ambitions during a time when their competitors might get banned)- Expects facilities toward InP capacity to come online in early 2027 (timeline FYI in terms of further ramp) - Total capacity is approaching 200,000/u per month, EOY 650,000/u per month of 800g/1.6t. EOY 2027, 930,000/u (this is the ramp i want to see)- "increase our manufacturing capacity for our external light source or ELSFP. That's for co-packaged optics or CPO". we anticipate ramping production later this year and into 2027, ultimately culminating in about 400,000 pieces per month in 2028(need some time to model this into revenue)- "As we have mentioned before, we've been manufacturing lasers internally for many years. This has allowed us to avoid some of the shortages that have affected others in the industry"(vertical integration bull case during CW/EML laser shortages) - We believe that in the future, CPO will continue to drive increased demand for high-power lasers(thesis validation on CPO sector)- "to our long-term objective of returning non-GAAP gross margins to around 40%"- "We ended the second quarter with $508.8 million in total cash equivalents"I need to double check if the ATM finished or not- "our ability to deliver revenue in general, and specifically when it comes to 800G products, is limited by our production capacity right now" "If we could produce more, we could ship more right now"Demand > Supply validation. - "Most of the increased capacity will be in U.S. Even so, let me say that, like I keep emphasizing, that is not good enough for the customer demand. The customer demand is 20%-40% higher."Unholy photonics demand validation across the whole sector, read through for $Lumentum(LITE.US), $SIVE / $Jabil(JBL.US), and others is amazing. - "Not in the next two, three years, especially the demand is so big. Okay? Even combined AI, $Lumentum(LITE.US), $Coherent Corp.(COHR.US), $Broadcom(AVGO.US) all together, it's still very tough to meet the customer demand in the next few years"More optical sector demand validation. - CPO Timelines: "If you're talking about really high volume manufacturer [for CPO market], I would say more like the late Q3 next year" and "We have been working very close with at least five customer"If you care about current earnings (which I'm not really looking at closely)Revenue: $191M vs. $190m EPS: $.06 vs. $.02TLDR: Extraordinary demand across the laser + optical sector read through. Kinda supporting Lumentum CEO statement that laser shortage is worse than memory shortages. 2027 capacity ramp on track. To map inflection period with timelines, would be around early next year, as stated in their previous earnings call. AAOI has the customers now. Limitation is making enough lasers and transceivers.S![图片 1,共 2 张]()

![图片 2,共 2 张]()

Funniest callout of the year from $Viavi Solutions(VIAV.US) on CPO timelines:

"Well, there's been a lot of industry talk [about delays], like, 'Oh, because the yield is going to be slower.' That's all nonsense. CPO and all that thing is moving forward"They stated that Yes there's always issues, but the process is being improved and things are getting better. To follow up on that, the CEO stated: - Viavi has POs for CPO-testing activity- “We’re already getting [CPO revenue] this quarter, and probably in December it will start accelerating.”On a side note, they also stated, 1.6T is "ramping very quickly", should reach parity with 800g next year, and signaled longer tail for 800g demand. TLDR: Seeing CPO test revenues hit for $Viavi Solutions(VIAV.US) to $Formfactor(FORM.US) around now. Nvidia also stated switch-side CPO for scale out and scale across has entered mass production earlier. As for scale up timelines, early production should be H2 2027 for some players, with other CPO players Ayar stating 2028 is the volume inflection period. Basically, all the timelines seem to be the same as before and revenue is starting to hit testing players first.

S![图片 1,共 1 张]()

$Lumentum(LITE.US) CEO Michael Hurlston at the RAISE Summit warned that the supply gap for InP lasers for AI DCs:

Is facing a more severe supply chain crisis than memory. And with Lumentum's 5 InP fabs, shipments would be more than 30%+ below customer demand.This is especially visible with EMLs today but is already expanding to CW, especially as CPO ramps.I've always been a fan of the laser chokepoint + bottleneck from $Applied Optoelectronics(AAOI.US), $SIVE, $Lumentum(LITE.US), and $Coherent Corp.(COHR.US). And glad this thesis is starting to see validation.S

The media framing and X reactions around Leopold are egregious.

Framing his successful multi-year thesis from $Sandisk(SNDK.US) to $Bloom Energy(BE.US) as a "collapse" or "failure".After July's surprising crash, then personally attacking him on top is just pathetic to witness. It's almost like everyone is cheering for the downfall of others. Yes, July's crash exposed problems with SA’s leverage, liquidity management, and hedging. But his current YTD performance remains +80%, ranking among the best performing hedge funds. And he still has public equities after all this (just removed leverage). I think he's doing something unique while being successful at it. And this draws the envy of others.

S![图片 1,共 1 张]()

$Reddit(RDDT.US) ER in a nutshell:

Revenue: $804.9M vs. $730.4M (expected).EPS: $1.25 vs. ~$0.95.Net income: $252.8M vs. $196.5MQ3 guidance:Revenue: $860–870M vs. 829.1MAdjusted EBITDA: $385-395M vs. $369MBlowout financials, market always like to explain the drop 22.6% off some new BS narrative. Last quarter: "AI will disrupt Reddit causing revenue loss!"This quarter: "See, DAU fell .6%!" (proceeds to ignore any revenue/profitability growth)

S

Few earnings TLDRs with my favorite $AXT(AXTI.US) and $Amazon(AMZN.US):

Amazon:- Raised 2026 capex to $220B vs. prior $200B (partly due to higher memory costs, which is bullish on $Micron Tech(MU.US) to Samsung) - Even at $220B, Amazon will not have enough capacity to meet all 2026 demand; Jassy expects the same in 2027.- Most incoming 2027 capacity is already reserved, with substantial 2028 capacity also reserved.Mostly read through on upstream semis. $Alphabet(GOOGL.US), $Meta Platforms(META.US), $Amazon(AMZN.US), and $Microsoft(MSFT.US) all identified compute shortage. All the narratives a few weeks earlier was "excess compute" from Meta and others + hyperscalers cutting back on spend... All BS. Amazon earnings was very bullish on AI semi trade. AXTI:- AXT to double InP capacity during 2026. Then double again in 2027. This is expected to make AXT "by far the largest indium phosphide producer in the world." - LFG- Q2 rev was $47.6M, the highest quarterly revenue in AXT history (InP revenue reached a record $30.7M, from DC applications.)- Revenue increased 77% sequentially and 164% year over year.- InP revenue-capacity targets: $60M per quarter exiting 2026.- $130M per quarter exiting 2027 That $130m target could be hiked too since management stated they find "whatever ways to increase that capacity expansion"- Management said the reported backlog remains well above $100M, but that number no longer reflects all available demand."Customer demand continues to outpace supply, no matter how fast we add capacity." 800G/1.6T is driving the current cycle, while NPO/CPO extends it beyond 2027. Also they're targeting 50%-plus gross margin: "We should definitely be targeting a number that begins with a five."China demand more than doubled, and their agreements with Casela, $Coherent Corp.(COHR.US) and $Lumentum(LITE.US) did not materially drive Q2. This is not even considering my projected massive ASP hikes yet as InP substrates get more bottlenecked. TLDR:- Amazon too much compute demands, needs capex to fufill it, so upstream semis go brrr. - AXT world largest InP substrate supplier, high gross margins, expansion, and supply can't keep up with demand. Bullish on demand side from Amazon + capex. Bullish on upstream optical supply chains from too much demand.

S![图片 1,共 1 张]()

Did Citadel really just liquidate Situational Awareness…

Then brought up entire markets the next day?$Nebius(NBIS.US) +26.25%$IREN(IREN.US) +25.96%$SharonAI(SHAZ.US) +22.82%$Sandisk(SNDK.US) + 23.98%$Bloom Energy(BE.US) +23.67%$SK Hynix(SKHY.US) +16.98%$Intel(INTC.US) +12.16%Amid many others. This has gotta be one of the wildest liquidations I’ve seen.S

There's a lot of stupid commentary around Leopold raising funds. After names like $Bloom Energy(BE.US), $Sandisk(SNDK.US), $SharonAI(SHAZ.US), and others all had very sharp drawdowns in July.

Just remember... here's a man in finance that's1. 6'52. Blue Eyes3. Hedge FundProbably better looking than you, and was up 439% through June YTD. Regarding the drawdown, Aschenbrenner acknowledged that the fund had "not been immune" to the market turmoil, particularly in Asia. FT separately reported that leverage amplified both its extraordinary gains and recent losses.He described the sell-off as potentially the best buying opportunity since early 2025I'd agree with him and hope he succeeds with the raise.Since a lot of the current selloff looks like it overshot its mark through forced deleveraging.S![图片 1,共 3 张]()

![图片 2,共 3 张]()

![图片 3,共 3 张]()

US Gov to take 1% stake in $GlobalFoundries(GFS.US), and award them $300m for the US CHIPS ACT.

This is actually a strong read through on $SIVE / $Lumentum(LITE.US), given this CHIPS ACT is specifically aimed at advancing CPO + Silicon Photonics. (For reference, Sivers and Lumentum were the only two public laser suppliers named in GFS presentation slides. Sivers laser arrays was named recently as a reference design in Globalfoundries SCALE for CPO). Per US Gov announcement: "GlobalFoundries will receive up to $300 million to accelerate domestic CPO R&D by two to three years" (NIST)Never thought we'd see the US Gov / $Intel(INTC.US) foundry playbook for CPO in specific...

S

Just some TLDR news:

- $CXMT IPO tomorrow if you like Chinese memory. - Samsung Electronics reportedly struggling to secure large FC-BGA substrates. Ibiden (4062) reportedly requested LTA guarantees, Samsung Electro-Mechanics sought prepayments. - Samsung + $Broadcom(AVGO.US) sign memory + foundry AI framework through 2030, expected to exceed $200b- $SOI expects FY2027 silicon photonics revenue to double compared to the previous year, surpassing Morgan Stanley's 60% growth projection. Photonics thesis go brrr. - SK Group + $NVIDIA(NVDA.US) sign $500B+ partnership to build out AI DCs and HBM4 memory. - SKC Absolics glass core delay to 2027 from reports. Targeting final reliability testing EOY, mass production next year. So if you're curious, this does push back some ramps from $LPK and others (hence drop on ER). - $Qualcomm(QCOM.US) price hikes by double digits for smartphone processors, due to upstream supplier hike pricing.- $Meta Platforms(META.US) expected to issue $12B in project-level/SPV financing for El Paso, Texas AI DC expansion - Naver announced a $10 billion investment from $NVIDIA(NVDA.US) and Brookfield to construct a 1GW-scale AI Factory. Near term plan is 200MW by 2028. (Nvidia $1B investment, Brookfield nonbinding $9B)- 64GB DDR5 server modules rises 146% versus end-June contract pricing- $Intel(INTC.US) brought forward 14A process mass production by a year, risk production H2 2027 and volume production in 2028, vs. 2029 HVM expectations. - Samsung Electro-Mechanics wins $200m MLCC order (existing bottleneck). - $AMD(AMD.US) (the Bandana bottleneck), announces Helios is in full production with shipments Q3 2026. Including an up to 2GW MI455X GPU deployment with Anthropic and a 6GW infrastructure rollout with OpenAI. Gave new >50% CAGR TAM to $220B by 2030 from $26b in 2025 for CPU market. Rolls out optical interconnects for Mi500 in 2027. From channel checks, AMD is heading down to the CPO route (seems likely to use Ayar). - $Oracle(ORCL.US) wins $7B Department of War enterprise software contract- JX metal doubles semi target capacity at its KR subsidary with a 4B yen investment, with operations to begin H2 2027, amid surging demand from major customers Samsung Electronics and SK Hynix- Tungsten hexafluoride spot prices surged 2.1-2.5x Y/Y following Japan's Kanto Denka and Chuo Gas announcing permanent production halts. Fluorinated liquid supply faces a vacuum as 3M plans to exit PFAS production. - From the four optical chipmaker earnings, Yuanjie/Eoptolink/TFC Optical/Dongshan Precision: no major order cuts, 1.6T shipments expected to accelerate into 2027. Optical chip suppliers expected to capture outsized margins from shortages. - Unitree Robotics Targets 30,000 Humanoid Robot Production Capacity by 2026. Read through on humanoid TAM scaling like $Churchill Capital XI(CCXI.US) and others. - Energy storage lithium batteries orders increase first half orders by 2,900% apparently in China. Not as familiar with EVE Energy and other battery makers.

S

From $AMD(AMD.US) Advancing AI, channel checks:

Helios networking partners told me they expect AMD to pursue CPO for future generations of Helios scale up networking. And expects other hyperscalers + industry to go down the CPO route.One AI infra executive at a company involved in a hyperscaler CPO programs said they had seen no indication of CPO scale up supply chain delays.Pushing back on recent 3rd party delay reports.This was informal commentary, not official AMD or partner guidance.S![图片 1,共 1 张]()

$Intel(INTC.US) and $AMD(AMD.US) to sign CPU LTAs with Chinese customers for AI DCs (Reuters).

- Prices of some CPU products have risen more than 40% in China since the start of the year from sources. - Month-on-month increases topping 10% for some productsCPUs were already a bottleneck, following CPU ratios due to AI inference... But the broader trend of LTAs seems to be appearing from: - Memory, with $Micron Tech(MU.US), Samsung, $Sandisk(SNDK.US), and SK Hynix signing DRAM/NAND LTAs.- Photonics, with $Lumentum(LITE.US), $Coherent Corp.(COHR.US) signing EML LTAs. And recent Trendforce reports that $AMD(AMD.US) and hyperscalers are now pursuing CW LTAs. And I'm sure there's many more from MLCCs to all the way to substrates. +1 for the bottleneck investors... hard to be a "bubble that pops" if you have take or pay demand spanning multiple years.S![图片 1,共 4 张]()

![图片 2,共 4 张]()

![图片 3,共 4 张]() +1

+1

Just some notes from $Tesla(TSLA.US) transcripts:

Elon Musk: "I think Optimus will be the biggest product ever" from Q2 earnings transcripts.Even from Q1, Elon Stated: "I think Optimus will be our biggest product. Not just Tesla's biggest product ever, but probably the biggest product ever.And I remain convinced of that conclusion". It's very rare to see such high conviction reiterated from Elon regarding humanoids both directionally and TAM-wise.In terms of upstream suppliers opportunities, Karn Budhiraj, VP of $Tesla(TSLA.US) supply chains stated: "We’re seeing the same level of investment going to memory and also new specific items like metal injection molded parts, flexible printed circuits, and all sorts of nonlinear technologies..." And that they had to build new supply chains from scratch. So would be interesting to look at for new supply chain supplier opportunities apart from the known ones. Just pulled older slides and it looks like capacity targets for Fremont are 1M and Giga Texas was 10M, so at scale, $Tesla(TSLA.US) seems to be the clear US leader. If you're looking at that S-Curve opportunity ramp. On a side note, Elon also gave a shoutout to $Micron Tech(MU.US) with likely reasonably priced LTAs, given his statement: "We really appreciate Micron making room for Tesla in the years to come and giving us actually a very significant allocation on reasonable terms given the pretty insane pricing of memory these days." (Just for structural memory demand). Elon also gave a shoutout to Panasonic which had invested many billions in increasing battery cell production (will need to do deeper DD into Panasonic after this), then Samsung and $Taiwan Semiconductor(TSM.US). Just takeaways from Tesla earnings TLDR: Elon tends to be directionally correct on where the future is heading, such as with EV or Space. He seems extremely bullish on humanoids.

S![图片 1,共 1 张]()

$SIVE CEO buys 70K shares today.

I don’t really comment much on insider buying/selling, since it’s not exactly a fundamental catalyst.But given the company’s future is dependent on the CEO’s vision + execution, from NASDAQ listing, M&A, to scaling:It’s extremely positive to have Vickram be completely aligned with the shareholders