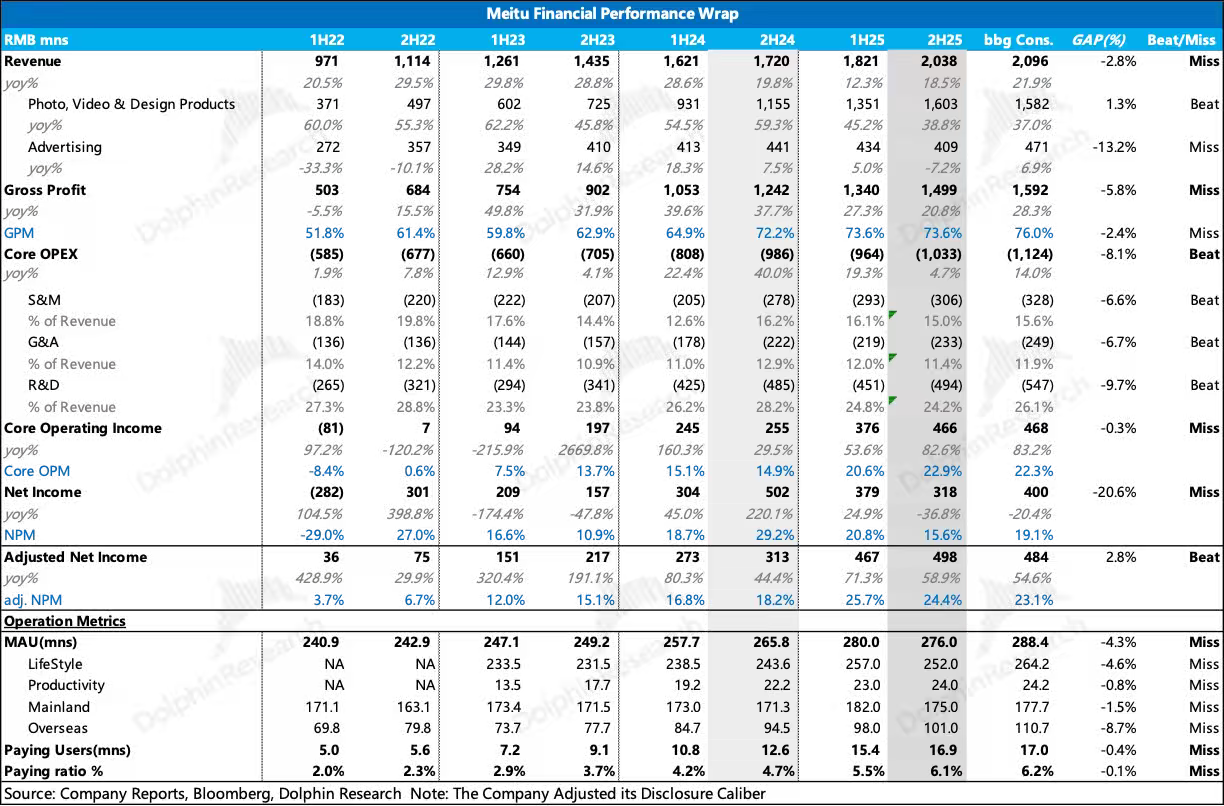

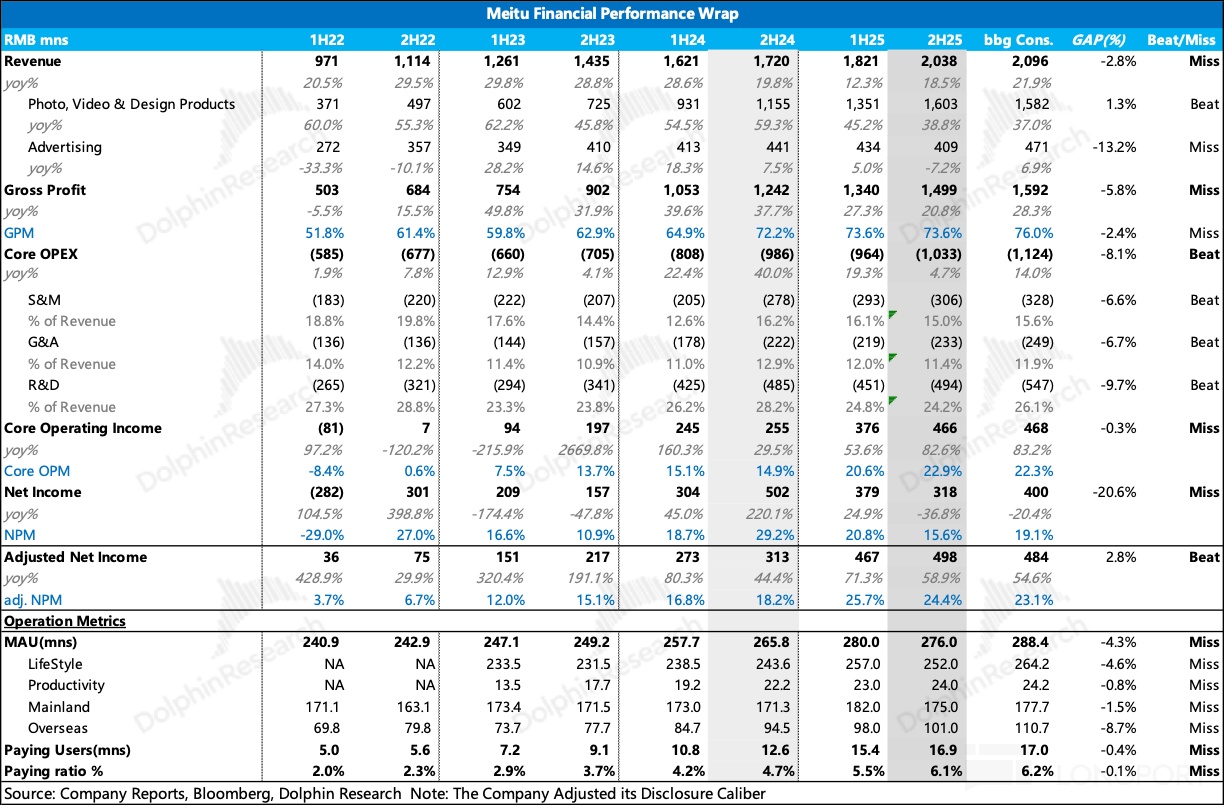

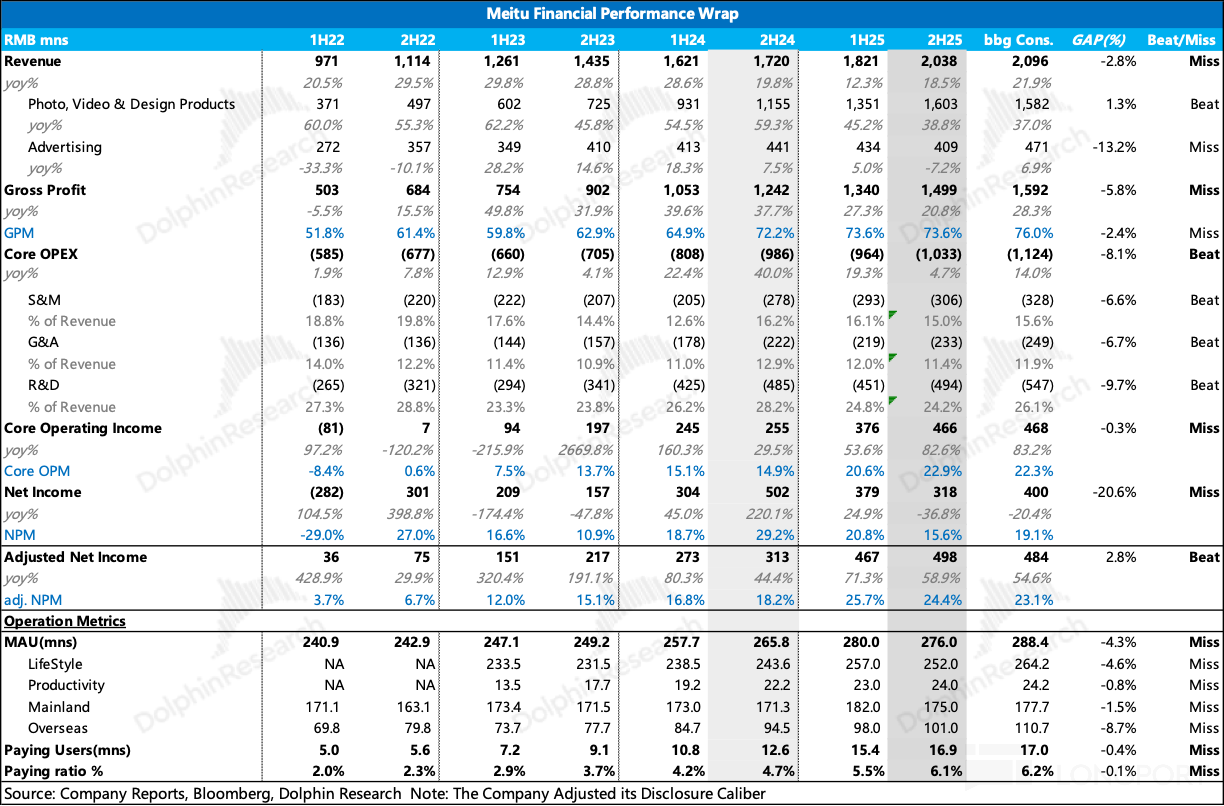

Meitu 2H25 First Take: Overall results came in below expectations, and an accidental early leak of the report may trigger a sharp market reaction. Revenue missed, GP missed materially, but disciplined opex delivery beat, leaving OP roughly in line. The user ecosystem underpinning subscriptions is under clear pressure, so Dolphin Research’s overall take is negative.

1) Overall MAUs fell by 4 mn vs. 1H. YoY growth slowed to 3.83%, missing Bloomberg consensus of 4.3%.

By use case, consumer-life scenarios lost 5 mn users vs. 1H. Dolphin Research attributes this to both measurement effects and a lack of year-end breakout features to drive acquisition.AI foundation models may also have siphoned off some C-end users. The productivity scenario was broadly in line.

Ex-China, YoY growth dropped sharply to 6.9% from 15.7% in 1H, missing the 8.7% consensus. The overseas MAU shortfall likely caps overall ARPPU and subscription penetration upside. On conversion, both subscriber count and penetration saw small misses and were basically in line.

In terms of growth volume, net new subscribers rose by 2.8 mn in 1H but slowed to just 1.5 mn in 2H. With total MAUs declining, the in-line penetration rate is partly a passive uplift from a smaller denominator, implying lower-quality conversion.

2) Core subscription revenue grew 38.8% YoY, still a strong pace. It reached RMB 1.603 bn, 1.3% above expectations.

3) Cost discipline

GP growth slowed to 20.8% YoY, with GPM flat vs. 1H. The GP miss mainly reflects two factors: a lower mix of high-margin advertising and the strategy of bundling compute costs into subscription plans to attract users, which drove a sharp increase in compute and API-related expenses.

Despite the GP miss, core OP was RMB 466 mn (+82.6% YoY), basically in line. The key driver was tight control across selling, G&A and R&D, delivering an across-the-board beat.

- On selling expenses, Dolphin Research had assumed intl expansion would require higher spend. In 2H, sales expense as a % of subscription revenue stayed at 16%.

- On R&D, the Model Container strategy curtailed base-model training spend. Full-year R&D grew just 3.8%.

Dolphin Research believes that, given the weak user ecosystem and especially the miss in overseas expansion, the company may still need to step up promotion to acquire users. Also note that R&D savings are coming at the expense of GP.For more, including management’s view on AI cannibalizing software and the outlook for B-end and overseas businesses, see the earnings call. Dolphin Research will share further views on Meitu; stay tuned.$MEITU(01357.HK)