BYD makes cars and buses but sure, "military company" ok 🙃 the label inflation is getting comical

BOYD Gaming

BYD----

Share your thoughts

Write something you'd like to share with our community...

- L

The "blacklist" of Chinese firms is not something new. Back in Feb 2026, the updated listed, which included Alibaba, BYD, Baidu, etc, was withdrawn shortly after it was posted for an hour on 13 Feb. It was thought that the withdrawal was to avoid antagonizing the Chinese following a trade truce reached by Trump-Xi. This, like the ding-dong of thr Nvidia export to China approval, are tools in the US war chest against Beijing. Having come after the Chinese crackdown on illegal cross border operation by Brokers in HK, restricting Chinese retail Investment in the US market, would anyone think this is a gesture to return the "kindness"?

☕️ [Task Coins Giveaway] Daily Market Talk — Tesla Robotaxi Goes Live

Tesla's Austin robotaxi launches without safety drivers, Intel jumps 11% on Google order, Marvell selected for S&P 500, US blacklists Alibaba and Tencent.

- M

Pentagon put Alibaba, BYD and Baidu on the military companies list and HK tech just folded -1.2%. here we go again with the China discount 😮💨

- H

Why the Upcoming Space IPO Could Matter for Markets

The upcoming space IPO could be a major signal that investors are ready to treat space as a serious public-market theme, not just a futuristic idea.

A strong debut may attract capital into satellite networks, launch systems, aerospace suppliers, defense-space, and space-based data services. It could also revive confidence in large frontier-tech listings.

The key risk is valuation: if excitement runs ahead of fundamentals, early enthusiasm may quickly turn into sharp post-listing volatility.

Community Spotlight | NVIDIA's Q1 Print, Cerebras Day One, and Singapore on the Sovereign-AI Map

This week's community feed clustered around NVIDIA's earnings print, the Cerebras IPO landing into a NVDA-dominated AI chip market, and a clear China-EV conviction call on BYD. 📊

- F

Featured

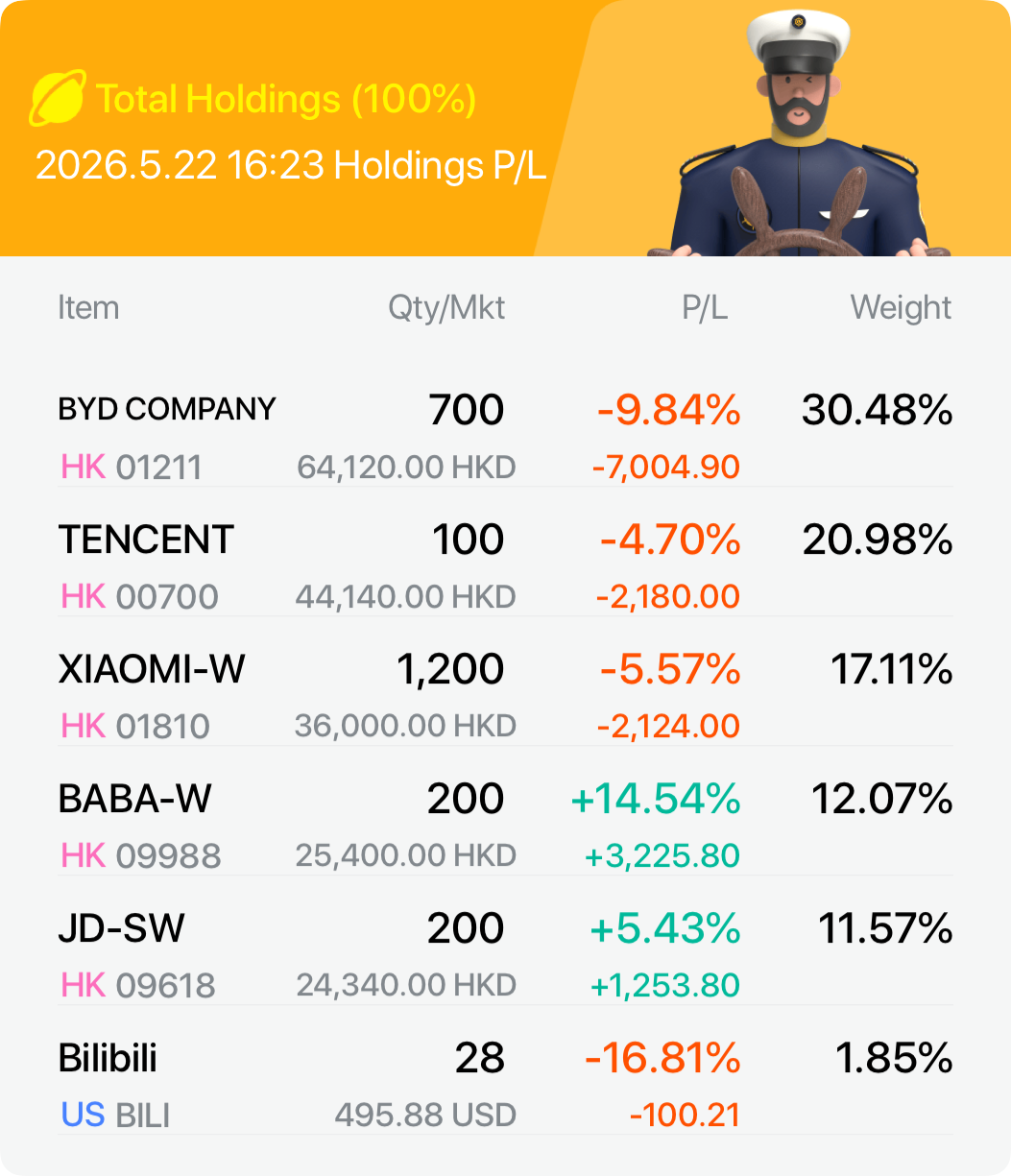

Featured[Week 5] Portfolio Health Check: Riding the Volatility Wave 🌊

1️⃣ Current Holdings

I continued to adjust my weightings and leaning further into my high-conviction plays. My sector distributions are:

🟢 Automobiles: 30.48% (BYD)

🟢 Interactive Media & Services: 22.82% (Tencent & Bilibili)

🟢 Broadline Retail: 23.64% (Alibaba & JD)

🟢 Tech Hardware & Peripherals: 17.11% (Xiaomi)

BYD is my largest single position at over 30% now. This reflect my increased commitment to the EV leader despite recent market swings.

2️⃣ Earnings Watch

The heavy lifting of earnings season is almost done! Xiao Mi will be the last one for me to watch.

This is the big one left, 26 May 2026. I am eager to see how the market reacts to their latest smartphone shipments and EV progress. Bilibili just reported and I am disappointed with the share price reaction😣.

3️⃣ Portfolio Reaction

It has been a tough week as the sea of red returns. Most of my holdings are facing a pullback:

• Alibaba (+14.54%) and JD.com (+5.43%) remain in the green.

• Bilibili (-17.04%) and BYD (-9.84%) took the hardest hits this week.

• Tencent (-4.70%) and Xiaomi (-5.57%) are also under pressure.

Overall, the portfolio is being tested by market-wide volatility but my core “Retail” anchors are keeping the ship afloat.😁

4️⃣ Next Plan

Patience is key. I added BYD and Bilibili this week, “averaging down” on positions. I strongly believe in for the long haul.

My next move is to hold steady through the Xiaomi earnings. I am pausing any further buying for now to maintain a healthy cash buffer in case the market dip deepens.🤣

5️⃣ Risk Check

Concentration in BYD has crept back up to 30.48%, which I need to monitor closely.

My top two holdings (BYD & Tencent) now make up 51.46% of the portfolio. I admitted that I am better diversified than in Week 3, the heavy HK/China tech exposure remains my primary risk.

Staying disciplined and looking past the short-term noise! 😌

My Portfolio Health Check

My Portfolio Health Check - D

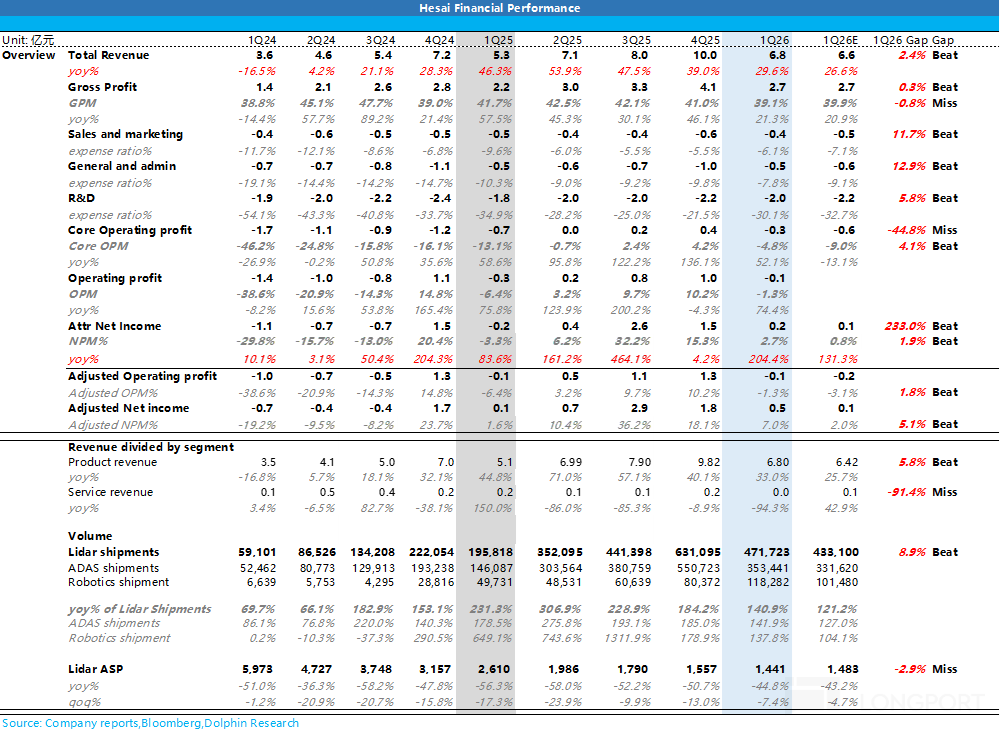

HSAI: Cut Losses, Hold the Line — Sector Leader Under Pressure?

2026 will remain a 'price-for-volume' year for Hesai Group amid high-stakes competition.

+7

HESAIFinancial Analysis - D

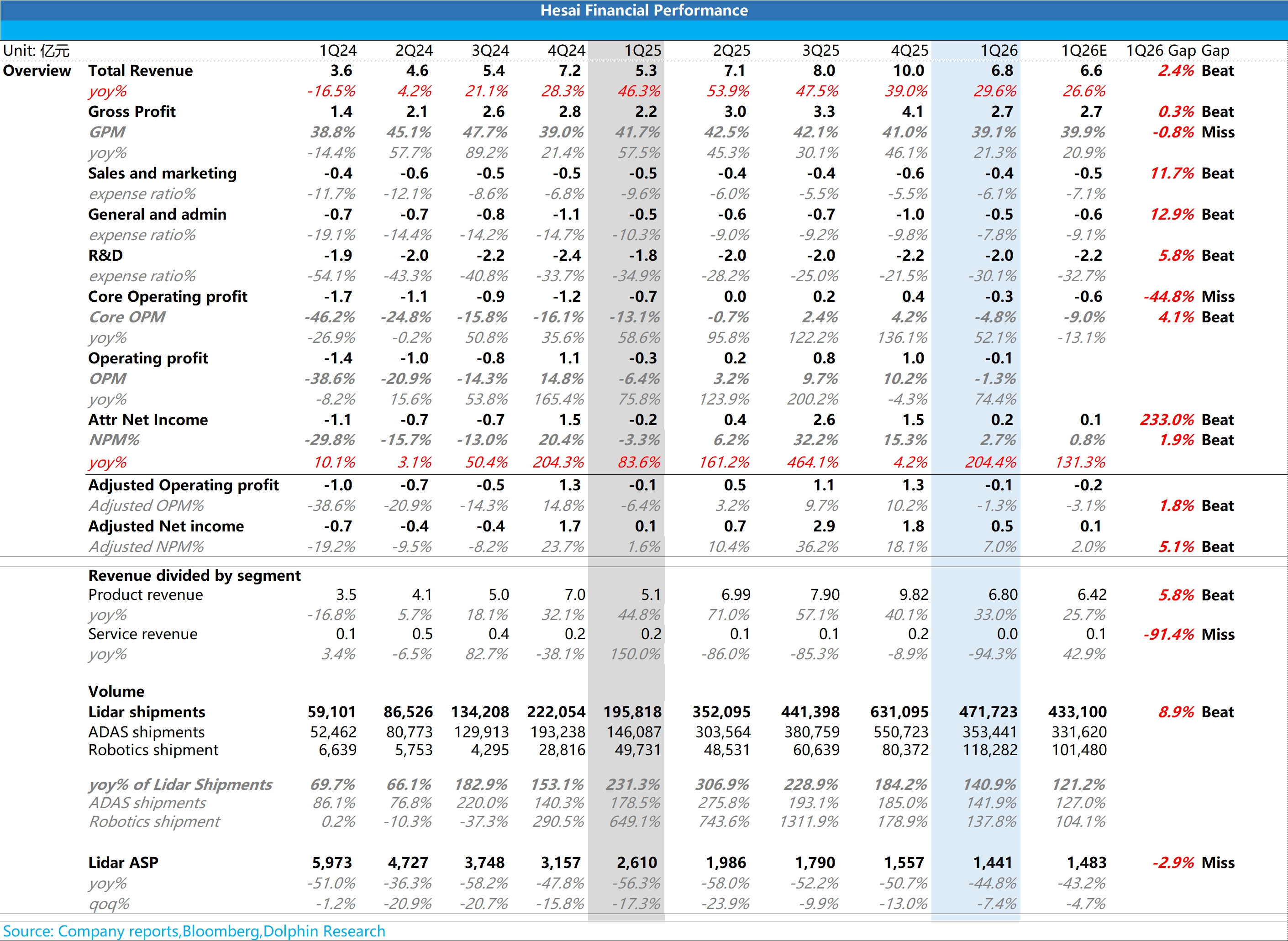

HSAI 1Q26 First Take: Slight beat overall, with revenue above the midpoint of guidance, but core OP remained in the red as ASP deflation weighed on margins.

1) Revenue: higher volume, lower price, slight beat

Revenue was RMB 684 mn (+28.7% YoY), landing toward the upper end of the RMB 650–700 mn guide. Growth was fully driven by shipments beating plan.

Shipments beat: seasonally soft quarter proved resilient, with ADAS and robotics as dual drivers.

Q1 is typically off-season, compounded by the phase-down of domestic NEV purchase tax incentives (domestic NEV sales -4% YoY), yet total shipments reached 477k units vs. 400–450k guided. This again underscores accelerating LiDAR penetration into mid- to lower-end models.

ADAS shipments were 353k units (+142% YoY), led by the thousand-yuan ATX ramping in RMB 100k–200k models at BYD and Geely. The lower-priced blind-spot filler FTX also started to scale.

Robotics shipments were 124k units (+138% YoY), exceeding the 100k guide. Growth was driven by the JT series for lawn mowers and related use cases.

② ASP still deflating: intensified competition as the main driver

Blended ASP was about RMB 1,441, down 45% YoY and a further 7% QoQ vs. 4Q25. Despite a higher mix of higher-priced robotics LiDARs (up 13ppt QoQ to 25%), overall ASP was dragged down, reflecting both mix and price-for-volume competition.

a. Mix shifted toward lower-priced ATX (e.g., custom versions supplied to BYD and Geely) with unit price around RMB 800. This is well below the 2026 overall ATX Avg. of about USD 150.

b. The lower-priced FTX blind-spot filler (about USD 100) began to ship. This further pushed down blended ASP.

2) Gross margin: notably pressured, GPM fell below the key 40% threshold for the first time

GPM was 39.1%, down 260bps YoY, below the market’s 39.9% expectation and the company’s usual 40%+ level. This marks a break below a psychologically important line.

The decline was mainly because ASP deflation (-45% YoY) outpaced cost reductions from in-house chips, with scale benefits not yet realized. As a result, per-unit GP was under pressure.

3) Opex and profit: disciplined spend, but core OP still loss-making

Q1 opex totaled RMB 300 mn; against ~30% revenue growth, opex rose ~40% YoY, reflecting tighter internal management and a more refined operating approach. Cost control remained a focus despite growth investments.

Core OP came in at -RMB 30 mn, a small loss as ASP deflation compressed GP and seasonality limited scale leverage. Still, it was slightly better than the market expected. $Hesai(HSAI.US) $Hesai(HSAI.US)

- F

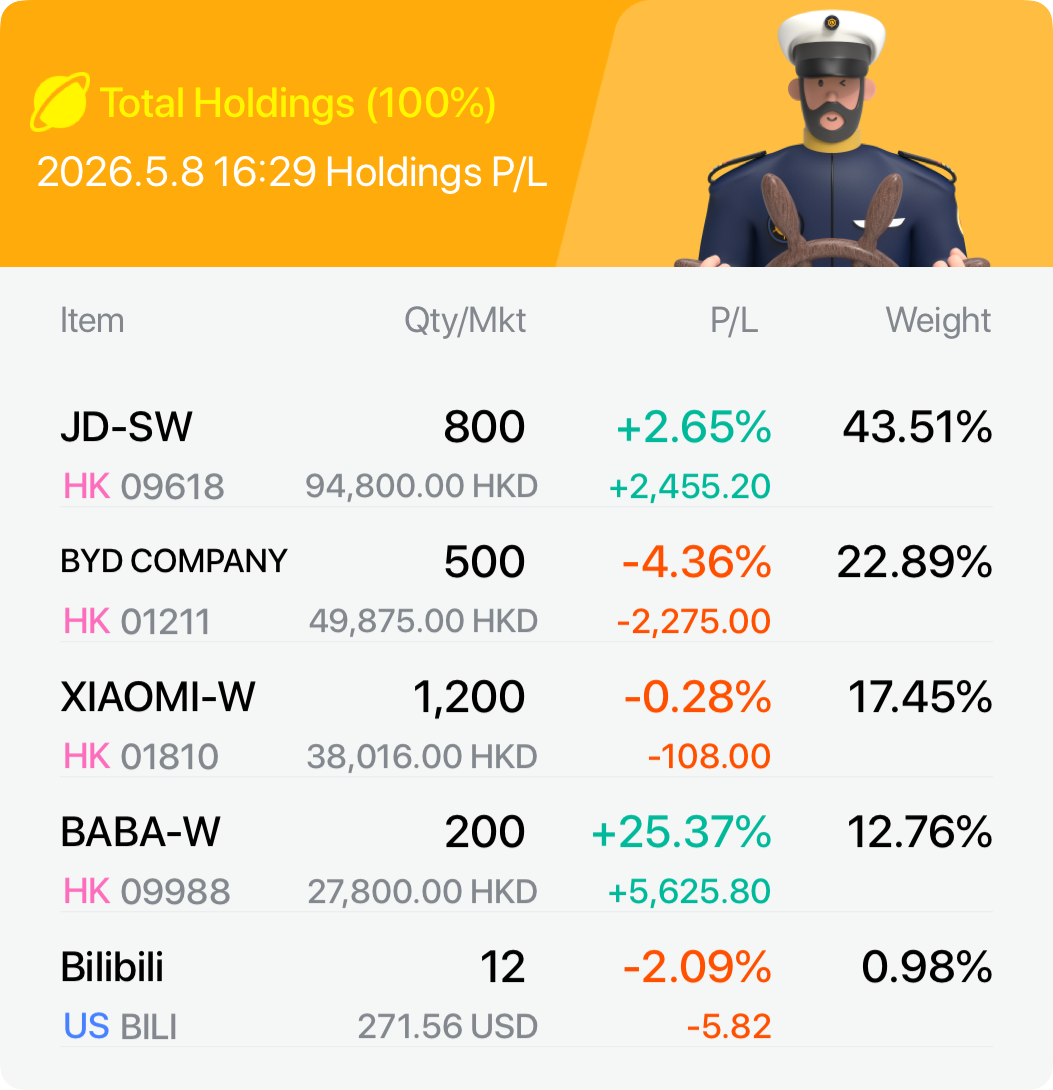

[Week 3] Portfolio Health Check: Navigating the May Earnings Season 🚗

1️⃣ Current Holdings

The core of my portfolio remains steady, centered on Technology and EV leaders.

My current sector distributions are:

🟢 Broadline Retail: 56.27% (JD & Alibaba)

🟢 Automobiles: 22.89% (BYD)

🟢 Tech Hardware & Peripherals: 17.45% (Xiaomi)

🟢 Interactive Media & Services: 0.98% (Bilibili)

My heavyweights are JD-SW (43.51%) and BYD (22.89%). I continue to hold Xiaomi and Alibaba, with a minor stake in Bilibili via the US market.

2️⃣ Earnings Watch

May is a massive month! I am keeping a close eye on these upcoming announcement dates:

🟢 JD.com: 12 May 2026 (Next Tuesday)

🟢 Alibaba: 13 May 2026 (Next Wednesday)

🟢 Bilibili: 19 May 2026

🟢 Xiaomi: 26 May 2026

The results and guidance from these giants will be crucial in shaping my strategy for the second half of the year.

3️⃣ Portfolio Reaction

I have not added any new positions this week. As of 8 May 2026, the portfolio is slightly in the green. Alibaba continues to be my star performer, sitting on a strong +25.37% gain, while JD.com is up +2.65%.

On the flip side, BYD has dipped -4.36%, with Bilibili (-2.09%) and Xiaomi (-0.28%) trading slightly below water. Fortunately, the solid gains in Alibaba are providing a great cushion.

4️⃣ Next Plan

I am looking to secure some gains. If the opportunity arises next week’s earnings, I plan to sell half of my JD.com position to lock in profits.

With current major markets at all-time highs, I want to increase my cash reserves to prepare for a potential downturn and buy high-quality companies at better valuations.

5️⃣ Risk Check

Concentration remains my main risk. My top two holdings representing over 66.4% of my capital. 😟

My exposure is heavily weighted toward Hong Kong and I am comfortable with this for now. At the meantime, I am actively looking out for global diversification opportunities.😉

My Portfolio Health Check

My Portfolio Health Check - D

Sanhua Intelligent Controls: Auto parts back in the black; how long until the robot boom?

Q1 revenue returned to positive growth. Back in positive territory.

+6

SanhuaFinancial Analysis - FFeatured

$BYD COMPANY(01211.HK)

BYD 1Q26: Profit Over Price Wars 🚀

(Sweet and Short Summary Review)

BYD’s latest results deliver a clear message: The global strategy is working. While total sales volume dipped, the company beat market expectations by focusing on “quality” profit rather than just raw numbers.

Three Key Takeaways:

1️⃣ Global Shift: Nearly half (47%) of BYD’s sales now come from overseas. Since international prices are 1.5x higher than in China, this expansion is successfully offsetting the “price war” back home.

2️⃣ Margin Resilience: Despite domestic discounts, BYD’s profit margin per car hit RMB 5.8k. This is nearly double what analysts predicted. Their vertical integration (making their own batteries) remains a massive competitive advantage.

3️⃣ Strategic Pivot: BYD has officially moved from a “domestic leader” to a “global profit machine.” They are choosing to capture higher margins globally rather than just fighting for market share in China.

🔷The Verdict

This report proves BYD can stay highly profitable even in a tough market. The long-term case for BYD as a global EV powerhouse remains firmly intact. 💎

Not financial advice. Always do your own DD!

- M

$Alibaba(BABA.US) is integrating its Qwen AI into cars from partners including BYD, Geely, Li Auto, and the SAIC-Volkswagen joint venture. Debuted and highlighted at the Beijing Auto Show, the voice AI enables in-car capabilities like food ordering, hotel bookings, and payments.

@Bridge Buzz SG

Trade Showcase: Trade, Show & Earn Rewards!

Trade Showcase: Trade, Show & Earn Rewards! - F

$BYD COMPANY(01211.HK)

Today’s Singapore Business Times headline reads: “EVs make up about 60% of car registrations in Singapore; BYD accounts for nearly one in four new cars.” It ready caught my attention😁

I invest in what I can see and understand. BYD remains a strong conviction for me and I added more to my position again last week.😉

Let’s go my green dragon 🐉.

Trade Showcase: Trade, Show & Earn Rewards!

Trade Showcase: Trade, Show & Earn Rewards! - F

$BYD COMPANY(01211.HK)

Is the world’s top EV maker charging up for a rally or stalling out? I am bullish on BYD Company Ltd (1211.HK) 🚀

The 4H chart and fundamentals flash bullish signals. Here is the breakdown:

🔹 Technical Snapshot

I am using Kalman Trend Levels Indicator by BigBeluge to filter the price data using dual time frame analysis. This indicator filters out market noise to reveal true price action.

❤️ Kalman Trend Shift: Price just broke above the green Kalman cloud (HKD100.0–HKD101.2). This is a major bullish signal, suggesting the long-term downtrend from HKD140.0 has finally neutralized.

❤️ Support & Resistance: Strong floor at HKD90.0 (blue ‘D’ and ‘S’ icons). Upside resistance at HKD125.0 remains the “boss level” BYD must clear to confirm a new bull market.

❤️ RSI (Relative Strength Index): Currently at 56.91. Healthy buying interest without being “overbought” (>70). Plenty of runway left before hitting a ceiling.

❤️ Momentum: Green arrows show successful “buy” signals as price bounced off HKD101.2 support.

🔹 Fundamentals (The Global Pivot)

BYD’s latest results (March 27, 2026) highlight a company in transition:

❤️ Revenue vs. Profit Trap: 2025 revenue hit HKD800B, but net profit dropped ~19% due to China’s brutal price war squeezing margins.

❤️ Export Engine: Raised 2026 export target to 1.5M vehicles (from 1.3M). Overseas sales now ~40% of revenue. International margins are far stronger than domestic.

❤️ Innovation Moat: Blade Battery 2.0 + “Flash Charging” (10%→70% in 5 minutes). Tech leadership keeps BYD ahead of Tesla in NEV volume.

❤️ Dividend Note: Payout ratio cut to 10% to fund global factory expansion (Brazil, Hungary, SE Asia). Great for growth but less immediate passive income.

My Verdict

🟢 ACCUMULATE / BUY ON DIPS

👉 The 2025 profit dip looks priced in. You are buying a global leader at valuations reflecting domestic fears while ignoring massive international expansion.

- D

BYD: Crown Lost; A 'Toyota' Abroad Next?

$BYD COMPANY(01211.HK) released its 2025 Q4 results after the HK close on the evening of Mar. 27 (Beijing time). Key points:

1) Revenue beat but driven by BYD Electronics; auto sales revenue in line: In Q4, total revenue was RMB 237.7bn, slightly above the RMB 236.7bn consensus, mainly on strong QoQ growth in non-core businesses, notably BYD Electronics.Auto sales revenue was RMB 181.5bn, in line with expectations, but vehicle ASP continued to trend down.2) Vehicle ASP still on a downward path: Vehicle ASP remains on a downward trajectory.In Q4...

+16

BYDFinancial Analysis - F

$BYD COMPANY(01211.HK)

BYD is at a crossroads! Tomorrow earnings are their big test. Can they prove their status as a global EV powerhouse?🤔

Key Data Summary:

❤️Trailing P/E Ratio: 23.09

❤️Price to book ratio: 4.03

While the long-term vision is strong, the numbers tell a cautious story. With the stock trading near the top of its historical range (0.98 valuation percentile), there’s a lot of priced-in expectation. Watching closely to see if the international growth justifies the premium!

NewDiscussionZones - D

US 'easing' on H200 chips hits a wall; TCOM tumbles late on antitrust probe | Daily News Recap

0114 | Dolphin Research Focus: 🐬 Macro/Industry 1) The China Chamber of Commerce to the EU said talks on the EU's anti-subsidy probe into Chinese EVs have made solid progress, with the EU set to replace countervailing duties with price undertakings. Eligible Chinese auto exporters can apply for assessment to obtain tariff exemptions, and the framework follows WTO rules and the non-discrimination principle, giving exporters clearer visibility for shipments to Europe. This helps defuse the China‑EU auto trade dispute, benefits major exporters such as BYD and SAIC, and supports value‑chain and supply‑chain stability.

2) With CSRC approval, the Shanghai, Shenzhen and Beijing exchanges issued a notice to adjust the margin requirement for margin financing. The notice adjusts the margin requirement ratio... Today’s Key News Recap

Today’s Key News Recap - D

XPeng wins Guangzhou L3 road test permit; BABA's Tongyi Wanxiang 2.6 adds role-play capability | Daily News Recap

1216 | Dolphin Research Focus: 🐬 Macros/Industry. The U.S. Bureau of Labor Statistics will release on Tue a closely watched 'combined' Oct–Nov nonfarm payrolls report. Street expects -10k in Oct and +50k to +130k in Nov, with the unemployment rate rising to 4.4%–4.5%, while Gov. payrolls will be weighed by deferred exits under delayed separation plans across Oct–Nov.

🐬 Single stocks. 1) $Alibaba(BABA.US) rolled out the Wanxiang 2.6 model suite... Today’s Key News Recap

Today’s Key News Recap - D

Horizon Robotics: Can China’s AD substitute chips unseat NVDA?

Horizon Robotics: An NVDA alternative for high-end autonomous driving?

+21HorizonDeep Research

+21HorizonDeep Research - L

Why does Li Auto want to divert its energy to making glasses? Glasses seem more like an AI label to make up for the sales decline, including the previously independent app of Li Auto's assistant, which was all the rage at launch but has long been forgotten. I always feel that Li Auto's R&D investment is too obviously utilitarian. If a strategic direction is identified, it should be continuously invested in without a financial investment perspective.

For example, BYD's DMi sat on the bench for years, but the performance of the models launched after its release was significantly improved, and it succeeded in competing with Toyota and Volkswagen in China.

Where is Li Auto's focus on continuous investment? If it defines itself as an AI company, isn't smart cars themselves focused enough? Smart driving and chips are not in the first tier either.

As a contrast, I actually agree with NIO's investment in strategic directions, such as battery swapping and service ecosystems. These are moats that require long-term capital, manpower, and technology to build and are hard to replicate.@Future Trader Pi Kanchuan

$Li Auto(LI.US)$NIO Inc(NIO.US)