$Expedia(EXPE.US) daily looking like a potential temp top at overbought with neg'd MACD. Time for basing/pullback?

Source: Sunrise Trader

Write something you'd like to share with our community...

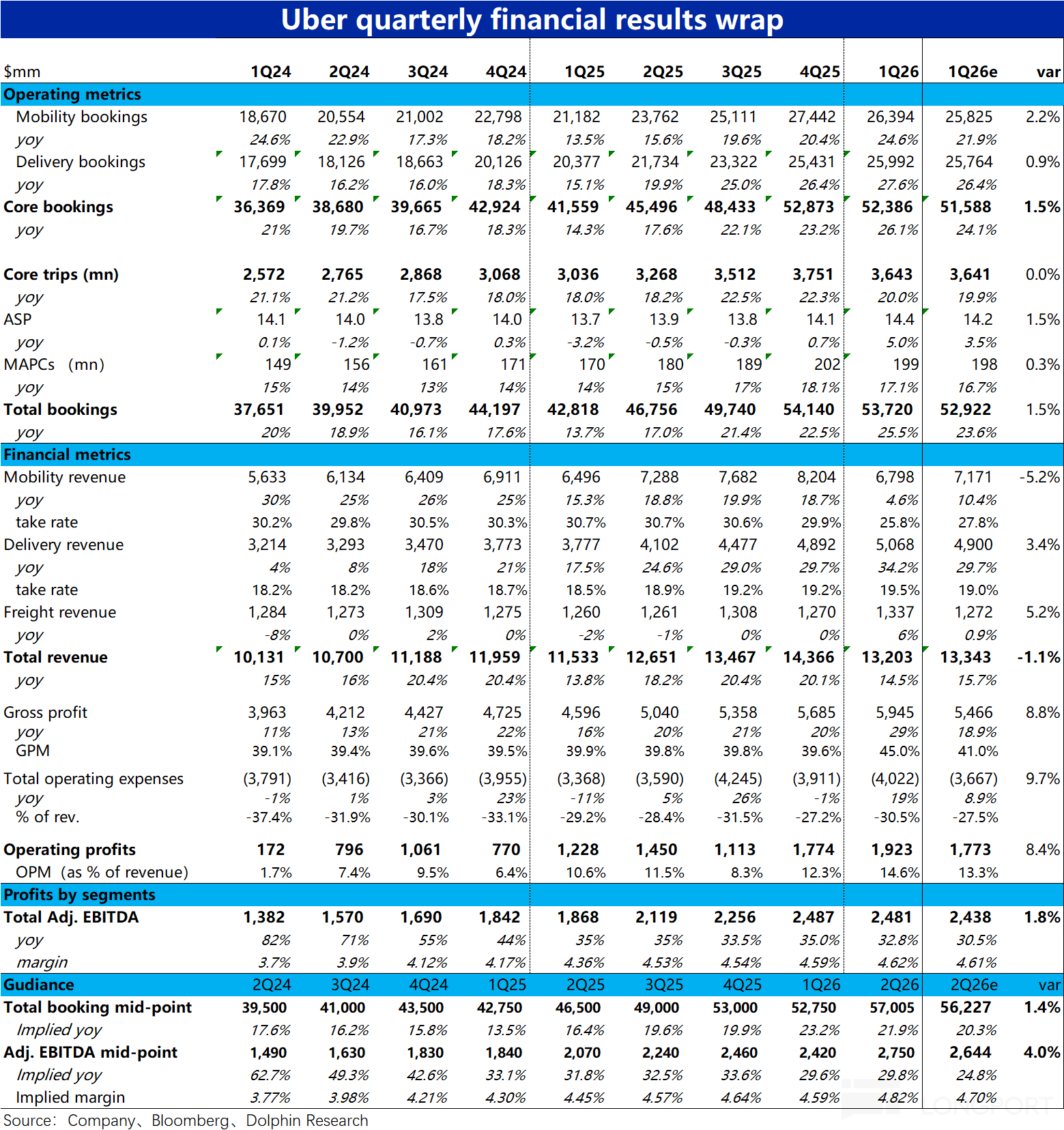

Below is Dolphin Research's compilation of the $Uber Tech(UBER.US) FY26Q1 earnings call transcript.

For our earnings analysis, see 'Uber: Results on track, but the Robotaxi threat lingers'. I. Key takeaways: 1) Shareholder returns: A record $3bn was returned to shareholders via buybacks this quarter. 2) Guidance: Management guides to continued growth momentum with disciplined capital allocation and a focus on sustainable profitable growth; it expects U.S. Mobility to keep accelerating through 2026...

$Expedia(EXPE.US) daily looking like a potential temp top at overbought with neg'd MACD. Time for basing/pullback?

Source: Sunrise Trader

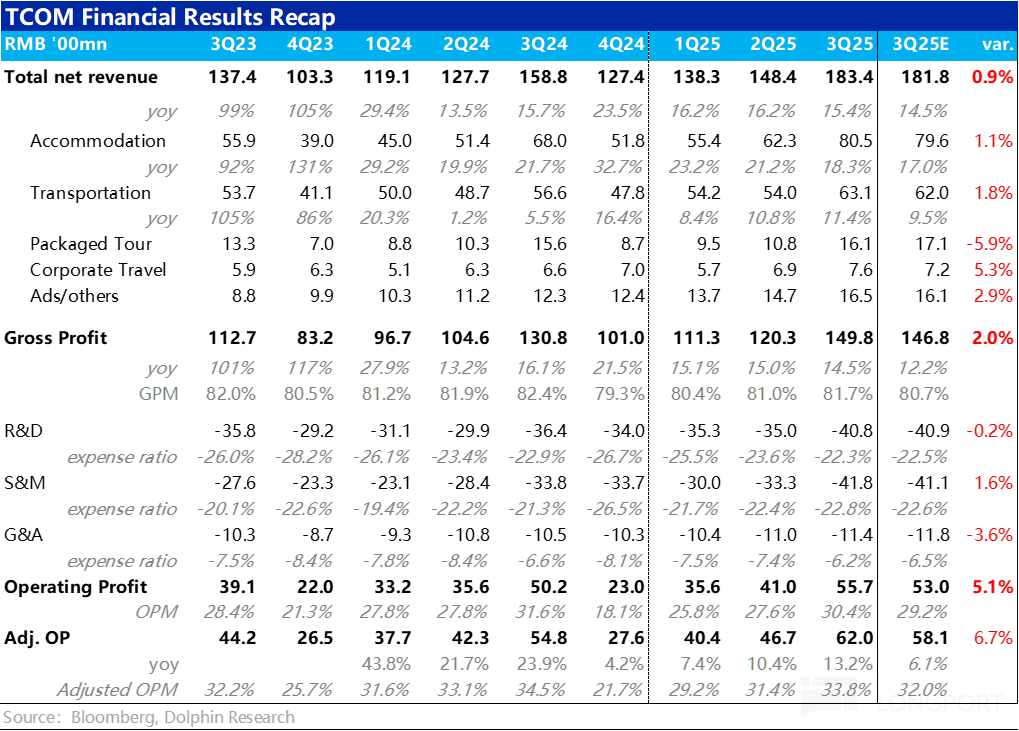

The following are the minutes of the FY25Q3 earnings call for $Trip.com(TCOM.US) organized by Dolphin Research. For an interpretation of the earnings report, please refer to "Trip.com: Awaiting the Release of Overseas Profits." I. Review of Core Financial Information II. Detailed Content of the Earnings Call 2.1 Key Information from Executive Statements 1. Strong Market Demand: The global tourism industry is booming, with travel enthusiasm surging. Travel demand is skyrocketing, primarily driven by the robust vitality of domestic tourism in China and the steady recovery of outbound travel. Travelers are actively exploring new destinations, seeking authentic and in-depth cultural experiences...

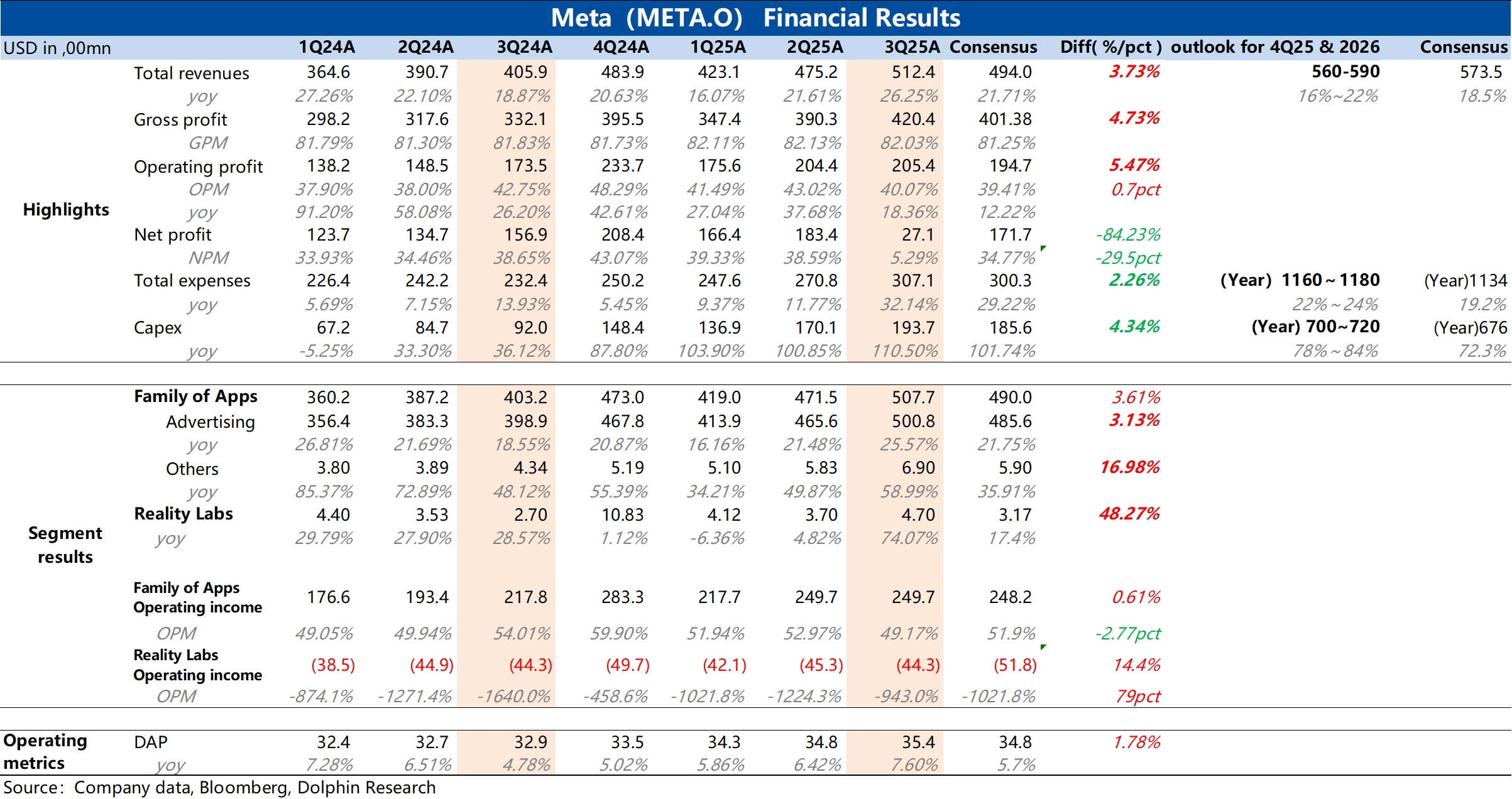

Meta3Q25 Quick Interpretation: At first glance, a company with a market value of $2 trillion having a quarterly profit of only $2.7 billion seems like a major flop! However, the net profit was mainly affected by a one-time provision of $15.9 billion due to the OBBB Act in the third quarter.

Excluding this factor, Meta's overall performance from revenue to expenditure is in a "high revenue, high expenditure" state. The 26% year-on-year revenue growth is quite impressive, but it did not exceed the current buy-side expectation range of approximately $51-52 billion. On the expenditure side, due to high increases in R&D and administrative expenses, the operating profit of $20.5 billion, with an 18% year-on-year growth, is not particularly outstanding compared to the revenue growth rate.

Of course, these are minor issues. The main concern is the upcoming guidance, which hits the market's "nightmare"—Opex & Capex. Whether for 2025 or 2026, both quantitative and qualitative aspects are generally being raised:

a. The 2025 Opex baseline is raised by $2 billion, reaching $116-118 billion. Based on the new midpoint estimate, the year-on-year growth in operating expenses for the fourth quarter will reach 37%.

b. In comparison, the 2025 fourth-quarter revenue guidance is $56-59 billion, with a year-on-year growth of only 16-22% (versus the buy-side expectation of approximately $58-60 billion). Clearly, fourth-quarter revenue growth is slowing. Based on this revenue and expenditure guidance, even if the highest revenue guidance of $59 billion is achieved, with the midpoint expenditure guidance, operating profit growth is likely to slow to around 10%+.

c. The 2025 Capex baseline is raised by $4 billion, with new guidance at $70-72 billion. Fourth-quarter capital expenditure will further increase to $20 billion from the third quarter's $19.4 billion.

d. The growth opportunities in 2026 are too tempting. Although specific data for 2026 capital expenditure has not been finalized, it is expected to "invest aggressively" through self-built and third-party co-built data centers, with the absolute value of capital expenditure "notably larger."

e. 2026 operating expenses: The growth rate in 2026 will be significantly higher than in 2025, mainly due to higher cloud expenses and amortization of infrastructure costs. This is actually because of the substantial recruitment of AI and technical talent in 2025, leading to a significant increase in employee expenses.

In this context, a market value of $1.89 trillion matching a full-year post-tax operating profit of less than $70 billion in 2025 results in a valuation of around 28X. When these numbers are put together, it becomes apparent: if revenue growth in 2026 cannot accelerate but investment increases, performance will clearly be in a mismatch period of input and output, causing EPS growth to slow to the low-teens or high single-digit growth range. Moreover, in 2026, due to increased capital and operating expenditures, the space for shareholder returns will be squeezed.

In this situation, if the valuation continues to hover in the 25-30X range, it is clearly inappropriate, and Meta is very likely to experience a valuation correction. $Meta Platforms(META.US)

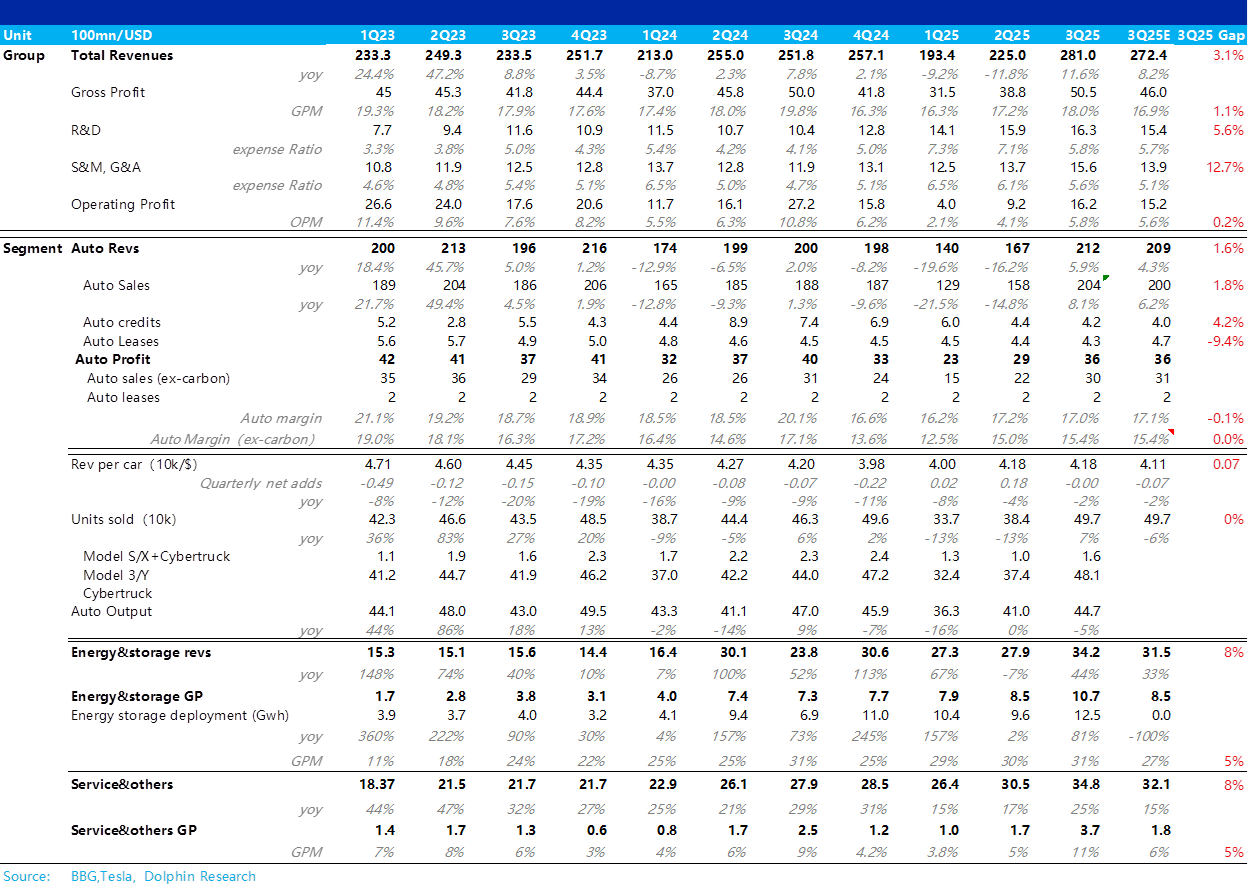

Tesla Quick Interpretation: Overall, regarding Tesla's third-quarter performance, the results are fairly decent. Both total revenue and total gross profit exceeded market expectations. However, net profit slightly fell short of expectations due to increased expenses.

From the perspective of the automotive business, which is the market's primary concern, Tesla's third-quarter vehicle sales revenue surpassed expectations. The core reason is that the market anticipated a quarter-on-quarter decline in Tesla's vehicle sales revenue, but the actual performance showed that the average selling price remained stable compared to the previous quarter.

Dolphin Research believes this is mainly due to Tesla raising the prices of Model S/X in the United States and launching the higher-priced Model L version in China, offsetting the discounts on inventory Model 3/Y vehicles and loan discount offers in various regions.

Regarding the most critical vehicle gross margin (excluding carbon credits), this quarter's vehicle gross margin improved quarter-on-quarter, aligning with market expectations. The quarter-on-quarter improvement in vehicle gross margin (excluding carbon credits) is attributed to the quarter-on-quarter increase in delivery volume, which released scale effects and reduced fixed per-unit amortized costs.

However, Tesla was still affected by over $400 million in tariffs this quarter, increasing the variable cost per vehicle. Ultimately, the automotive business gross margin was generally in line with expectations.

Since the second-quarter report, Tesla's stock price has reached a high of 439, which already reflects relatively full expectations for AI business and the upcoming mass production of Optimus. Therefore, compared to the third-quarter performance, the market is more concerned about the progress of Tesla's anticipated business.

In this earnings call, it was confirmed that the reduced configuration version of Model 3/Y has replaced the plan for the low-cost Model 2.5. Instead, Tesla is more focused on the mass production of the autonomous Cybercab (expected to start mass production in Q2 next year). Due to the U.S. IRA subsidies phasing out in the fourth quarter, U.S. demand will face significant pressure. Without the support of Model 2.5, the fundamentals of vehicle sales in the fourth quarter are expected to continue deteriorating.

Additionally, the release and mass production plan for the Optimus 3.0 prototype has been further delayed (Optimus P3 prototype release in Q1 2026, with mass production planning starting at the end of 2026), undoubtedly pouring cold water on the anticipated business. $Tesla(TSLA.US)