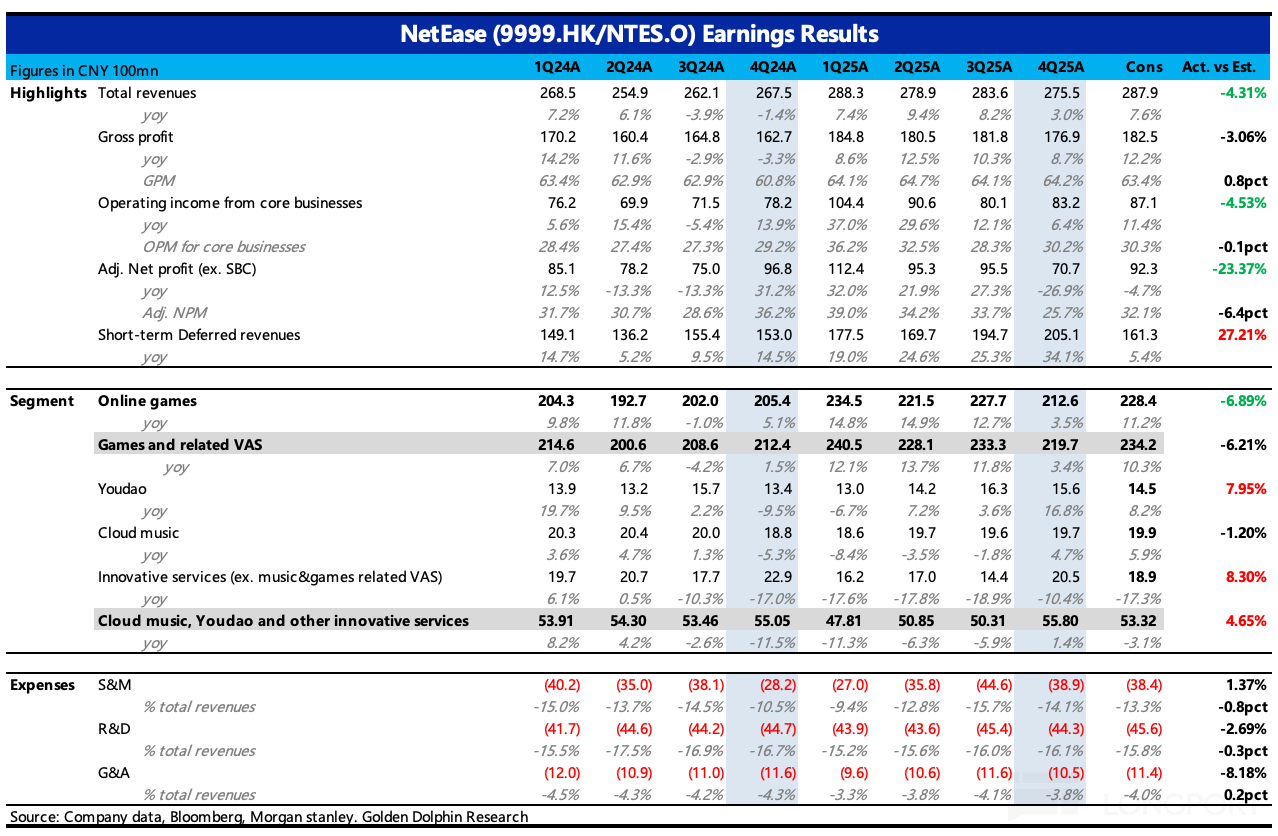

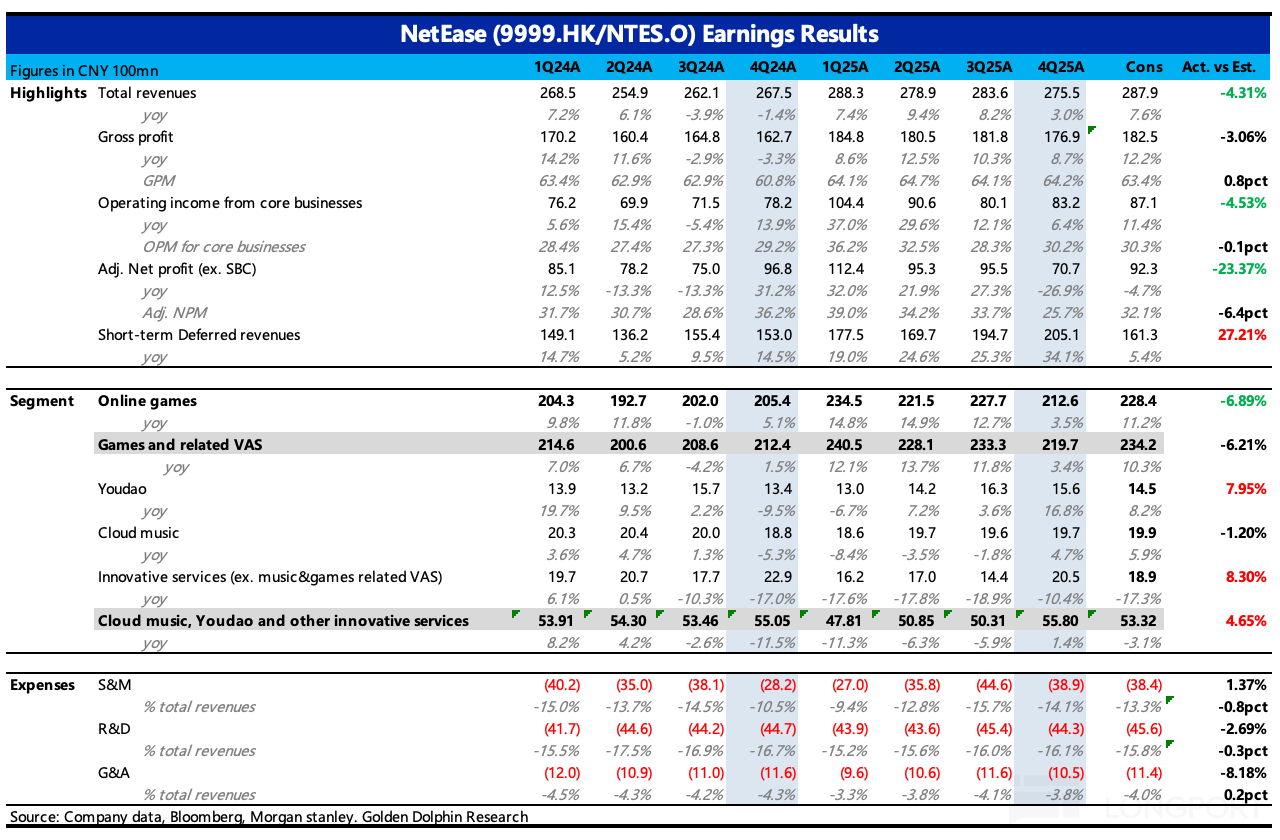

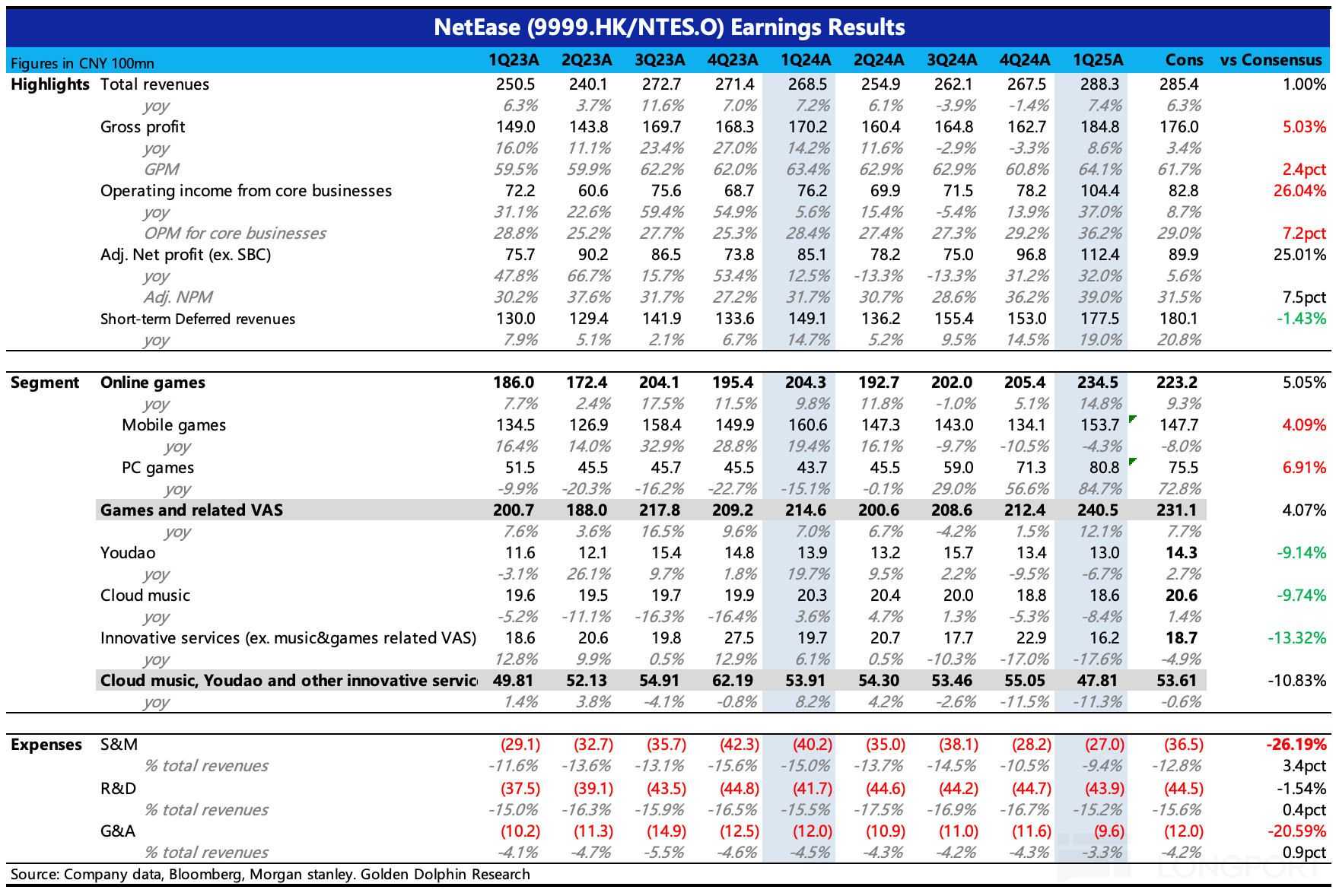

$NetEase(NTES.US) Double Beat? Not enough for Mr. Market

EPS: $2.56 vs $2.02 estREV: $4.435B vs $4.200B est🟥 -5.17%D

New U.S. tariffs take effect today; Tencent Cloud launches R&D agent CodeBuddy NPC | Daily News Recap

0724 | Dolphin Research Focus: 🐬 Macro/Industry 1) At 00:01 ET Fri (12:00 BJT on Jul 24), the U.S. rolled out a new import tariff schedule with rates of 10%–12.5% across ~60 economies, replacing the expiring global temporary tariffs. Based on Section 301, rates vary by economy, with exemptions for food, fuel, and certain industrial goods. Heightened unilateral trade barriers could exacerbate global trade frictions, weigh on profit expectations for export-oriented manufacturing supply chains, and near term dampen market risk appetite...

Today’s Key News Recap