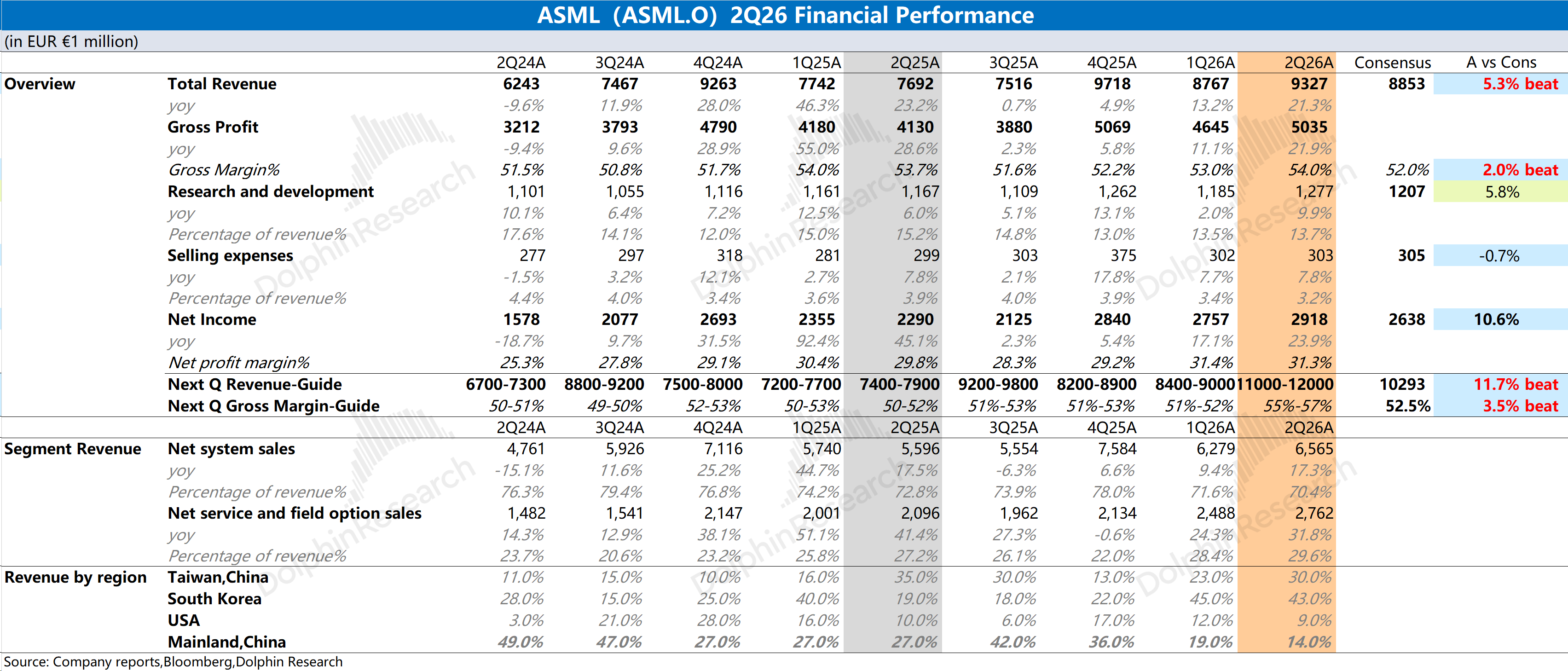

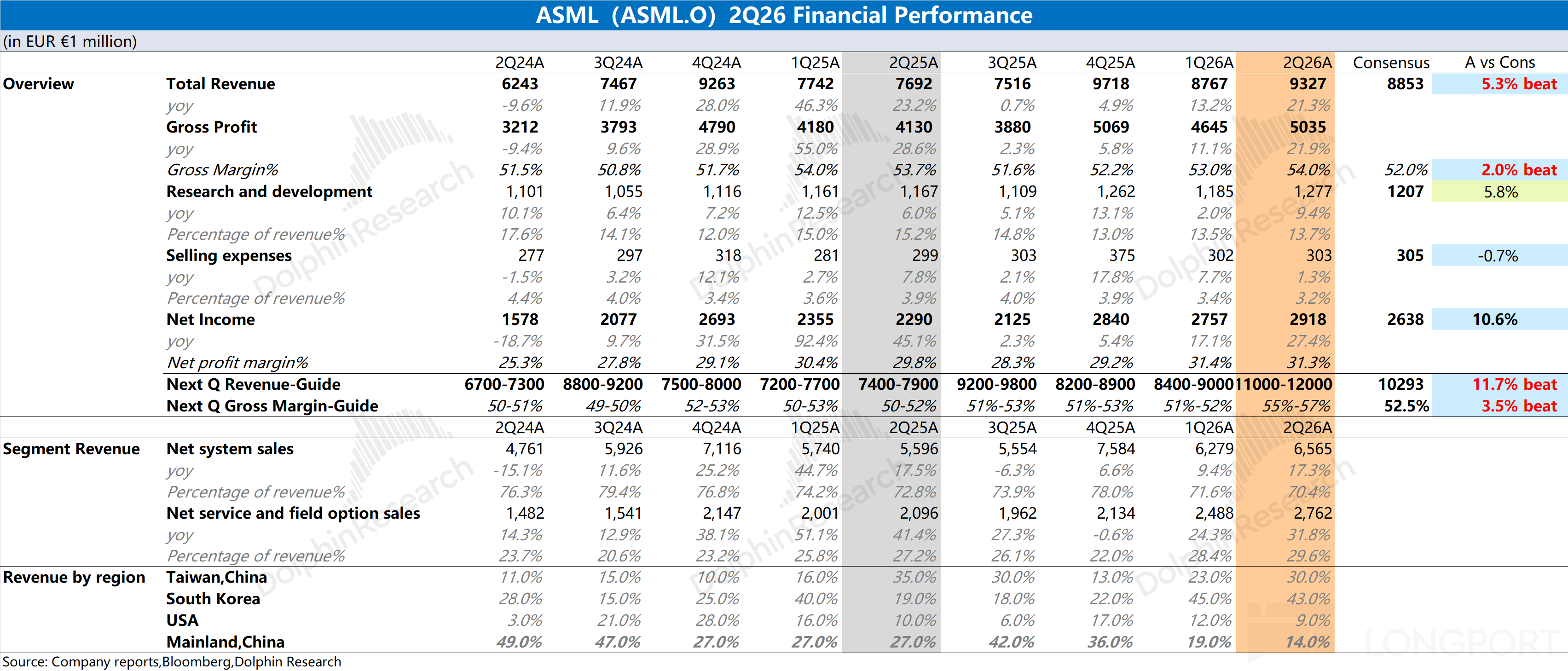

ASML First Take: A solid print, with revenue and GPM beating estimates. Growth re-accelerated, driven by pull-ins from TSMC and Korean memory customers.

Guidance was the standout. Management guides next-quarter revenue at €11–12bn, well above the Street at €10.3bn.

Management also raised the 2026 full-year outlook to €43–45bn (from €36–40bn). That implies +31–37% YoY.

Street expectations were ~€39.5–40bn, so the new guide beats all forecasts and reinforces market confidence.Based on the guide, Q4 revenue could climb further to about €14–15bn. That suggests core wafer fabs will begin large-scale pull-ins in 2H.

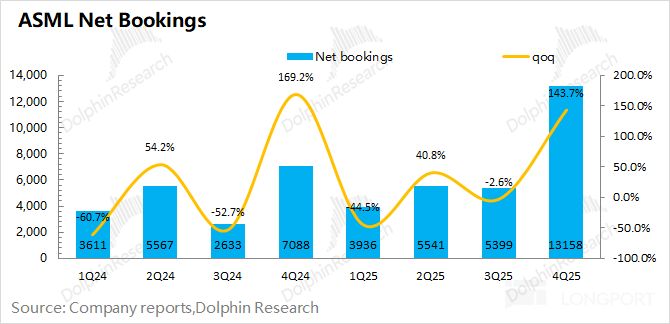

On orders, the company stopped disclosing detailed bookings starting last quarter. Bookings are a key leading indicator; watch for any color from management on the call (see Dolphin Research Trans to follow).

Despite the broad AI pullback, ASML’s drawdown has been relatively modest (~15%). Downstream wafer fabs are set to lift capex, and MU has again raised its capex outlook.

This should provide tangible earnings support.Overall, management’s sharply higher operational guide underpins 30%+ growth for the year and helps steady market sentiment. For more on orders and tech progress, please follow Dolphin Research’s upcoming detailed take and management call highlights。$ASML(ASML.US)