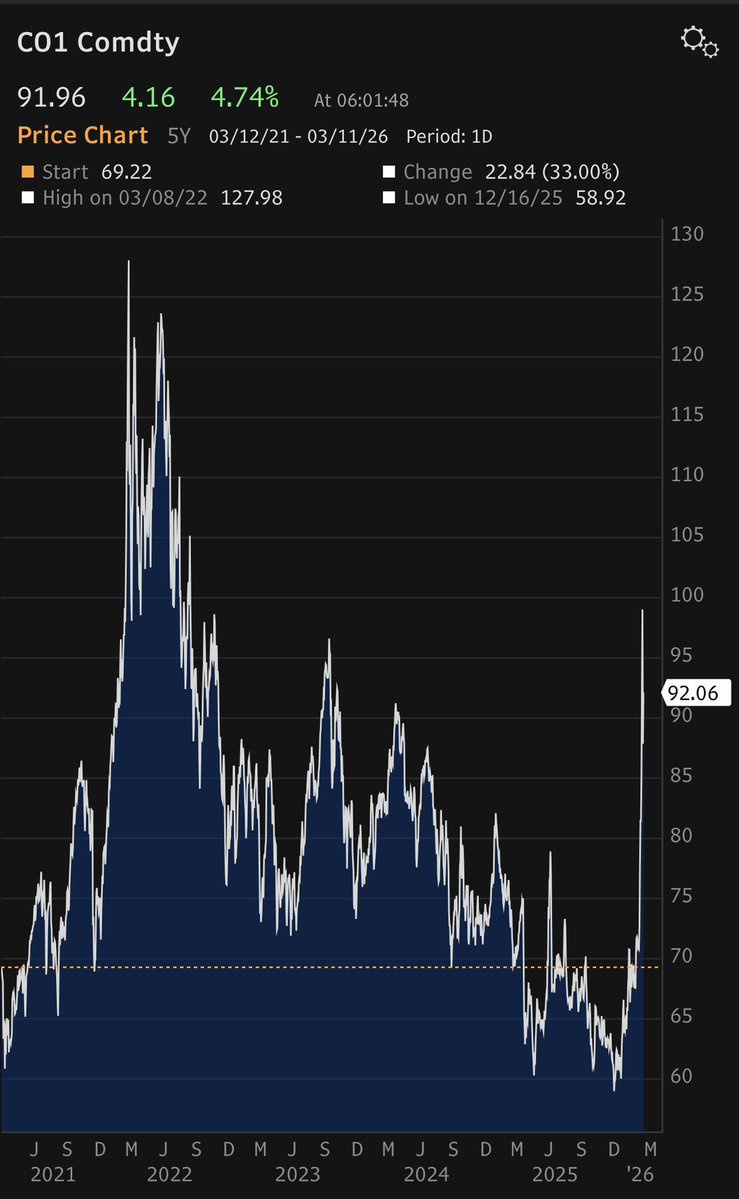

In today’s pre-mkt summary for Subscribers: Stocks flat as Brent crude climbed back above $90/bbl, with traders largely ignoring the IEA's proposed record 300-400 million barrel emergency reserve release, which would far exceed the 182M barrels released in 2022 post-Ukraine invasion. 10-year TYs rose modestly, gold was flat, and #btc fell. $Oracle(ORCL.US) surged +11% pre-mkt on a strong 3Q beat and raised FY revenue guidance driven by accelerating AI cloud demand, The VIX jumped to 26.

Today's Feb CPI print (pre-Iran conflict oil spike) precedes next week's FOMC meeting, where no interest rate change is expected and the focus will be on the updated dot plot and economic projections amid fears that sustained higher oil could delay rate cuts despite slowing employment. We see equities reclaiming new highs once the Middle East conflict resolves, oil retreats, and softer jobs data boosts Fed cut odds, with 2026 S&P 500 EPS forecasts at $310 implying a reasonable ~21.9x P/E = 4.6% earnings yield and a +50bp premium vs 10yr treasury yields in line with historic norms during non-recessions.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.