YUMC: How a 'Western chicken' ruled China for 30 years?

In China's famously high-volatility F&B market—where survival is a one-in-ten game—very few brands make it past 30 years and keep scaling. KFC, the 'foreign chicken' that entered China in 1987, not only survived but expanded to nearly 13,000 stores, turning fried chicken into a mass-market QSR with queues from Tier-1 CBDs to county street corners. Behind it, Yum China (YUMC / 9987) has become the largest restaurant operator in China.

In the secondary market, though, Yum China often wears a 'boring' label: a mature name with growth capped, a cash cow kept alive by buybacks. Interest has waned further over the past two years amid soft macro demand and SSS pressure. Yet despite the 'Western fast food is fading' narrative, the company has not slowed its store openings, total units are approaching 20k, and OP margin has risen steadily for multiple quarters.

In our view, Yum China is no longer a pure-play fast-food company, but a composite dining platform built on supply chain depth, digitalization, and localization. It appears to sell chicken and pizza, but in essence it sells a hard-to-replicate system of low cost, high efficiency, and strong repeat purchase. We unpack this through three questions:

First, what kind of business is Yum China? We frame the core economics before drilling into the drivers.

Second, how does it ride through cycles—where exactly is the moat? We focus on supply chain and digital capability.

Third, how much should a 'cash-flow machine' like this be worth? We outline both relative and DCF views.

I. What kind of company is Yum China?

1) It earns returns from a heavy-asset operating model

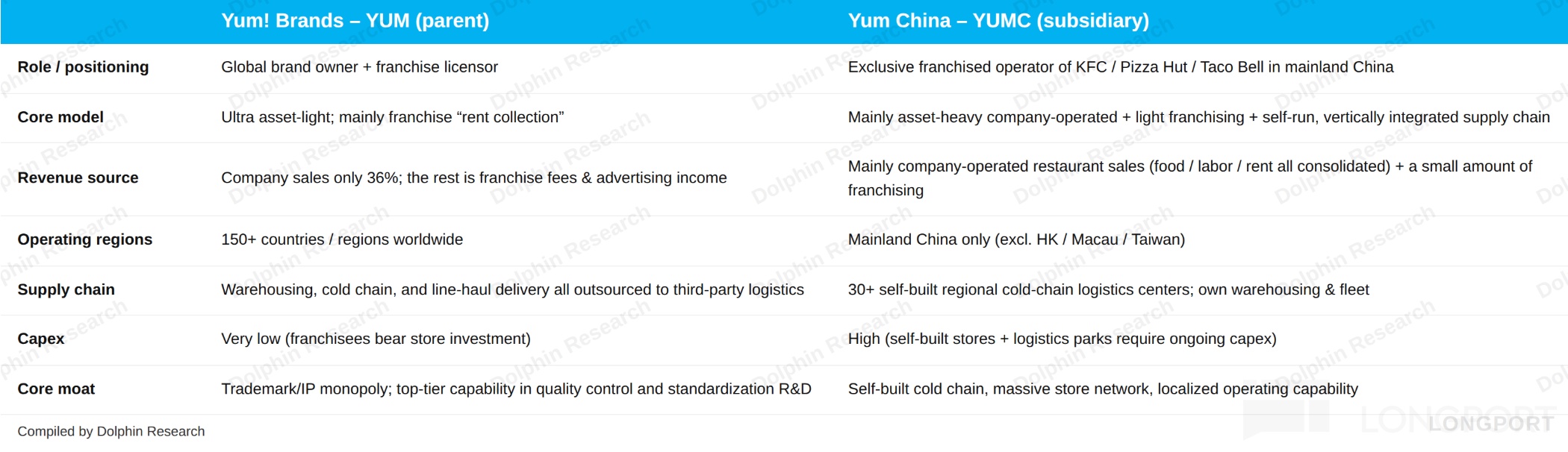

A frequent misconception is to equate Yum China with Yum! Brands. Spun off in 2016, Yum China secured exclusive rights to operate KFC, Pizza Hut, and Taco Bell in Mainland China, paying an approx. 3% royalty on system sales to the parent. The rights are exclusive within the region and are the backbone of the model.

As the table below shows, the two models are almost mirror images. The parent is a classic asset-light franchisor, with 98%+ stores franchised globally, essentially a fee-collecting cash machine. Yum China, by contrast, has long run a heavy-asset, company-operated model—leasing stores, fitting out, hiring, procuring, and running its own supply chain.

The revenue split makes this clear. In 2025, Yum China generated about $11.8bn in total revenue, with roughly 94% from company-operated restaurant sales. Franchise fees plus sales of food and packaging to franchisees via its supply network together accounted for only ~5%.

By brand, two powerhouses—KFC and Pizza Hut—define the base. Together they contribute over 90% of revenue, with KFC alone at about 74%, making it the primary focus of our discussion. The brand mix anchors scale and resilience.

Emerging brands—Little Sheep, Huang Ji Huang, Lavazza, and KCOFFEE—play the role of cross-category innovation labs. Their revenue and unit counts are far smaller than KFC and Pizza Hut, but they share Yum China's unified supply chain and digital backbone. That avoids building separate heavy-asset stacks and lowers the opex required for category testing.

2) China’s largest Intl QSR with 10k+ stores

On unit count, KFC is the largest QSR brand domestically, with nearly 13,000 stores by end-2025. Comparisons with chains like Mixue (40k) or Luckin (20k) miss the point—foodservice chain-ability is far more complex than standardized tea or coffee. The operational bar is materially higher for hot kitchen formats.

Most Chinese '10k-store' freshly prepared food concepts share one playbook: ultra-low price points, ultra-simplified operations, and minimal per-store capex. Players like Wallace (~20k) and Tastien (~10k) run with RMB 10–20 tickets, very simple back kitchens, and low-investment husband-and-wife formats. In short, scale is achieved by pushing entry barriers as low as possible.

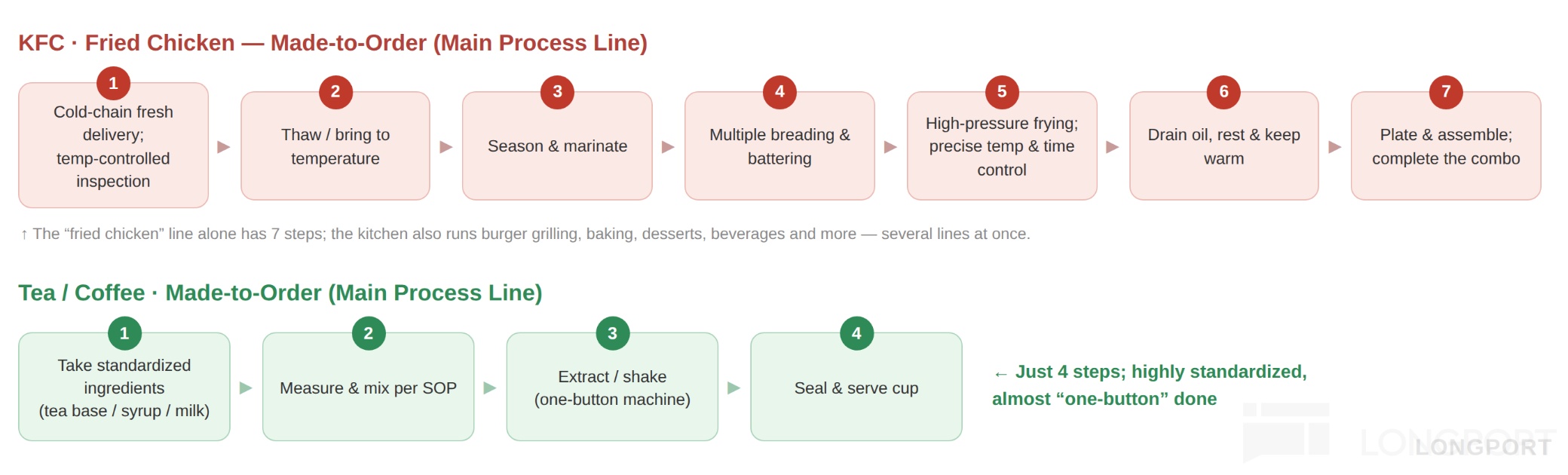

KFC does the opposite: positioned as a mid-market, standardized full meal with a RMB 35–40 ticket. Behind that are heavier kitchens (fresh fry with ~dozen steps), complex cold chain (fresh poultry under full temperature control), and million-RMB single-store capex. This requires an order-of-magnitude stronger supply chain and store management capability; any weak link shows as scale grows.

Under such high-bar constraints, KFC still scaled past 10k stores with stable quality—the only player to do so at this standard. Even McDonald's China, after 30+ years, remains below the 10k threshold at roughly 8,000 stores.

Dolphin Research

3) Multi-format portfolio to ride cycles

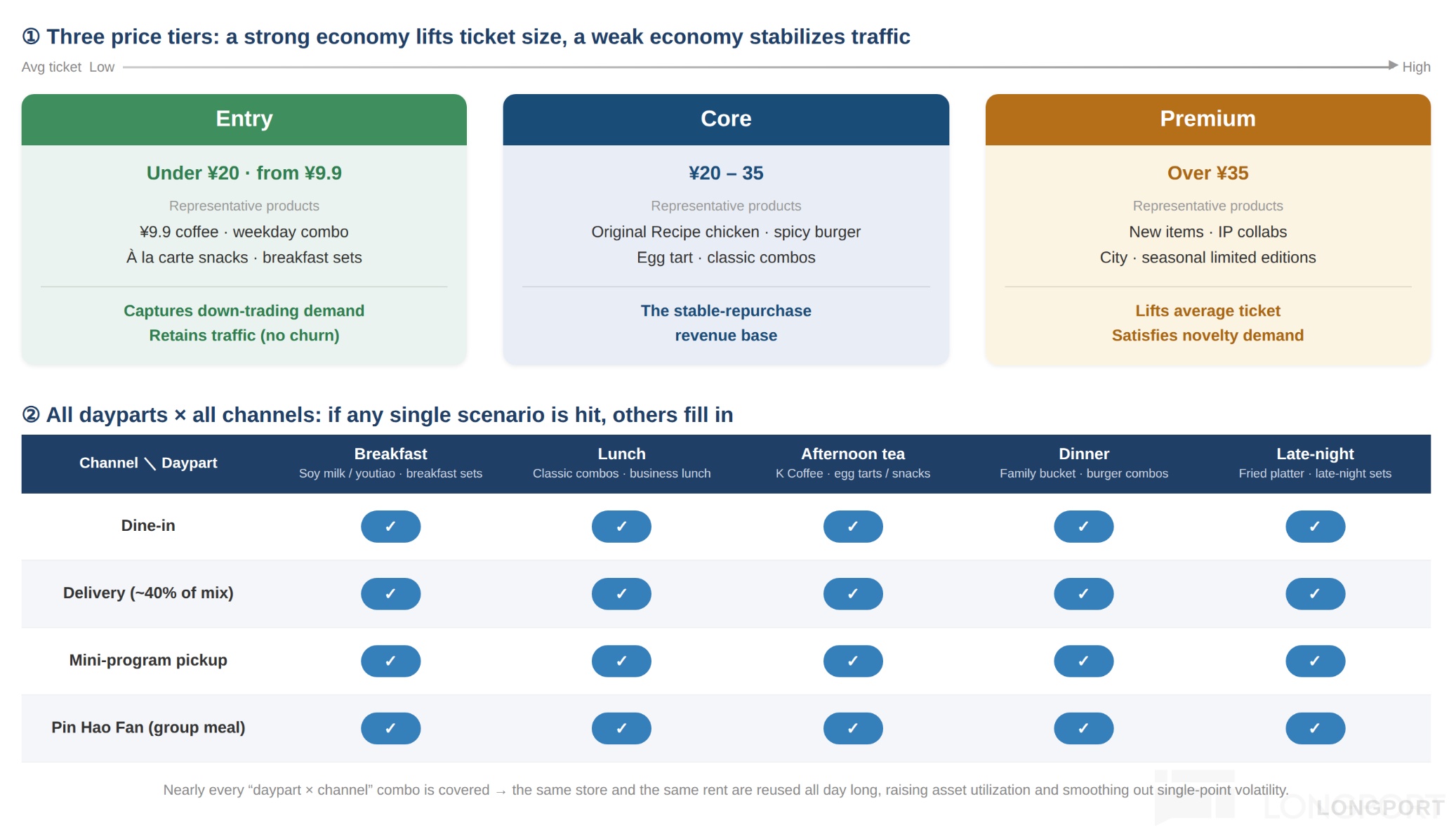

China F&B is notoriously cyclical and volatile: when demand weakens, table turns, tickets, and footfall often fall together, while category homogenization amplifies pressure even for leaders. Yet Yum China's revenue has been relatively resilient—down only 2.9% in 2022 at the trough for dine-in (vs. Haidilao’s ~20% decline), then rebounding in 2023.

Beyond supply chain-enabled footprint growth to offset weaker SSS, KFC’s coverage across three price bands—entry (from RMB 9.9), core, and upgrade—helps smooth the cycle. When macro is strong, premium items lift ticket; when weak, entry items absorb trade-down and preserve traffic. The all-day parts (breakfast/lunch/dinner/late night + afternoon tea) and omni-channel dine-in + delivery coverage also diversify shocks so that weakness in one occasion is cushioned by others.

In short, avoiding reliance on any single hero SKU, region, or occasion is a structural reason why revenue has been steady. We detail mechanisms below and show how they reduce drawdowns across cycles.

4) Top-tier profitability in the sector

On profitability, KFC’s restaurant-level margin has recovered from ~15% to ~17% over the past five years, firmly in the first tier. Global leading QSRs generally run 15%–20% at the restaurant level, placing KFC within the target band.

More important is the quality of that margin. The past few years were demand-soft, during which KFC leaned into value—RMB 9.9 bundles and 'Crazy Thursday'—to trade margin for volume. Despite lower tickets by design, restaurant margin rebounded to ~17% post-2022, indicating margin was not 'squeezed' by pricing, but driven by two internal levers: continued food cost deflation from supply chain scale, and labor productivity gains from digitalization.

In other words, this is a cycle-resilient margin derived from efficiency rather than price hikes. It is more durable than pro-cyclical margin spikes that depend on demand tailwinds.

Pizza Hut follows a different logic. As a CDR (Casual Dining Restaurant), it has larger boxes, higher dine-in mix, lower turn, and thus weaker fixed-cost absorption on rent and labor, naturally compressing restaurant margins vs. KFC’s QSR format. Still, by widening price bands, launching value traffic drivers, and rolling out WOW smaller-box formats to lower rent and labor, Pizza Hut has steadily repaired unit economics.

This underscores the reusability of Yum China’s platform—its integrated supply chain and digital backbone can lift even structurally weaker brands. Pizza Hut thus has tangible room for further margin repair within the group framework.

5) Asset turns drive steady ROE improvement

From a shareholder return lens, ROE recovered from 6.5% at the 2022 trough to 16.7% by 2025. A DuPont view shows net margin normalizing from ~4.6% to about 8%, reflecting profit recovery, while asset turns improved from 0.8 to 1.1 as in-store traffic returned and the mix shifts toward lighter franchising.

The equity multiplier has been stable near 2x, with payables and lease liabilities dominating non-interest-bearing operating liabilities and minimal financial debt. Coupled with sizable buybacks and ongoing dividends, management plans to return essentially all FCF to shareholders after minority distributions from 2027 onward. That points to attractive total shareholder return potential.

Putting it together, Yum China may not be a 'high-growth' story, but it wins on steady revenue across cycles with limited drawdowns and first-tier profitability. Add improving turns and buybacks supporting ROE, and you get a 'cash-flow machine' that compounds through cycles. How is this achieved? In our view, two true moats underpin it—supply chain and digital.

II. Core moats: supply chain and digitalization

1) Supply chain: the foundation

Chain restaurants look like brand businesses, but are fundamentally supply chain businesses. In a market like China—with large regional taste differences, stringent cold-chain needs, and widely dispersed store networks—without a deep local supply chain, a strong brand and savvy marketing will crack once expansion accelerates.

For a restaurant chain, the constraint on expansion is not just site selection or franchising. The question is whether each incremental store can be served with stable, low-cost, traceable supply while maintaining standards. Yum China does this on two pillars in our view:

1) Local depth + centralized procurement

First, centralizing purchasing from regions to HQ and locking in long-term supply agreements with leading upstream vendors is not unique—this is table stakes for world-class QSRs. McDonald's pioneered much of this, and Domino's likewise has long-term contracts and commissaries. Centralized procurement is simply an entry ticket; Yum China's edge lies elsewhere.

a) Procurement scale

In China, the core deflation lever in centralized buying is volume. More volume means more bargaining power upstream, and store count is the cleanest proxy. KFC’s ~13k stores are ~1.7x McDonald's China (~7.8k); layer in unified procurement across Pizza Hut, Taco Bell, and others, and Yum China’s aggregate local procurement volume dwarfs McDonald's.

As a result, Yum China holds stronger pricing power in standardized local inputs such as poultry, frozen fries, bakery, and seasonings. Raw material costs are typically 5%–10% lower than peers, providing structural cost advantage at scale.

b) Local depth: not just a higher mix, but faster execution

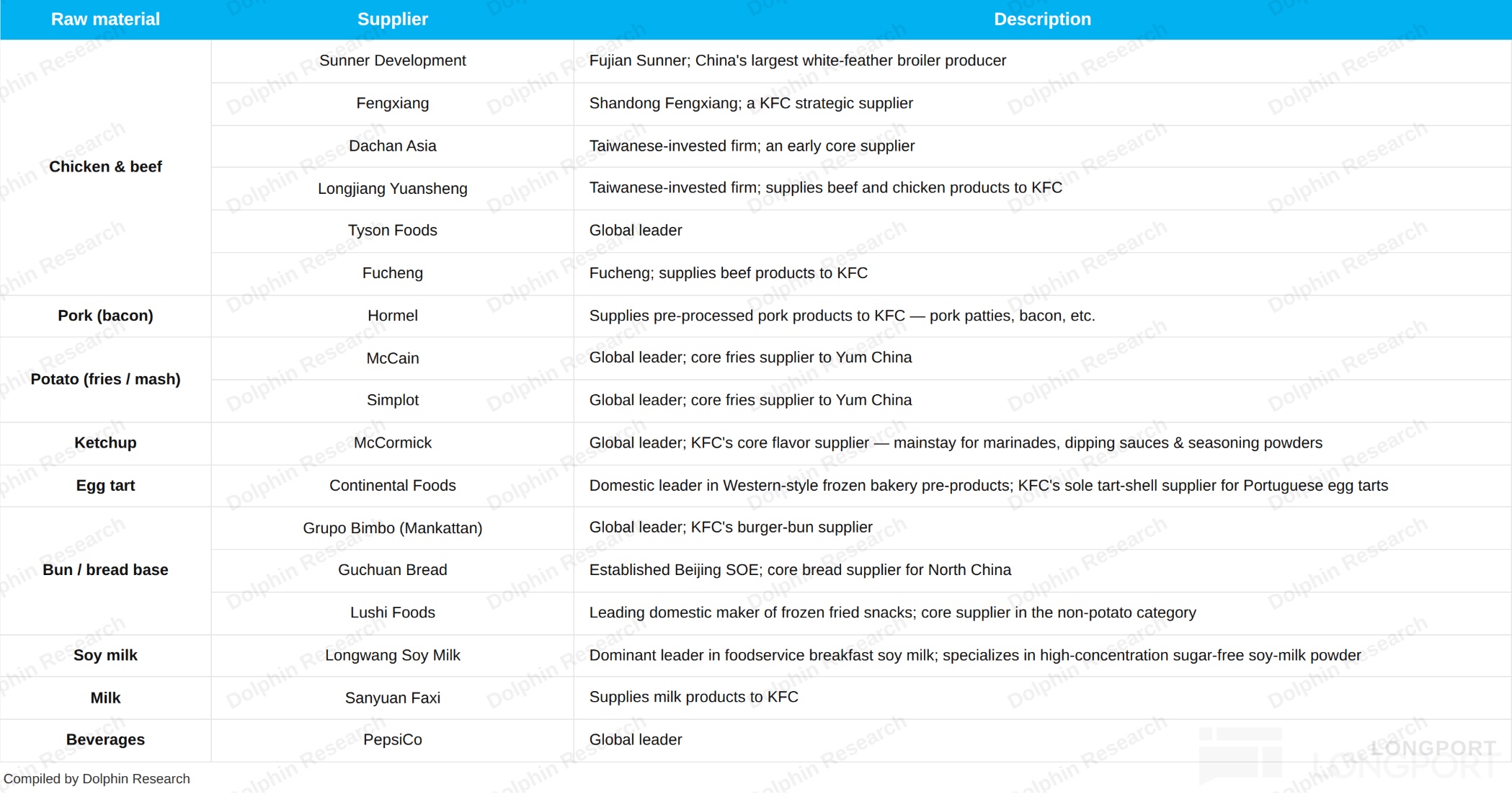

Over 90% of Yum China’s food inputs are sourced locally, with 850+ domestic suppliers by end-2025 covering 2,200+ SKUs spanning poultry, rice/flour, soy products, Chinese marinades, and regional specialties. This enables continuous, heavy localization—rice, fresh-ground soy milk, youtiao, and regional/seasonal items can be launched frequently.

The diversified, highly localized supplier pool brings two benefits: shorter logistics routes and lower single-supplier disruption risk, and faster co-development cycles with local manufacturers, allowing quicker iteration to local tastes. In contrast, while McDonald's China also sources 90%+ locally by value, it is tethered to globally synchronized external suppliers and standards. Changes to recipes or inputs must follow global protocols, lengthening local launch cycles and adding constraints.

The combination lifts bargaining power, batch consistency, and co-development speed, letting the back end absorb cost and buffer risks ahead of the store network. In effect, before 'opening stores' even happens, Yum China’s back end has already shouldered much of the cost and risk on behalf of stores.

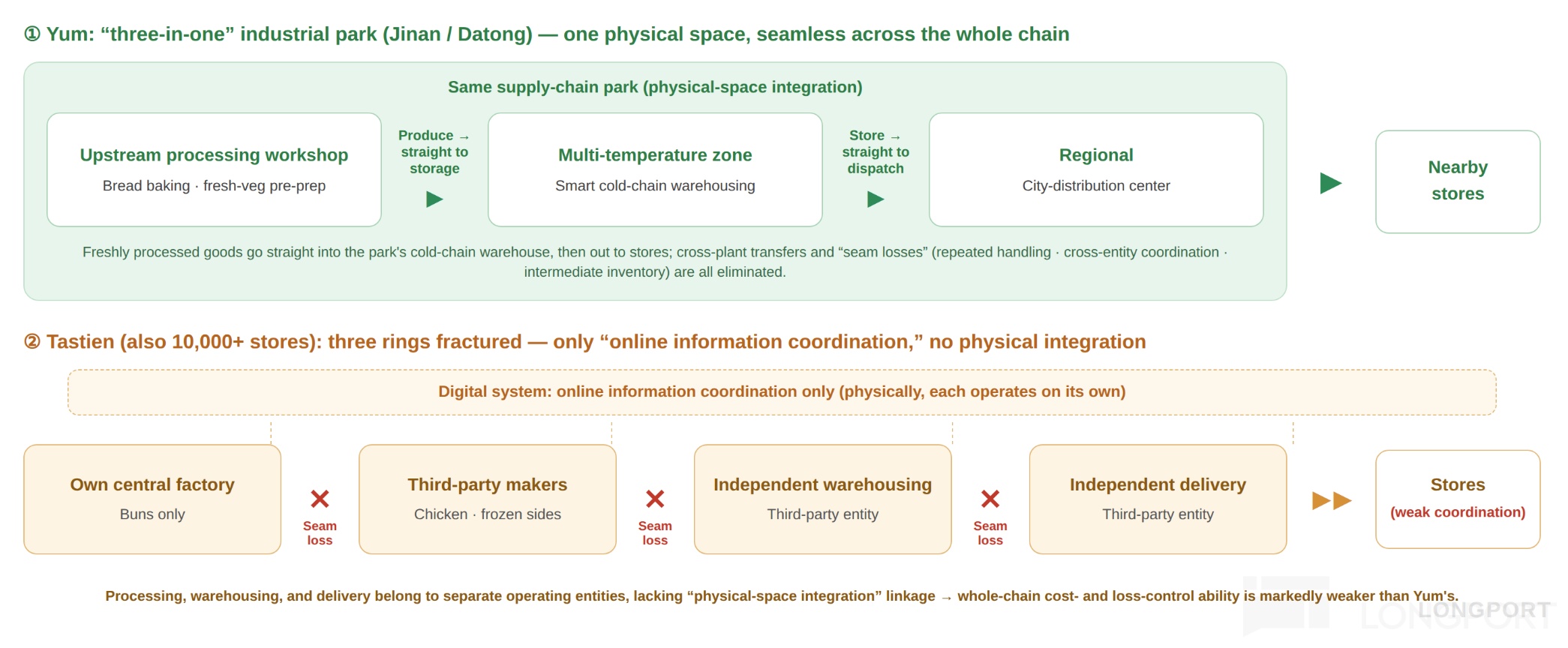

2) Self-built logistics parks: from warehouse to platform

On warehousing, processing, and transport, no single link is an impregnable moat. Trucks, automated warehouses, and processing lines are purchasable with enough capital and time—there is no exclusivity. In fact, McDonald's partner HAVI’s cold-chain system and Domino's commissary model may be stronger at individual links.

Yum China's strength is end-to-end orchestration. Within a single park, upstream processing lines (bakery, fresh-veg prep), multi-temperature smart cold storage, and regional distribution are co-located. This 'three-in-one' design shines with short-shelf-life items: 'produce to inbound, inbound to outbound' in near real time.

Freshly processed goods move directly into the on-site cold store and out to nearby stores without long inter-plant transfers. That saves not only freight but also 'interface losses'—extra handling, cross-party coordination, and buffer inventory. Turn improves materially, reducing working capital and waste.

By contrast, at 10k-store peer Tastien, these three links are largely disconnected. Only bun blanks come from owned central plants; poultry and frozen veg are bought from third-party suppliers, and processing, warehousing, and distribution are handled by separate entities. Digital systems coordinate information, but lack the added benefit of physical co-location.

2) Digitalization: the control tower

If supply chain is the foundation, digitalization is the control system. Most chains in China today do not truly 'own' their users. Even for a price promotion, many cannot deliver offers directly to users because traffic is not proprietary—dependent on mall footfall or third-party platforms like Meituan and Douyin.

This creates two risks: platform rule or subsidy changes can swing traffic sharply, and each order pays a platform take rate that erodes margins. Put simply, most restaurant brands are 'tenants' of platform traffic, not the 'landlords'.

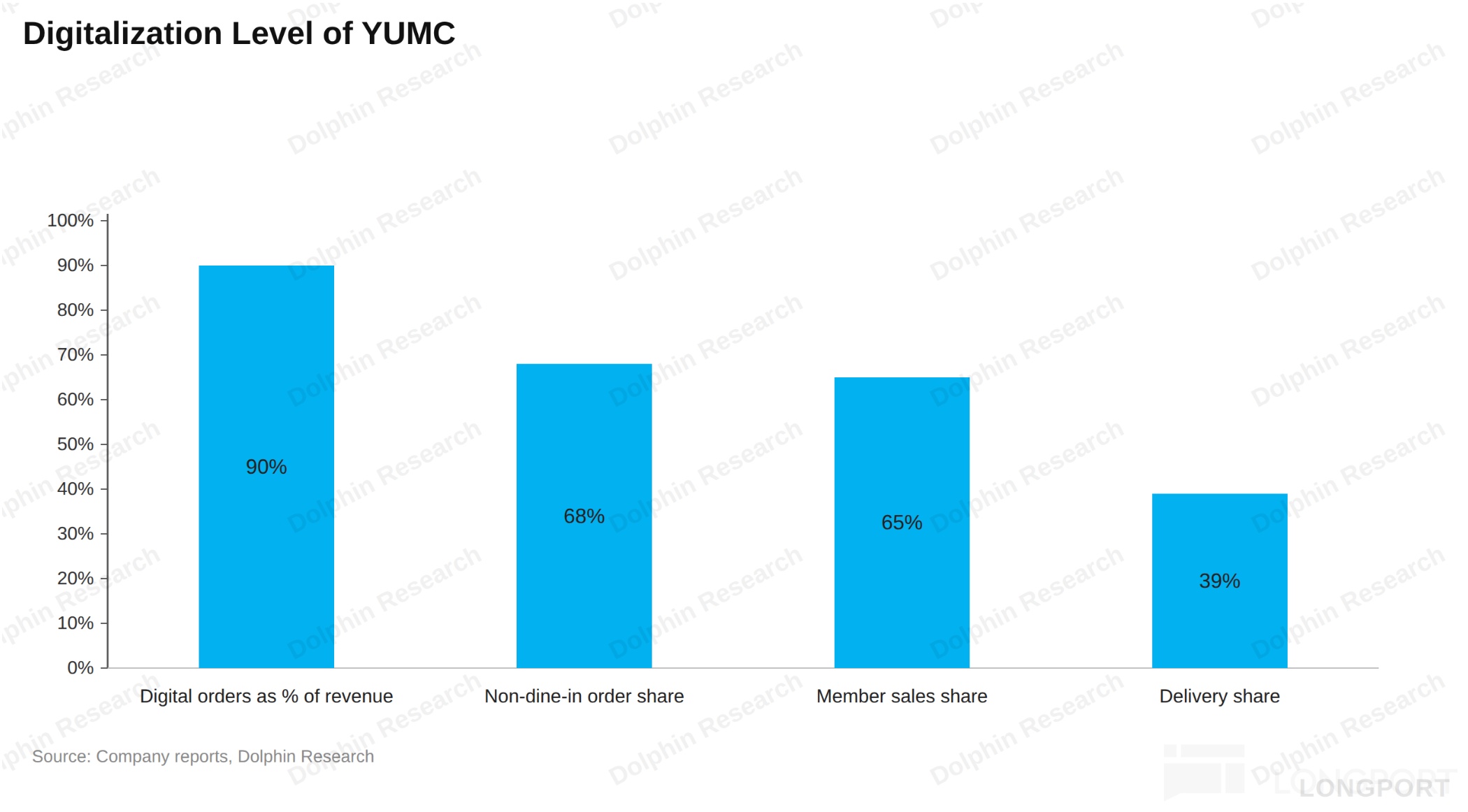

Yum China saw this early and began building out digitalization in 2015. It now operates a super-app-centric digital ecosystem, using app/miniprogram/membership/delivery to reach users at the front end and 'Yum Cloud' to empower supply chain and store ops at the back end.

As the chart shows, member sales now account for roughly 65% of revenue—first tier among global large-scale operators. Owning traffic is rare in F&B; the higher the share of proprietary channels and habits built around its own miniprograms, the more stable the SSS traffic.

'Crazy Thursday' is a case study of this digital muscle. Launched as a Thursday deal in 2018, it went viral in 2021 via user-generated 'Crazy Thursday literature'; the company then leaned in with an awards gala and the 'V me 50' card. By end-2025, the Weibo topic had 3.1bn views.

Results are two-fold: Thursday sales run ~50% above other weekdays, forming a stable mid-week peak, and the weekly ritual builds a repeat habit amplified by zero-cost UGC. A promotion was turned into a sustainable brand asset through digital and brand operations.

Ultimately, the power lies not in any single feature but in linking 'traffic acquisition → member capture → smart ops → repeat conversion' into a self-reinforcing loop. The more proprietary the channels and the thicker the private domain, the more precise the ops and the higher the repeat rate, which in turn lowers CAC.

III. How to value Yum China?

With the business quality mapped out, we turn to valuation. We lay out assumptions and outlook for each segment before triangulating on value.

For 2026–2030, growth can be decomposed into KFC, Pizza Hut, and 'Others'. The shared themes are lower-tier expansion, faster franchising, and modest SSS recovery, differentiated mainly by stage and cadence. We reflect these differences in unit and mix assumptions.

1) KFC: go lower-tier + accelerate franchising to build the next 10k

As of end-2025, KFC had 12,997 stores. Management guidance is clear: significantly accelerate franchising, lifting franchise mix in net adds to 40%–50% over time. This shifts capital intensity and unlocks more marginal sites.

The essence of faster franchising is to use smaller, lighter, lower-investment formats to make previously uneconomic low-tier locations viable. The 'KFC Town mini-store' is tailored for this push, matching lower-tier demand density with a fit-for-purpose box.

For company-operated stores, we assume continued infill in top-tier city core trade areas, with most incremental units coming from franchised lower-tier openings. This mix supports both reach and capital efficiency as the network deepens.

Specifically, we assume KFC reaches 19,527 stores by 2030, with franchise penetration rising from ~15% to ~25%. With Wallace already near 20k, this is not an aggressive scenario in absolute terms.

On the key swing factor—SSS—we assume a modest recovery. Beyond traffic offsets to lower tickets, the biggest incremental driver is the 'store-in-store' KCOFFEE model: leveraging KFC’s existing locations, footfall, and supply chain to sell coffee with minimal incremental rent or CAC. That lifts sales per sqm and supports SSS.

2) Pizza Hut: a later-cycle lower-tier story with bigger optionality

Pizza Hut had 4,168 stores at end-2025, with a slower franchise ramp than KFC. Franchise share of the base was only ~7%, and guidance for franchise share of net adds is 20%–30%, below KFC’s 40%–50% pace.

The key to lower-tier expansion is the WOW format—wider price bands and a more mass-market proposition aimed at white-space lower-tier cities. Essentially, Pizza Hut is evolving from a Tier-1/2 casual dining brand into a mass pizza brand that can penetrate lower tiers.

Because it is early with a low base, once WOW proves out in lower tiers, unit growth could flex faster than KFC. That said, greater optionality does not mean higher certainty—replicability of the WOW model and reshaping mass perception remain to be validated. Hence expansion visibility is lower than KFC’s already-proven lower-tier/franchise path.

'Others' include standalone KCOFFEE, Lavazza, Taco Bell, Little Sheep, and Huang Ji Huang. Each is small today with limited revenue contribution; individually they are not needle movers. But sharing the group’s supply chain and digital backbone keeps test-and-learn costs low—if any one scales, it becomes a near 'free' second growth curve.

Based on these, our 5-year revenue and profit CAGRs are as follows. We assume steady footprint expansion, modest SSS lift, and incremental margin from mix and efficiency.

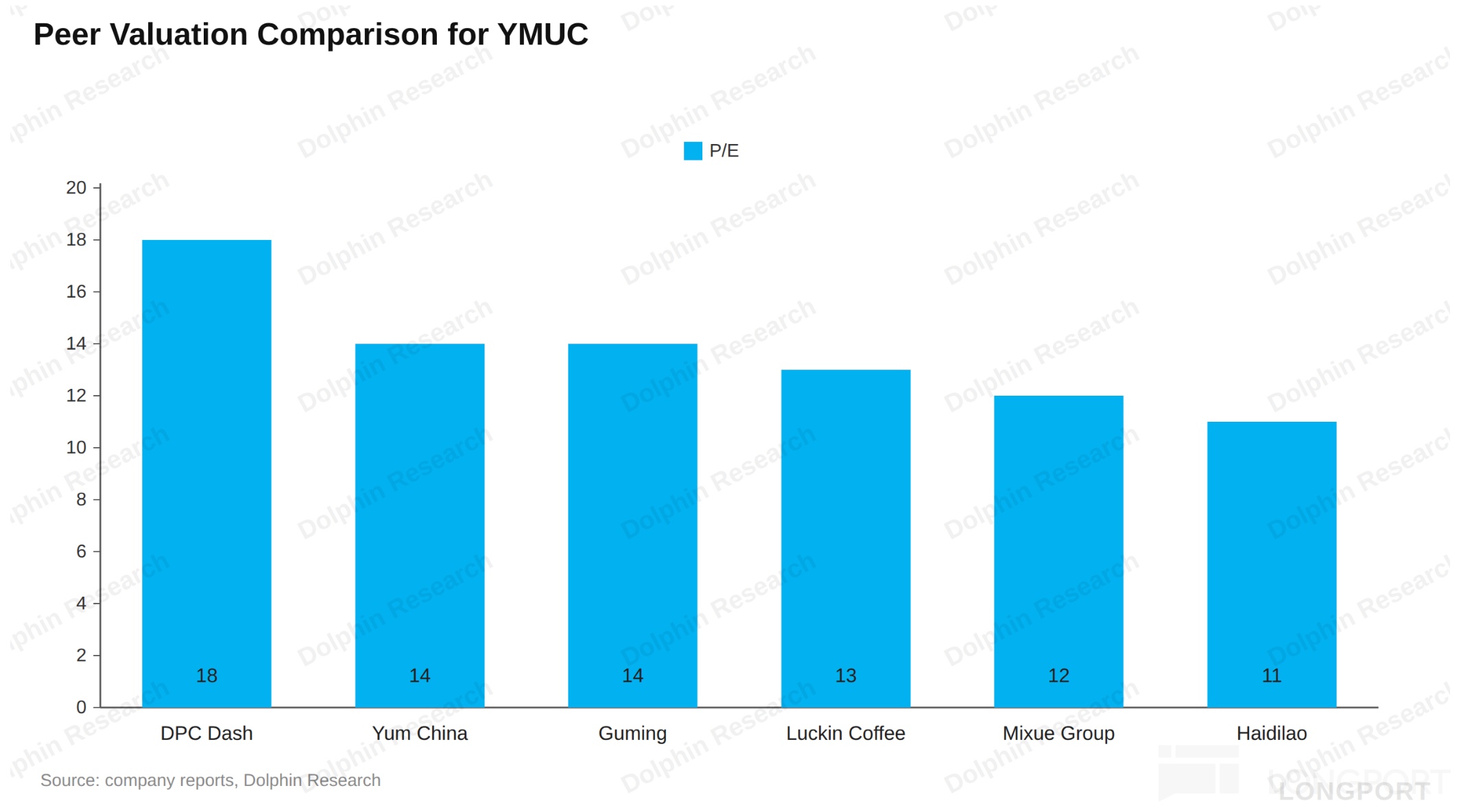

On relative valuation, Yum China trades at ~14x 2026E, versus an ~8% EPS CAGR—roughly neutral. Compared with peers that have already de-rated, the stock is not cheap.

In our view, this neither-cheap-nor-expensive stance largely reflects a macro discount on 'soft China consumption' rather than company-specific issues. That implies upside in the near term is unlikely from multiple expansion, and more likely from sustained profit delivery and per-share EPS accretion via buybacks.

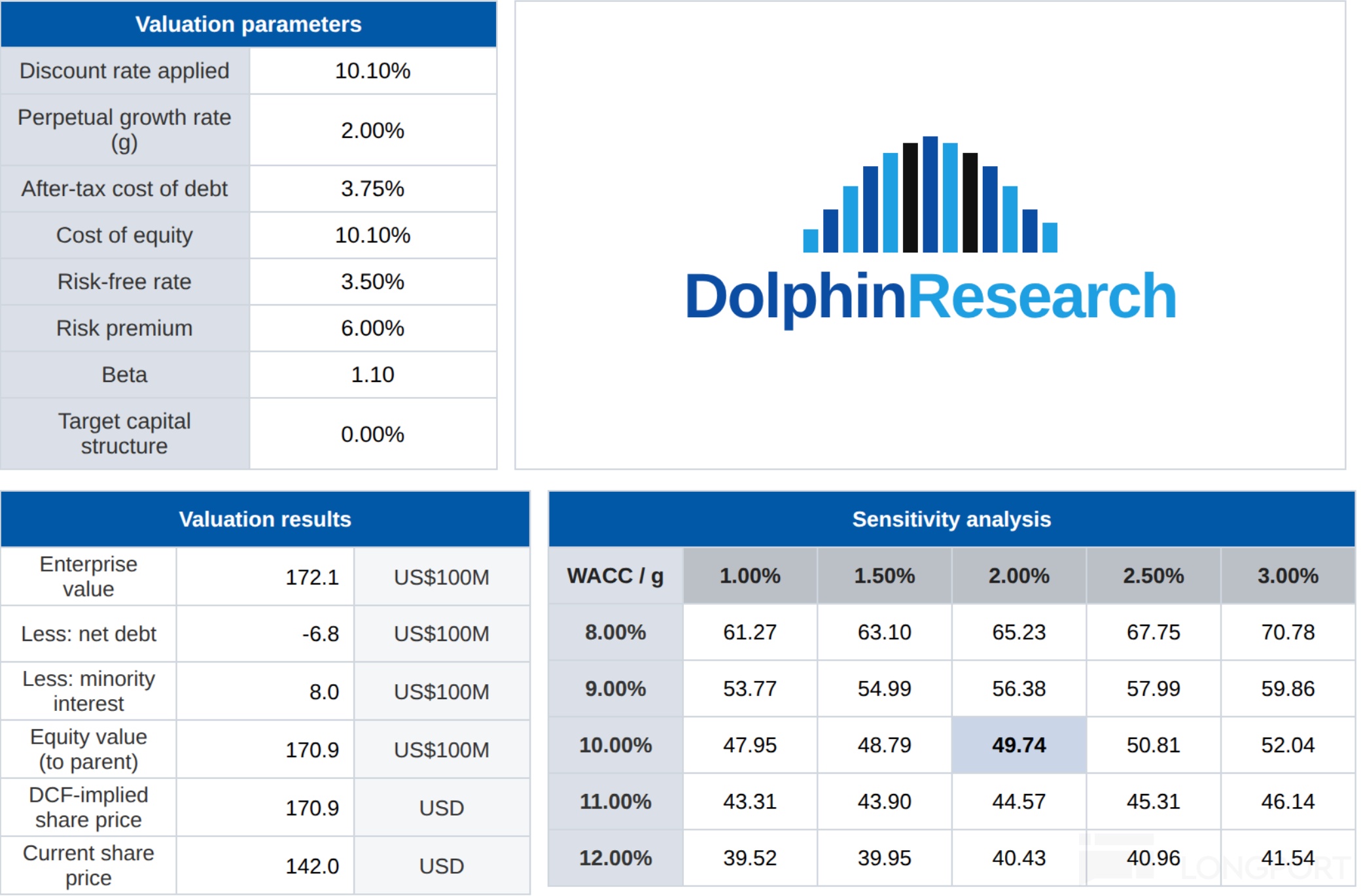

On DCF, using WACC of 10.1% and a 2% terminal growth rate—deliberately conservative to reflect China uncertainty—we derive $49 per share, implying ~22% upside. Put differently, upside depends heavily on when China consumption expectations improve: fundamentals (profit + buybacks) offer ~20% 'floor returns', while valuation repair (lower WACC) is a larger but wait-for-it call option.

Bridging relative and absolute, our take is that Yum China is a 'bond-like + growth option' setup at a fair sticker. About 14–15x forward P/E and ~9%–10% total shareholder return (c.$1.5bn to be returned in 2026; near full FCF return from 2027) provide the bond-like floor, while lower-tier expansion, faster franchising, and coffee scale-up are near-free growth options.

IV. Summary

As with Walmart, Gu Ming, and 'MingMing is Busy' in our prior work, Yum China’s essence is a self-reinforcing low-cost ecosystem. Its carrier happens to be fried chicken and pizza rather than paper towels or milk tea, but the flywheel is similar.

Building this system takes decades—supply chain city by city, digital iteration year by year, and brand equity across generations. Yum China may not beat McDonald’s or Domino’s on any single logistics, storage, or processing link, but in tying them together into a networked system, it has few rivals.

From a portfolio perspective, for low-risk, cashflow-focused investors, Yum China offers bond-like characteristics: combined dividends and buybacks drive an 8%–10% TSR midpoint, with scope for further FCF returns over time. At the same time, lower-tier footprint expansion and Pizza Hut margin repair provide long-term growth optionality. This makes it a high-quality core holding in China consumption—stable cash flows with a free recovery option.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.