Paradis Stock Report: Harmonic Drive Systems (6324)

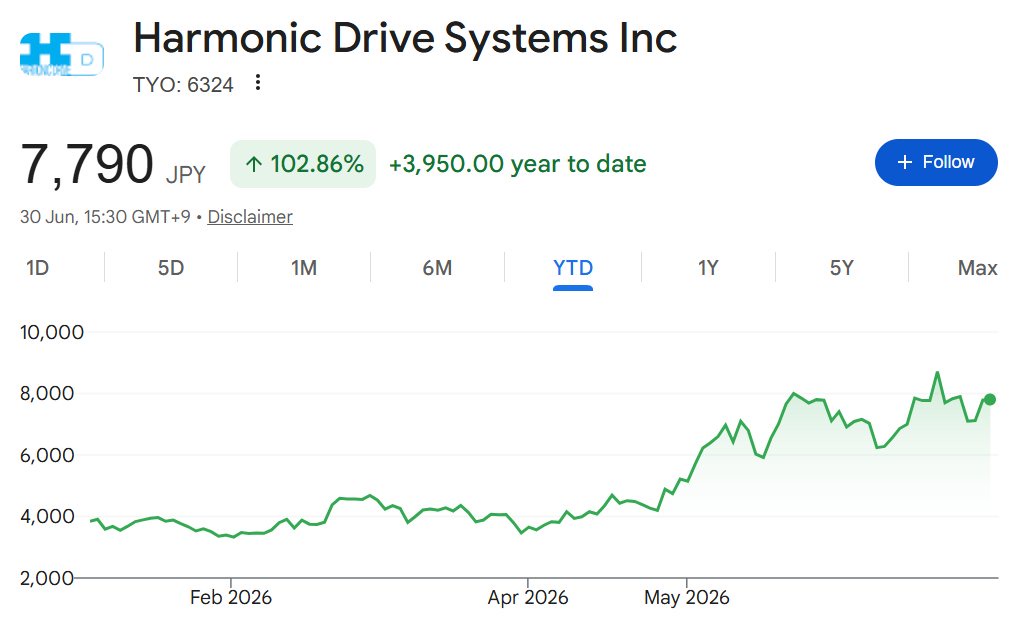

For upstream humanoid exposure. (Disclosure: I hold a position).I have mentioned HDS a few times in my humanoids article and in various comments.-> Here's my technical research article that I wrote a few months ago for a few buy-side institutions.(With updated financials and amended/shortened for my anonymity and integrity to paying firms. Some customer mapping etc. may need updating also):Report:Every humanoid demo you have seen - Figure pouring a coffee, Optimus folding a shirt, a Unitree robot doing a backflip - leans on a very specific component almost nobody outside the motion control world can name. Before the model decides to move the hand and before the motor delivers torque, something has to convert a low-torque rotor into the precise, high-torque rotation a wrist or finger actually needs. That something is a precision reducer. And in the highest precision joints, the reducer of record for 40 years has been the strain-wave gear.Invented, branded, and still dominated at the premium end by one company: Harmonic Drive Systems (6324).First, a piece of housekeeping:- The entity that matters is the Japanese parent, listed on the Tokyo Prime Market. - It owns 100% of Harmonic Drive SE in Germany (the former Harmonic Drive AG) and a majority of Harmonic Drive LLC in Beverly, Massachusetts. - It is not a Nidec company. Nidec-Shimpo is a separate competitor, and Harmonic Drive actually sold its policy stake in fellow reducer-maker Nabtesco during the year to March 2025. Their flagship product is a simple three-part assembly: 1. a wave generator2. a thin walled steel cup called a flexspline3. a rigid circular spline[I've removed some technical stuff cos it can get boring quickly]Harmonic Drive sells this as component sets (the CSF, CSG, SHF and SHG families), as integrated AC servo actuators bundling a frameless motor, the gear and an encoder (the SHA and FHA lines), and as lower-ratio planetary units for less demanding joints.In a six-axis industrial arm or a cobot, this is the gear in the wrist, forearm and elbow. The heavy base and shoulder axes belong to RV cycloidal reducers, where Nabtesco holds something like 60% of the world market; harmonic and cycloidal are complements far more than competitors. The same strain-wave gear shows up in semiconductor wafer-handling and lithography stages, in surgical robots. In aerospace, Harmonic Drive units have flown on NASA's Curiosity and Perseverance rovers. The customer map broadly reads like a census of the automation industry: FANUC, Yaskawa, ABB, KUKA, Kawasaki, Universal Robots, plus a long tail of semiconductor equipment and medical device OEMs.[I've removed some speculative numbers and customers]For analysts considering the bull-case optionality: The moat is in the process, and specifically in one component: the flexspline. That thin steel cup is elastically deformed millions of times over its life, and it is the part that fails. Patent and engineering literature is blunt about this...the flexspline fatigues, and the cheap routes to making one wreck its cycle life. Bulk-metallic-glass flexsplines crack at far lower cycle counts because their fracture toughness is a fraction of forged steel's. 3D printed metal flexsplines carry porosity and surface roughness defects that, in the words of one patent filing, dramatically reduce their lifetimes. [Patent/IP stuff is boring, so I have removed]Harmonic Drive's proprietary tooth profiles (the "IH" generation and its successors) spread load across many teeth meshing at once, which is how you buy fatigue margin without buying weight.It is an empirical feedback loop: decades of field-return data from satellites, wafer handlers and arms running under extreme duty, fed back into design margins.Layered on top is qualification lock-in:In aerospace, semiconductor and medical applications, the reducer is designed into a system that then takes 12 to 24 months to re-certify if you swap it. Once a Harmonic Drive part is flight or fab qualified, the switching cost is the re-qualification programme. That locks revenue for years, and in aerospace it is close to permanent.Now moving onto the core demand vector: HumanoidsThe narrative premium is humanoids and maths can be seductive.A humanoid uses somewhere between 20 and 40 reducers across its joints, a mix of harmonic and planetary. At a Harmonic-grade ASP frequently cited near $800 a unit, 100,000 humanoids is on the order of $1.6B of harmonic-reducer demand which is a 5-10x TAM expansion against today's industrial base. From supply chain mapping, unit numbers are finally inflecting off zero: Harmonic Drive has started to book real, if small, humanoid orders. Roughly ¥1.3B in a single quarter, around ¥2.5B guided for the year to March 2026, with management telling analysts the following year could double or triple that, and the count of potential humanoid customers climbing past 15, concentrated in Japan and North America. In my view, this is the closest thing the listed world has to a pure play on the actuator content of a humanoid joint.For clients, there are naturally some coverage concerns however:Coverage is thin and almost entirely Japan-desk - Goldman, Morgan Stanley MUFG, Jefferies, Macquarie, Citi, Nomura, Mizuho. For a generalist global fund the name is genuinely hard to own: 1. A Tokyo Prime listing2. Japanese-GAAP disclosure3. No quarterly order detailAnd a business whose irreplaceability lives in segments (semiconductor, aerospace, premium humanoid) that headline market share data (which shows Harmonic Drive losing share) actively obscures.However, in my view, the cyclical recovery is underway:This is not a story stock with no business. For the year to March 2026, Net sales rose 7.0% to ¥59.6B. It is important to factor in the quarterly cadence too:Revenue climbed ¥13.5B, ¥14.3B, ¥14.3B, ¥17.4B through the year, and EPS went from minus ¥0.40 in the first quarter to ¥8.86 in the fourth as factory utilisation recovered and the CoS ratio fell.This is textbook fixed-cost absorption, with incremental margins reportedly above 50%. Guidance for the year to March 2027 is for sales of ¥68.0B, up 14.2%, operating profit up 141% to ¥6.2B, and net income up 180% to ¥4.5B. Orders are corroborating: - full-year intake of ¥61.6B was up 16.2%, with North American reduction-gear orders up 31.3% and Japan up 26.9%. The balance sheet removes any solvency question from the discussion:- Roughly 72% equity ratio, net cash, operating cash flow of ¥6.4B, and enough firepower to fund a 33% expansion of the US Beverly plant by December 2026 without touching shareholders. In May the company set a fresh five-year plan: - ¥100B-plus in sales and a >15% operating margin by the year to March 2031. On review, this is a fortress balance sheet attached to a genuine moat in a market that is inflecting.Risks:China.Harmonic Drive's global unit share has fallen from north of 70% historically to an estimated 20% today. In China (the largest robot market) domestic suppliers now lead outright: Leaderdrive and Zhejiang Laifual held roughly 27.5% and 21.4% of the country's robotic harmonic-reducer market by 2025 shipments. Leaderdrive grew revenue 47% to 570.7M yuan in 2025 and more than doubled net profit, and has already fulfilled humanoid R&D orders for Tesla and Figure. The pricing gap should be emphasised at this stage: Chinese Tier-1 units land at circa 40-60% of Harmonic Drive's price, and that gap is widening.Laifual's average reducer ASP fell about 30% in two years, which its own IPO prospectus framed as a deliberate share grab. Independent stress-testing puts the best Chinese parts at 70-85% of the Japanese benchmark on torque density and lifespan, but at backlash parity. Based on discussions with [famous robotics company], for most of the joints in most of the robots, "good enough at half the price" is the whole ballgame. Management's own long-term framing has overall strain-wave share declining toward 6% in the long run.[Some analysis on valuations and financial modelling, removed cos it's boring]Further, the largest humanoid programmes may design around Harmonic Drive:Tesla designs its actuators in-house and multi-sources the reducers, including from Chinese suppliers, with teardown chatter pointing to a meaningful and rising Chinese share of Optimus content at 30-40% lower cost. Harmonic Drive is, at best, one of several reducer sources for the biggest program and not the sole-source chokepoint the current valuation and our forecasting implies.[More boring bits on depreciation, yen strength, cyclicality, sales geographies]To conclude:1. Harmonic Drive owns a qualification locked chokepoint in premium precision reducers.2. Sits on a strong balance sheet.3. Is one year into a credible cyclical recovery.4. Holds the cleanest listed exposure to humanoid actuator content that exists. If a large Western humanoid program (Figure, Apptronik, even Tesla) confirms primary source Harmonic Drive content shipping at premium prices and scale, the structural story has potential to re-rate.

本文版权归属原作者/机构所有。

当前内容仅代表作者观点,与本平台立场无关。内容仅供投资者参考,亦不构成任何投资建议。如对本平台提供的内容服务有任何疑问或建议,请联系我们。

发表你的评论

暂无评论