Index Rebalancing: How It Affects Your ETF Holdings

Index rebalancing quietly reshapes your ETF holdings multiple times a year. Discover how the process works and what it means for your portfolio.

TL;DR: Index rebalancing is the process by which the stocks inside an index — and the ETFs that track it — are periodically reviewed and adjusted. It happens automatically, but it can cause short-term price volatility and affect your ETF's holdings. Understanding how it works helps you make more informed decisions as a passive investor.

If you hold exchange-traded funds (ETFs), you have probably noticed that their holdings occasionally change — even when you have not made a single trade. A stock you once saw in your ETF might quietly disappear, replaced by a new one. This is the result of index rebalancing, a behind-the-scenes process that shapes what is inside your ETF and how it performs.

Index rebalancing is a structured, rules-based process that occurs multiple times a year and has measurable consequences for prices, portfolio composition, and even tax liabilities. This guide explains how it works, when it happens, and what it means for your holdings across Singapore, US, and Hong Kong markets.

To build a solid foundation in investment fundamentals, understanding what drives change inside your ETF is a natural first step.

What Is Index Rebalancing?

An index is not a static list of securities. It is a set of rules — criteria for which companies qualify, how much weight they carry, and when they are reviewed. Index rebalancing is the periodic process of updating an index's composition to reflect those rules as market conditions change.

When companies grow, shrink, merge, or go public, the index may no longer accurately represent the market segment it was designed to track. Rebalancing corrects this by adding qualifying companies, removing those that no longer meet the criteria, and adjusting existing weightings. Because ETFs mirror specific indices, the ETF provider must buy shares of newly added companies and sell those being removed to keep the fund aligned.

Why Indices Need Regular Updates

Markets evolve constantly. A company that qualified for inclusion in a large-cap index last year may have seen its market capitalisation fall below the threshold, while another may have grown rapidly enough to join. Without periodic updates, an index would drift from its stated objective. Index providers — such as S&P Dow Jones Indices, FTSE Russell, and MSCI — each have their own methodologies, but share the same goal: keeping the index relevant and representative over time.

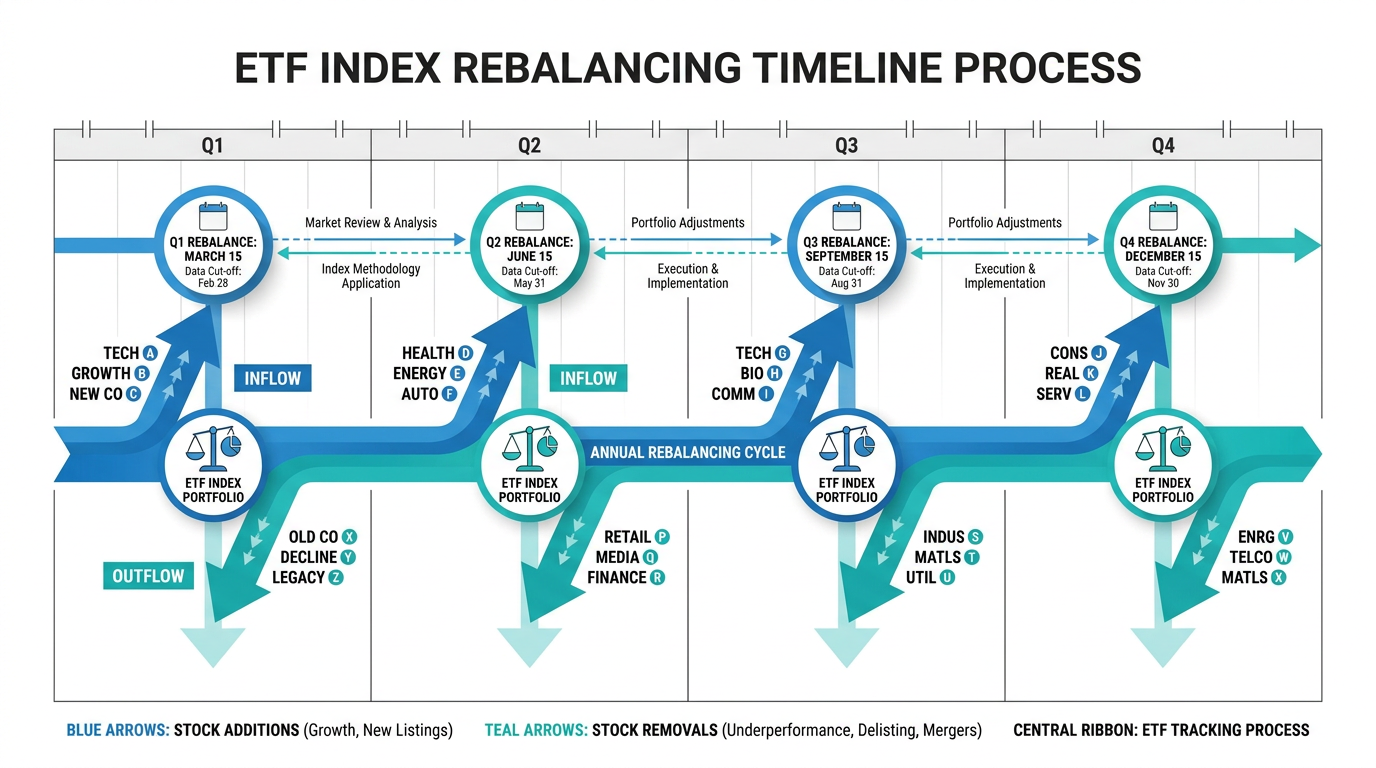

How Index Rebalancing Works

The rebalancing process follows a predictable sequence, though the exact timeline varies by index provider.

Step 1: Review and analysis. The index provider analyses current holdings against eligibility criteria. This includes market capitalisation thresholds, liquidity requirements, financial performance metrics, and sector classification.

Step 2: Announcement. Proposed changes are published in advance — typically five trading days ahead for the S&P 500, and two to three weeks ahead for indices managed by MSCI, according to CME Group (source).

Step 3: ETF provider preparation. ETF managers calculate the number of shares they need to buy or sell to match the new index composition, taking into account transaction costs, liquidity, and cash flows.

Step 4: Execution. Trades are executed on the effective rebalancing date, bringing the ETF's holdings in line with the updated index.

How Often Does Index Rebalancing Happen?

The frequency depends on the index. Most major equity indices rebalance on a quarterly or semi-annual basis. The S&P 500, for example, rebalances quarterly in March, June, September, and December. FTSE Russell announced a shift from annual to semi-annual rebalancing starting in 2026, taking place in June and November.

Sector-specific and factor-based ETFs may rebalance more frequently, as their constituent criteria — such as valuation ratios or momentum scores — can change more rapidly than broad market membership rules.

Note: Leveraged and inverse ETFs are a special case. These funds rebalance their exposure to the underlying benchmark every single day to maintain their stated multiple. This daily rebalancing makes them structurally unsuitable for long-term passive holding, as the compounding effect over time can cause significant divergence from the intended multiple.

Types of ETFs and How They Rebalance

Not all ETFs rebalance in the same way. The rebalancing method is directly tied to the type of index the fund tracks.

Market Capitalisation-Weighted ETFs

The most common type, these funds weight each holding according to market capitalisation. After rebalancing, weights are adjusted to reflect updated data. Trading activity is relatively modest unless companies are added or removed from the index.

Equal-Weight ETFs

These ETFs assign the same percentage to every constituent regardless of size. Because prices move at different rates, allocations drift between rebalancing dates. When rebalancing occurs, the fund sells positions that have grown and buys those that have lagged — a systematic buy-low, sell-high mechanism. This leads to higher portfolio turnover and potentially greater transaction costs.

Factor and Thematic ETFs

Factor-based funds target specific investment characteristics such as value, momentum, or quality. They rebalance to ensure their holdings continue to score well on the relevant metrics. Dividend-focused ETFs similarly rebalance to maintain their yield characteristics as dividends and company financials change over time.

What Index Rebalancing Means for Your Portfolio

Index rebalancing has several practical consequences for ETF holders that are worth understanding.

Short-Term Price Movements

When a stock is added to a widely tracked index, ETFs and index funds tracking that index must purchase shares of that company. Because trillions of dollars are benchmarked to major indices, this mechanical buying activity can push the stock's price up in the days before the rebalancing date — a phenomenon often called the "index inclusion effect."

The reverse is also true: a company removed from an index may experience downward price pressure as funds sell their holdings. This movement is driven by mechanical flows, not by changes in business fundamentals.

Note: Past observations of the index inclusion effect describe historical patterns and do not guarantee similar outcomes in future rebalancing events.

Tracking Error

Tracking error is the difference between an ETF's returns and those of the index it follows. Rebalancing activity can contribute to tracking error, particularly for ETFs that are slow to execute their required trades. Transaction costs, market impact from large trades, and timing differences between announcement and execution all play a role.

Capital Gains Distributions

Selling securities during rebalancing can generate realised gains within the fund. In some jurisdictions, these gains are distributed to investors, creating a taxable event even if you did not sell your ETF shares. This is more common in mutual funds but can occur in ETFs as well, particularly those with high portfolio turnover.

Tip: Singapore investors generally do not pay capital gains tax on investment income. However, if you hold ETFs that invest in US equities, you may be subject to US withholding tax on dividends. Always consult a qualified tax adviser for guidance specific to your situation.

Explore the full range of investment products available on the Longbridge platform, including ETFs across Singapore, US, and Hong Kong markets.

Portfolio Drift and the Investor's Role

Index rebalancing handles the internal alignment of your ETF, but it does not manage your personal portfolio's overall balance. Over time, as different asset classes perform differently, your allocation between equities and bonds — or between geographies — will shift. This is called portfolio drift, and addressing it is your responsibility.

Calendar-Based Rebalancing

This approach involves reviewing and rebalancing on a fixed schedule — annually or semi-annually. It removes emotion from the process and ensures discipline regardless of market conditions. Rebalancing less frequently generally incurs lower transaction costs than rebalancing very often.

Threshold-Based Rebalancing

Alternatively, you can rebalance only when your equity allocation drifts more than a set amount — for example, five percentage points — from your target. This responds to actual market movements rather than the calendar and may involve fewer trades in stable markets, though it requires more regular monitoring.

Both approaches are valid. The key is choosing one and applying it consistently.

How to Stay Informed as an ETF Investor

Rebalancing events are announced in advance. Index providers publish their schedules and criteria publicly, and major changes are widely reported in financial news. You can track market movements and ETF performance using the Longbridge market data tools, which provide real-time pricing and portfolio insights across Singapore, US, and Hong Kong exchanges.

Tip: Understanding rebalancing announcements can help explain short-term price movements, but most ETF investors are better served by focusing on long-term asset allocation rather than attempting to trade around rebalancing events.

Frequently Asked Questions

Does index rebalancing happen automatically in ETFs?

Yes. ETF providers are responsible for executing all rebalancing trades within the fund. As a unit holder, you do not need to take any action. The fund adjusts its holdings to match the updated index, and the process is reflected in the ETF's net asset value over time.

Does index rebalancing affect ETF performance?

It can, in the short term. Rebalancing generates transaction costs, and price movements around rebalancing dates can cause temporary divergence from the index. Over the long term, these effects are generally small for broad market ETFs, though they may be more pronounced for equal-weight or factor-based funds with higher portfolio turnover.

Should I rebalance my own portfolio when the index rebalances?

These are two separate activities. The ETF's internal rebalancing is handled by the fund manager. Your personal portfolio rebalancing — adjusting the mix between different asset classes or ETFs — is a decision you make based on your own target allocation, investment horizon, and risk tolerance.

How do I find out when my ETF's index is due to rebalance?

Index providers publish their schedules publicly. The S&P 500 rebalances quarterly in March, June, September, and December. You can also review your ETF's factsheet or prospectus, which outlines the rebalancing schedule and methodology of the underlying index.

Conclusion

Index rebalancing is a significant and often overlooked process in passive investing. It ensures the ETF you hold continues to represent the market segment it was designed to track, but it also brings real-world consequences: short-term price movements, potential tracking error, and possible taxable events.

For long-term ETF investors, the practical takeaway is clear. Trust that the ETF provider handles internal rebalancing automatically, stay aware of major index changes, and periodically review your own portfolio to address drift between asset classes.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.