Singapore ETF Taxation: What Every Investor Needs to Know

Singapore imposes no capital gains tax on ETFs, but US withholding tax and estate tax can silently erode returns. Here's what investors need to know.

TL;DR: Singapore does not impose capital gains tax or domestic dividend tax on Exchange-Traded Fund (ETF) investments, which makes its tax framework relatively straightforward for investors. However, investing in US-listed ETFs triggers a 30% US withholding tax on dividends, and non-residents face US estate tax exposure — two costs that can be mitigated by choosing Ireland-domiciled ETFs or using the Supplementary Retirement Scheme (SRS).

For many Singapore investors, Exchange-Traded Funds (ETFs) have become a cornerstone of long-term portfolio building, offering broad market exposure and relatively low expense ratios. Yet one dimension often overlooked when evaluating total costs is Singapore ETF taxation — specifically, how different fund structures and domiciles affect the after-tax returns you actually receive.

Singapore's tax framework is broadly favourable: no capital gains tax, no domestic withholding tax on dividends from locally listed funds. The picture becomes more nuanced once you invest in US-listed ETFs or consider estate planning. This guide breaks down the key tax considerations clearly, so you can make more informed choices when building your portfolio.

Singapore's Tax Framework for Individual Investors

Singapore operates a relatively straightforward tax environment for retail investors in the Asia-Pacific region. Understanding the baseline rules helps you identify where real costs arise.

No Capital Gains Tax

Singapore does not impose capital gains tax. Profits from selling an ETF are generally not taxed. However, the Inland Revenue Authority of Singapore (IRAS) applies a "badges of trade" framework to distinguish investors from traders, assessing factors such as transaction frequency, holding period, and whether there is an organised trading structure.

If IRAS determines your activity constitutes a trade, profits may be taxed as trading income at the prevailing personal income tax rate (0–24%, progressive). For most retail investors holding ETFs over the medium to long term, this classification risk is minimal.

Dividends From Singapore-Listed ETFs

Dividends received from Singapore-listed ETFs and stocks are not subject to withholding tax at the investor level. Once a Singapore-domiciled fund or company pays corporate tax on its profits, dividends distributed to shareholders — whether residents or foreign investors — are treated as final. No further tax is deducted at the investor's end.

Note: Real Estate Investment Trust (REIT) ETFs have specific tax treatment under IRAS guidelines. For individual investors, distributions from REIT ETFs are generally exempt from income tax, unless those distributions are received through a Singapore partnership or as part of a business, profession, or trade. (Source: IRAS e-Tax Guide on REIT ETFs)

The Hidden Cost: US Withholding Tax on ETF Dividends

This is where Singapore ETF taxation becomes more complex — and more consequential for your returns.

How the 30% US Withholding Tax Works

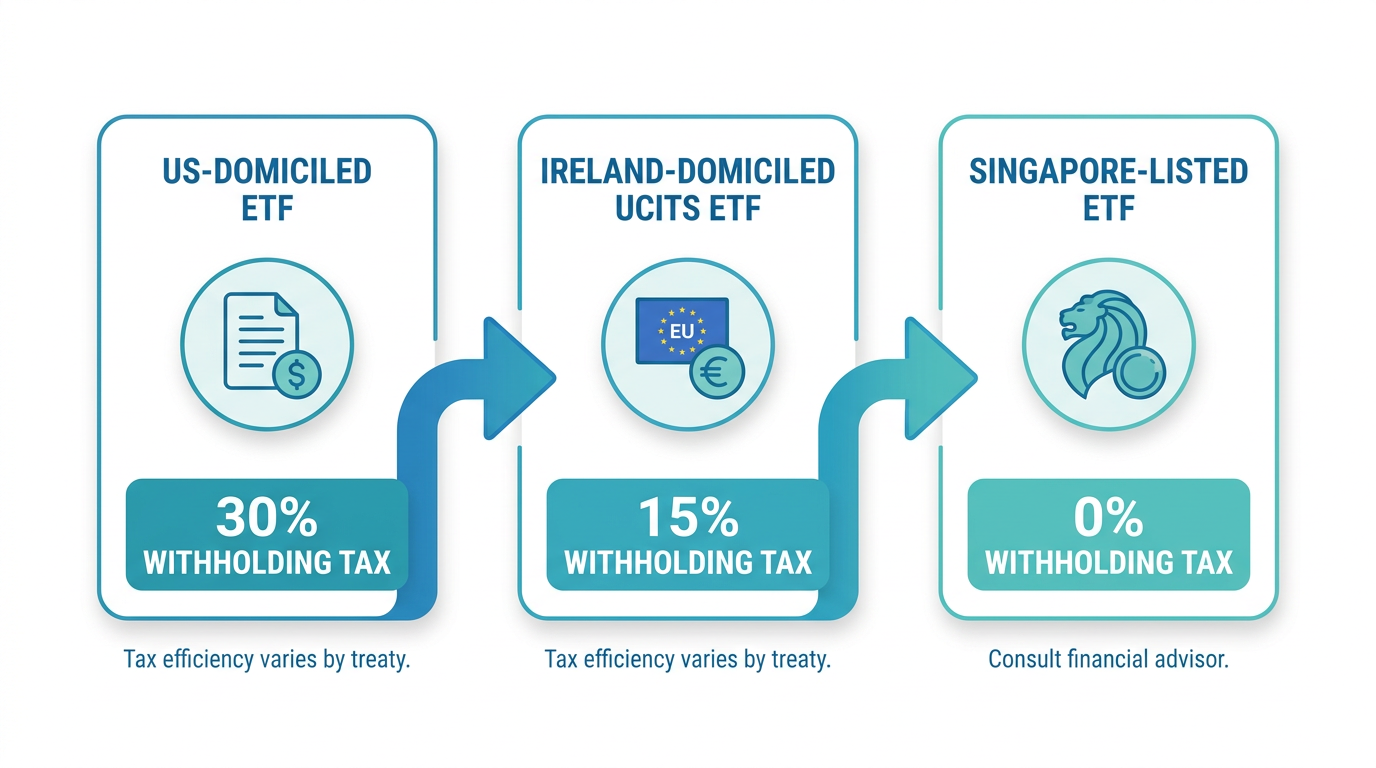

Singapore does not have a tax treaty with the United States. As a result, Singapore investors holding US-listed ETFs — such as funds tracking the S&P 500 or broad global indices — are subject to a 30% US withholding tax on all dividend distributions. This tax is applied at source before dividends reach your brokerage account; you do not need to file anything separately, but you also cannot reclaim it.

To illustrate the impact (illustrative example only): if a US-listed ETF pays USD 100 in dividends, you would receive USD 70. Over time, and particularly for funds with meaningful dividend yields, this drag can compound on your overall returns.

Ireland-Domiciled UCITS ETFs: A Different Withholding Tax Treatment

Undertakings for Collective Investment in Transferable Securities (UCITS) are a regulatory framework established by the European Union. Ireland-domiciled UCITS ETFs benefit from a favourable tax treaty between the US and Ireland, which reduces the withholding tax applied at the fund level from 30% to 15% on US dividends.

Crucially, Ireland does not impose withholding tax on dividends paid by Irish-domiciled UCITS funds to non-resident investors. This means Singapore investors in Ireland-domiciled ETFs benefit from the lower 15% rate rather than the full 30%.

For synthetic ETFs — where the fund achieves index exposure through derivative contracts rather than holding the underlying shares directly — the withholding tax impact can be reduced further, potentially to zero, depending on the structure.

Summary of Withholding Tax by ETF Type

| ETF Type | Dividend Withholding Tax (Singapore Investors) |

|---|---|

| US-domiciled ETFs (e.g. tracking S&P 500, listed in New York) | 30% |

| Physical Ireland-domiciled UCITS ETFs | 15% |

| Synthetic Ireland-domiciled UCITS ETFs | 0% (structure-dependent) |

| Singapore-listed ETFs | 0% |

The reduced rate for Ireland-domiciled funds reflects the income tax treaty between the United States and Ireland. Rates are indicative and depend on fund structure and domicile; investors should confirm the current treatment with the fund issuer's documentation and the relevant tax authority.

US Estate Tax: A Risk Often Overlooked

Beyond dividend withholding tax, there is a second structural risk for Singapore investors holding US-situs assets: the US federal estate tax.

What Is US Estate Tax?

The US imposes estate tax on assets considered "US-situated" (or US-situs) at the time of a non-resident's death. According to the US Internal Revenue Service (IRS), non-resident, non-citizen estates generally receive an estate tax exemption of USD 60,000 — substantially lower than the exemption available to US citizens and residents, which stood at USD 13.99 million for 2025.

For US-domiciled ETFs, the fund units are classified as US-situs assets. If the total value of your US-situs assets exceeds the USD 60,000 threshold at the time of death, the excess may be subject to US estate tax at marginal rates of up to 40%. (Source: US Internal Revenue Service guidance on estates of non-residents not citizens of the US.) This is a material consideration for Singapore investors who have built meaningful ETF portfolios over time.

How Ireland-Domiciled ETFs Reduce This Risk

Ireland-domiciled UCITS ETFs are not classified as US-situs assets, even if the fund holds US shares as its underlying investments. Because the fund itself is incorporated in Ireland, it falls outside the scope of US estate tax for non-resident investors. This structural distinction — where a fund is legally domiciled versus what it invests in — is an important factor for Singapore investors thinking about estate planning alongside investment returns.

Using the Supplementary Retirement Scheme to Invest in ETFs

The Supplementary Retirement Scheme (SRS) is a voluntary, government-backed scheme that offers a meaningful tax advantage for retirement investing.

How SRS Tax Benefits Work

SRS contributions are eligible for income tax relief, subject to the overall personal income tax relief cap of SGD 80,000. Singapore Citizens and Permanent Residents may contribute up to SGD 15,300 per year; foreigners up to SGD 35,700. (Source: IRAS SRS Contributions)

Investment returns within SRS are not taxed during the accumulation phase. At retirement withdrawal, only 50% of the amount withdrawn is subject to income tax.

Investing SRS Funds in ETFs

SRS funds can be invested in a range of eligible products, including ETFs listed on the Singapore Exchange (SGX). Doing so allows you to grow your retirement savings while benefiting from ETF diversification, and defer tax until withdrawal. For investors who are keen to explore this strategy, the Longbridge Academy guide on SRS investment options provides a useful starting point.

Tip: SRS contributions must be made by 31 December of the relevant year to qualify for tax relief in the following Year of Assessment. Plan your contributions early to maximise the benefit.

Three Layers of Taxation to Understand

When evaluating the true cost of an ETF, consider taxation at three levels: the fund corporation level (some jurisdictions charge corporate tax on fund income; Ireland does not, adding to UCITS efficiency), the distribution level (where withholding taxes apply based on domicile), and the investor level (where Singapore individuals generally owe no additional tax on gains or dividends). Two ETFs tracking the same index can produce meaningfully different net returns for a Singapore investor simply because of these structural differences.

Practical Considerations When Choosing ETFs in Singapore

Singapore investors can access a wide range of ETFs and other investment products across multiple markets. When evaluating tax efficiency alongside other factors, consider the following:

ETF domicile: For international equity exposure with US holdings, Ireland-domiciled UCITS ETFs reduce withholding tax drag and eliminate US estate tax exposure.

Accumulating vs. distributing share classes: Accumulating ETFs reinvest dividends at the fund level, reducing the immediate withholding tax impact compared to distributing share classes.

SRS eligibility: If you contribute to SRS, prioritise ETFs eligible for SRS investment to maximise tax deferral.

Records and holding periods: Document your investment rationale. Occasional ETF investing is unlikely to trigger IRAS's trader classification, but clear records are prudent.

Estate planning: If your international holdings are significant, seek professional advice on the implications of US-situs assets.

For real-time portfolio tracking across Singapore, US, and Hong Kong markets, explore the Longbridge market data services platform.

Frequently Asked Questions

Do Singapore investors pay tax on ETF profits?

Singapore does not impose capital gains tax, so profits from selling ETFs are generally not taxable for retail investors. IRAS may classify very frequent traders as engaged in a trade or business, in which case profits could be treated as taxable income. For most long-term, buy-and-hold investors, this does not apply.

What is the withholding tax on US ETFs for Singapore investors?

Singapore investors holding US-listed ETFs are subject to a 30% US withholding tax on dividend distributions, as Singapore does not have a tax treaty with the United States. This tax is deducted at source before dividends reach your account.

Are Ireland-domiciled ETFs more tax-efficient for Singapore investors?

Ireland-domiciled UCITS ETFs reduce the US dividend withholding tax from 30% to 15% and are not subject to US estate tax — structural advantages, not a performance guarantee. Whether they suit you depends on your individual objectives, risk tolerance, and circumstances.

Can I invest my SRS savings in ETFs?

Yes. SRS funds can be invested in eligible ETFs listed on the Singapore Exchange. Investment returns within the SRS account accumulate tax-free, and only 50% of withdrawals at retirement are subject to income tax.

Are REIT ETF distributions taxable in Singapore?

For individual investors, distributions from Singapore-listed REIT ETFs are generally exempt from income tax, unless received through a partnership or as part of a trade or business. Corporate and non-resident non-individual investors may be treated differently. Consult IRAS guidance or a qualified tax professional for your specific situation.

What is US estate tax and does it affect Singapore ETF investors?

The US imposes estate tax on US-situs assets held by non-residents at death, with only a USD 60,000 exemption for non-US persons. US-domiciled ETF units are US-situs assets. Ireland-domiciled ETFs fall outside this scope, as they are not classified as US-situs assets.

Conclusion

Singapore's tax environment is broadly favourable for ETF investors. No capital gains tax and no domestic dividend withholding tax mean most retail investors retain more of their returns than in many other jurisdictions. However, the 30% US withholding tax on US-listed ETF dividends and US estate tax exposure are real costs requiring informed choices.

Considering Ireland-domiciled UCITS ETFs for international exposure, using the SRS for retirement savings, and maintaining clarity on your investor status are practical steps worth exploring. The right approach depends on your individual objectives, risk tolerance, and circumstances. Consult a licensed financial adviser or tax professional for personalised guidance.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.