Mutual Fund Fees: Hidden Costs Singapore Investors Pay

Singapore investors often overlook hidden mutual fund fees like platform charges and trailer fees. Learn how these costs reduce returns and strategies to minimize them.

TL;DR: Singapore investors often overlook mutual fund fees that may not be immediately apparent like platform charges, trailer fees, and switching costs that can influence long-term outcomes and returns. Understanding the difference between management fees and Total Expense Ratio (TER), plus comparing fee structures across platforms, can help improve cost efficiency over time.

Investing in mutual funds seems straightforward until you examine the fee structure. While the potential returns draw investors in, the costs that may affect overall returns often remain hidden in fine print. For Singapore investors, understanding mutual fund fees is not just about reading a prospectus—it is about recognizing how seemingly small percentages compound into substantial amounts over time.

According to the Monetary Authority of Singapore (MAS), investors should be aware of all charges before committing funds. Yet many Singaporeans discover the true cost of their investments only after years of diminished returns. This guide breaks down the visible and hidden fees that affect your mutual fund investments, helping you make more informed decisions.

Understanding the Fee Landscape

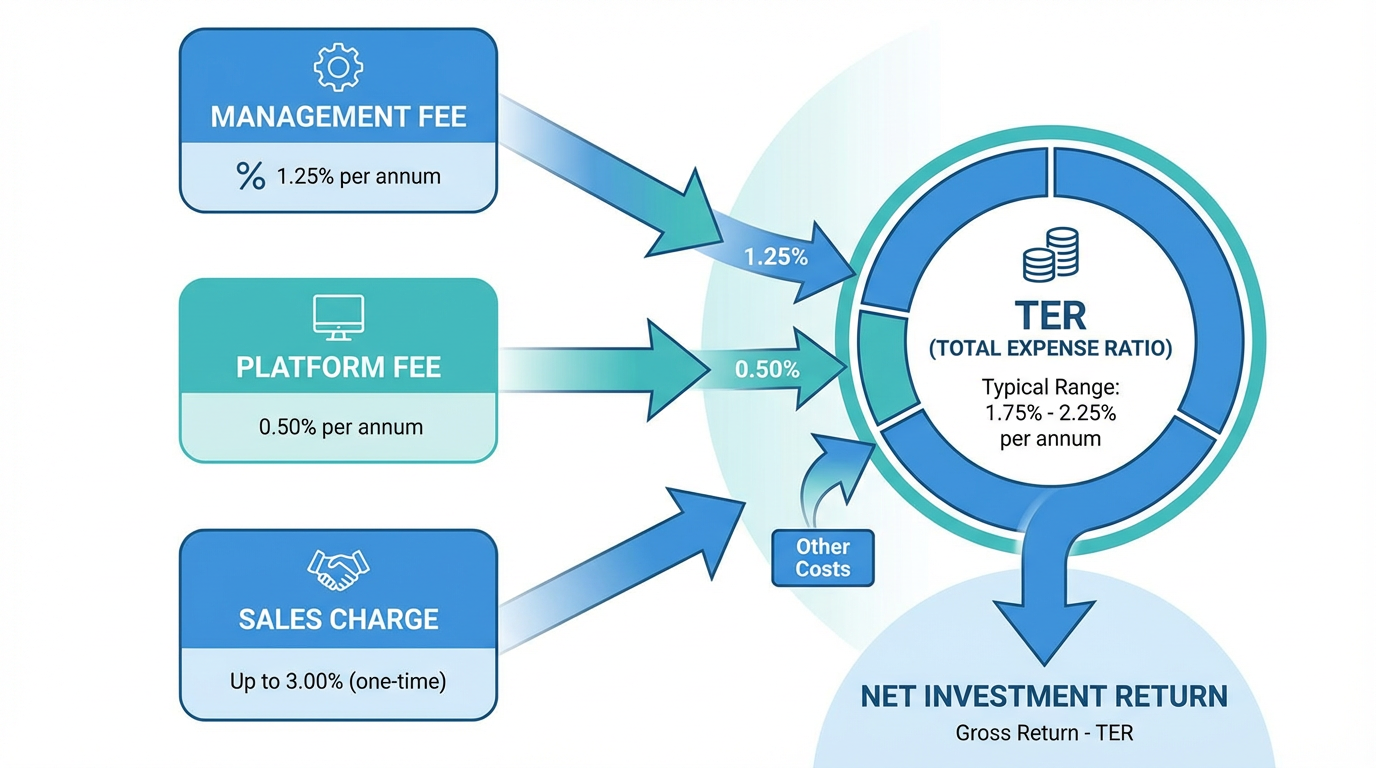

Mutual fund fees in Singapore generally fall into two main categories: one-time transaction fees and ongoing annual charges. Transaction fees occur when you buy, sell, or switch between funds. Annual charges are deducted continuously from your investment, regardless of fund performance.

Management Fees: The Foundation Cost

Management fees compensate the fund manager for researching opportunities, making investment decisions, and overseeing your portfolio. In Singapore, these fees typically range from 1.0% to 2.0% per annum for actively managed funds. The fee is deducted daily from the Net Asset Value (NAV) before you see the published price.

What many investors miss is that management fees vary by share class. The same fund might offer institutional shares at 0.55% and retail shares at 1.45%. This means two investors in the identical portfolio can pay drastically different fees based solely on which share class they access through their platform.

Total Expense Ratio: The Complete Picture

While management fees represent the largest component, the Total Expense Ratio (TER) includes all ongoing costs. Beyond management fees, TER encompasses:

-

Administrative expenses for record-keeping and reporting

-

Custodian fees for safeguarding fund assets

-

Legal and auditing costs

-

Regulatory compliance expenses

-

Marketing and distribution charges

The TER provides a more accurate picture of what you actually pay annually. A fund advertising a 1.5% management fee might have a TER of 1.8%, meaning an additional 0.3% disappears for operational costs.

The Less Visible Costs Singapore Investors Often Miss

Beyond the standard management fees and TER, several less obvious charges can significantly impact your returns.

Platform Fees and Maintenance Charges

Platform fees can typically range from 0.1% to 0.3% per annum depending on your chosen distributor, typically deducted from your cash holdings. If you maintain minimal cash balances, platforms may automatically sell portions of your fund holdings to cover these charges. Some platforms charge wrap account fees of 1% to 3% upfront on new investments.

Trailer Fees: The Silent Commission

Trailer fees represent one of the most significant hidden costs. Fund managers may pay distributors 20% to 60% of the management fee as ongoing commission for maintaining the client relationship. While you never see this itemized, it is built into the management fee structure.

For a fund charging 1.5% management fees, as much as 0.9% might go to your platform or advisor as a trailer fee. This creates potential conflicts of interest, as distributors earn more from recommending higher-fee funds rather than better-performing alternatives.

Sales Charges and Redemption Fees

Sales charges, also called load fees, can reach 5% of your initial investment in Singapore. A front-end load of 3% means only $9,700 of your $10,000 investment actually purchases fund units. Some platforms now offer zero-sales-charge options.

Redemption fees apply when selling fund units within a specified holding period, while switching fees between funds typically range from 0.5% to 1%.

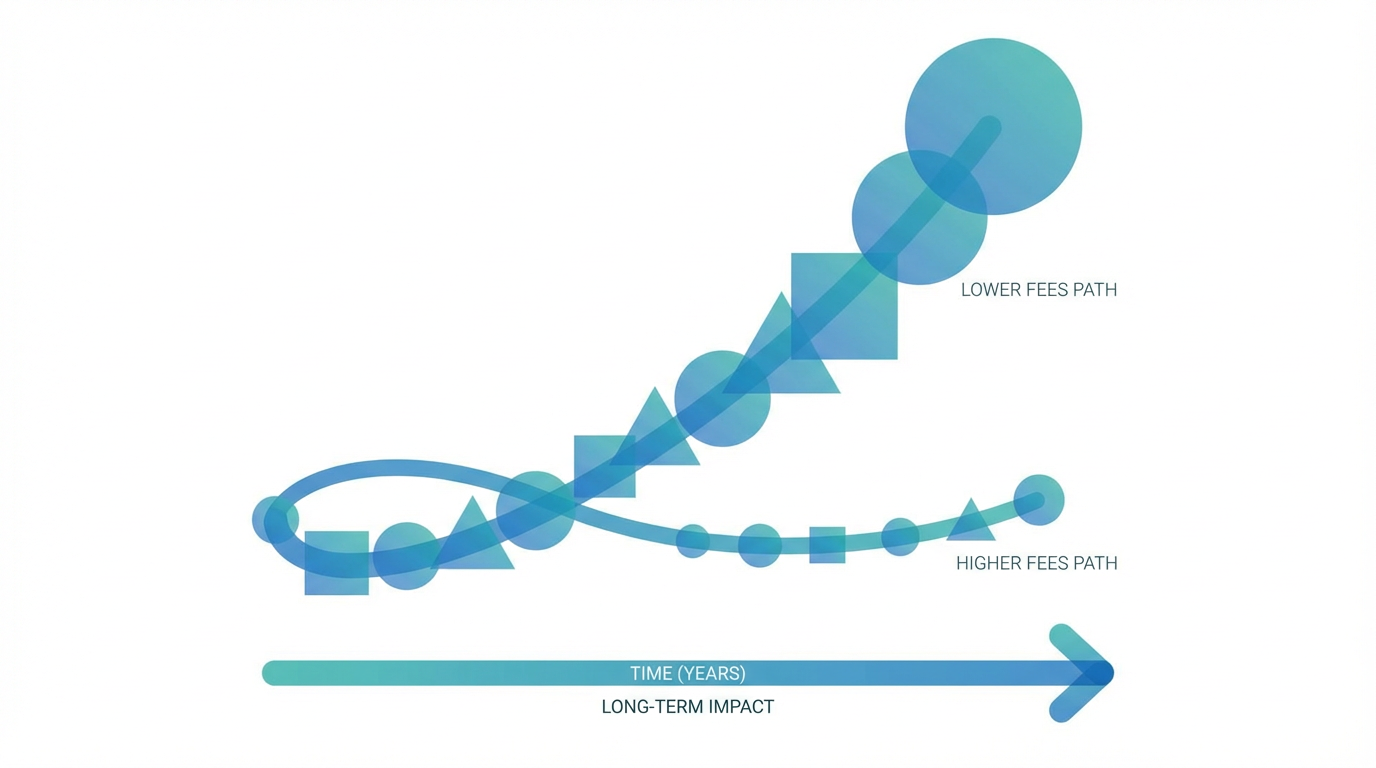

The Compounding Impact of Fees

Small percentage differences in fees create massive divergence in long-term wealth accumulation. For example, consider two investors, each starting with $10,000 and achieving 8% annual returns before fees over 20 years.

Investor A pays 0.5% in total annual fees and accumulates approximately $42,478.

Investor B pays 1.0% in total annual fees and accumulates approximately $38,697.

The 0.5% fee difference costs Investor B $3,781—nearly 10% less wealth despite identical gross returns. This calculation assumes no additional sales charges or platform fees, meaning the actual gap could be even wider.

Over a 30-year horizon, a 1% annual fee can consume nearly one-third of your portfolio value compared to a 0.3% fee structure. The compounding effect works against you, as fees are calculated on your entire portfolio value.

Tip: When comparing investment options, always calculate the projected impact of fees over your intended holding period, not just the annual percentage. Use online compound interest calculators to visualize how fees affect your specific investment scenario.

Ways to Minimize Mutual Fund Fees For Investors’ Consideration

Understanding fees is only valuable if you take action to minimize them. Several strategies can help Singapore investors reduce the drag of fees on their returns.

Choose Low-Cost Platforms

Platform selection significantly impacts your overall cost structure. Several Singapore platforms may now offer zero-sales-charge and zero-platform-fee access to mutual funds. Longbridge provides access to diverse investment products with transparent fee structures. When evaluating platforms, examine headline fees, redemption charges, switching fees, and minimum balance requirements.

Focus on Share Class Selection

If your platform offers multiple share classes for the same fund, always compare the fee structures. Institutional or direct share classes typically charge lower management fees than retail classes. Some platforms now provide access to institutional share classes at retail investment levels, allowing smaller investors to benefit from lower-fee structures.

Consider Passive Investment Alternatives

Exchange Traded Funds (ETFs) tracking similar indices typically charge 0.1% to 0.5% annually—substantially less than actively managed mutual funds. You can explore various investment options to compare how different fee structures align with your investment strategy and goals.

Review and Rebalance Regularly

Set an annual reminder to assess whether each fund justifies its cost through superior performance. If a fund consistently underperforms its benchmark after fees, investors may review performance relative to fees as part of their overall evaluation process.

Reading the Fine Print: What to Check

Before investing in any mutual fund, examine these key documents:

Prospectus Fee Table: Itemizes all shareholder fees and annual operating expenses, including hypothetical examples showing the dollar impact over different time periods.

Product Highlights Sheet: Singapore regulations require this document clearly stating the TER and any sales or redemption charges.

Platform Fee Schedule: Covers platform fees, custody charges, and transaction costs separate from the fund's internal expenses.

Historical Performance: Always examine returns after all fees, not gross performance.

Understanding Hidden Costs Beyond the Fee Table

Some costs never appear in the TER calculation. Transaction costs from portfolio turnover can add 0.5% to 1% annually for actively managed strategies. Funds with high turnover ratios incur more trading costs, directly reducing returns without appearing in published fee tables.

Many investors misunderstand Net Asset Value (NAV), assuming a rising NAV always indicates good performance. NAV reflects the per-unit value after all daily expense deductions. Focus on total return figures relative to the fund's stated benchmark rather than comparing NAV across funds.

Making Informed Decisions

Start by determining your investment timeline. Longer horizons magnify the impact of fees, making cost minimization more critical for retirement savings than short-term goals. Calculate the actual dollar impact of fees on your specific investment amount and timeline. A seemingly small percentage difference takes on new significance when translated into thousands of dollars in lost wealth accumulation.

Online investment education resources can help you understand how different fee structures impact various investment strategies. Remember that a fund delivering 10% gross returns with 2% in fees nets you 8%, identical to a fund producing 9% gross returns with 1% in fees—but the latter demonstrates better cost efficiency.

Frequently Asked Questions

What is the average mutual fund fee in Singapore?

Management fees for actively managed mutual funds in Singapore typically range from 1.0% to 2.0% per annum, with the Total Expense Ratio (TER) adding another 0.2% to 0.5%. Including platform fees and sales charges, total costs can reach 2.5% to 3.0% annually. However, increasing competition has driven some platforms to offer zero-sales-charge access.

How do I find out what fees I am paying on my mutual fund?

Check three primary sources: the fund prospectus fee table, the Product Highlights Sheet (required in Singapore), and your platform's fee schedule. Request a full fee disclosure from your platform if any charges remain unclear, as MAS regulations require transparent fee reporting.

Are mutual fund fees tax deductible in Singapore?

No, mutual fund management fees and other investment costs are not tax deductible for individual investors in Singapore. Singapore does not impose capital gains tax on fund appreciation or dividend income. This makes fee minimization even more important, as costs cannot be offset through tax deductions.

Can I negotiate mutual fund fees?

Individual retail investors typically cannot negotiate fund management fees, as these are set by the fund company. However, you can sometimes negotiate platform fees and sales charges with distributors, particularly for larger investment amounts. The most effective approach is choosing platforms that already offer competitive fee structures.

What is the difference between front-end and back-end loads?

A front-end load is a sales charge deducted when you purchase fund units, immediately reducing your invested capital. A 3% front-end load on a $10,000 investment means only $9,700 actually buys fund shares. Back-end loads, also called contingent deferred sales charges, are charged when you redeem units, typically decreasing the longer you hold the investment. Many back-end loads eliminate entirely after five to seven years, making them less costly for long-term investors than front-end loads.

Conclusion

Mutual fund fees in Singapore extend far beyond the advertised management fee, encompassing platform charges, trailer fees, sales loads, and operational expenses that collectively can consume 2% to 3% of your investment annually. Small differences in fee structures translate into substantial wealth divergence over investment horizons of 10, 20, or 30 years.

By selecting low-cost platforms, comparing share classes, and scrutinizing total cost structures, Singapore investors can preserve thousands of dollars that would otherwise disappear to unnecessary charges. Start by examining your current mutual fund holdings today. Calculate the actual dollar impact of fees on your portfolio and make adjustments where lower-cost options provide similar exposure. Your future wealth depends not just on market returns but on how much of those returns you actually keep.

Explore the Longbridge app to access investment products across Singapore, US, and Hong Kong markets. Learn more about optimizing your investment strategy.