Put-Call Parity: The Equation Every Trader Should Know

Put-call parity links call options, put options, and the underlying asset in a precise pricing relationship. Learn the formula, examples, and how to apply it in options trading.

TL;DR: Put-call parity is a fundamental pricing relationship that links the value of a call option, a put option, the underlying asset, and the risk-free rate. When this equation holds, markets are efficiently priced; when it breaks, arbitrage opportunities can emerge. Understanding it helps options traders assess fair value, construct synthetic positions, and spot mispricings.

Options trading can appear complex at first glance, but several foundational principles bring clarity to the mechanics. One of the most important is put-call parity — a pricing relationship that connects call options, put options, the underlying asset, and the risk-free interest rate. Whether you are new to options or looking to deepen your understanding, grasping put-call parity explained in straightforward terms is an essential step. This article walks through the concept, the formula, practical examples, and how traders apply it in practice.

What Is Put-Call Parity?

Put-call parity is a principle in options pricing theory that defines the relationship between the prices of European call options and European put options sharing the same underlying asset, strike price, and expiration date.

First formally described by economist Hans Stoll in his 1969 paper "The Relation Between Put and Call Prices," the principle is built on a simple no-arbitrage argument: two portfolios that produce identical payoffs at expiration must have the same value today. If they do not, traders will exploit the difference until prices realign.

European vs. American Options

Put-call parity strictly applies to European-style options, which can only be exercised at expiration. American-style options allow early exercise, making the relationship an inequality rather than an exact equation. The right to exercise early carries extra value — particularly for puts when interest rates are positive — which breaks strict parity. Whether early exercise is worthwhile depends on factors such as whether an option is in the money and how exercise and assignment work.

The No-Arbitrage Foundation

The logic underpinning put-call parity is that rational market participants will not allow a persistent pricing discrepancy to exist. If the equation is violated, arbitrageurs may buy the underpriced portfolio and sell the overpriced one, capturing the difference in theory and pushing prices back into alignment. In practice, real-world frictions erode such opportunities, so this is best understood as an idealised, self-correcting mechanism that keeps options prices tightly bound across liquid markets.

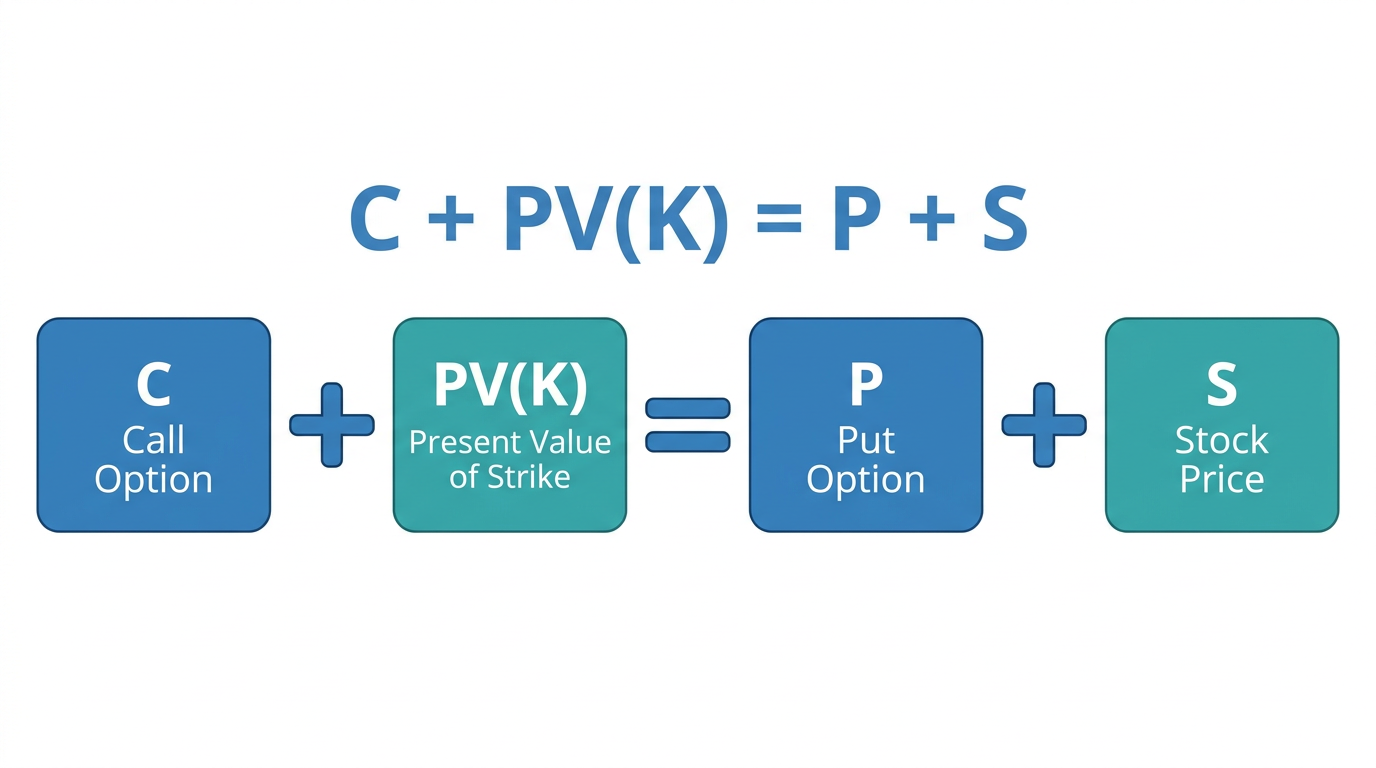

The Put-Call Parity Formula

The core formula for put-call parity is:

C + PV(K) = P + S

Where:

- C = Price of the call option

- PV(K) = Present value of the strike price (discounted at the risk-free rate)

- P = Price of the put option

- S = Current price of the underlying asset (spot price)

In plain terms: the price of a call option plus the present value of the exercise price equals the price of a put option plus the current stock price.

Breaking Down Each Component

The present value of the strike price, PV(K), is calculated by discounting the strike back from expiration to today using the risk-free interest rate. On the left-hand side, you hold a call option plus a cash position equal to that present value. On the right-hand side, you hold a put option and the underlying stock. Both sides deliver identical payoffs at expiration, regardless of where the stock price lands.

A Practical Example

Suppose a stock trades at USD 40, and both options have a strike price of USD 35 (these figures are hypothetical and for illustration purposes only, not investment advice). If the call is priced at USD 8 and the put at USD 3, the relationship holds: 8 minus 3 equals 40 minus 35. This confirms the prices are consistent with put-call parity. If the numbers do not balance, a potential mispricing exists.

Tip: Think of put-call parity as a balance scale. Both sides represent portfolios with identical outcomes at expiry — they must carry the same value today.

How Arbitrage Keeps Markets in Check

When put-call parity is violated, it can create an apparent arbitrage opportunity. In theory, a trader could construct positions designed to capture the pricing difference, though in practice real-world frictions tend to erode such gains. Understanding this mechanism explains why markets are generally efficient in options pricing.

For example, if a call option is overpriced relative to parity, a trader might sell the call, buy the put, and buy the underlying asset. This set of positions creates a synthetic equivalent of the call at a lower cost, capturing the pricing difference as profit.

Why Arbitrage Is Rarely Risk-Free in Practice

Transaction costs, bid-ask spreads, borrowing fees, and execution timing all erode potential gains in real markets. For retail investors, visible parity violations are often consumed by these frictions before any profit can be secured.

Professional arbitrageurs — particularly market makers — operate at scale with low transaction costs, enabling them to act on small deviations. Their activity is precisely what keeps put-call parity intact in liquid markets. For most individual investors, the greater practical value lies in using parity as a pricing validation tool rather than a direct trading strategy.

Synthetic Positions: Rearranging the Equation

A notable application of put-call parity is the ability to construct synthetic positions. By rearranging the equation, traders can replicate the payoff of one instrument using a combination of others:

- Synthetic call: Long put + Long stock (recreates the payoff of holding a call)

- Synthetic put: Long call + Short stock (recreates the payoff of holding a put)

- Synthetic stock: Long call + Short put at the same strike (equivalent to owning the stock)

Synthetic positions become valuable when a specific option is unavailable, illiquid, or priced unfavourably. They also appear in more advanced hedging strategies, where a trader adjusts exposure without altering a direct stock position. The same premium and time-value concepts also underpin related leveraged instruments, such as warrants and their premium and gearing calculations. You can explore the range of investment products available on the Longbridge platform, including options for US markets, to see where these strategies may apply.

The Effect of Dividends and Interest Rates

Two factors commonly cause confusion when applying put-call parity in practice: dividends and interest rates.

Adjusting for Dividends

The standard formula assumes no dividends. In reality, a stock's price drops by approximately the dividend amount on the ex-dividend date. The adjusted formula subtracts the present value of expected dividends from the stock price:

C + PV(K) = P + [S – PV(D)]

Ignoring dividends is one of the most common reasons traders observe apparent parity violations that are not genuine arbitrage opportunities.

The Role of Interest Rates

A higher risk-free rate increases the present value discount on the strike price, affecting the relative pricing of calls versus puts. Call premiums tend to rise when interest rates increase; put premiums tend to fall. Both factors are worth factoring in whenever you compare options prices across strike prices or expirations.

Tip: When comparing call and put prices, always account for the current risk-free rate and any expected dividend payments. These two variables explain many apparent discrepancies in options pricing.

Connecting Put-Call Parity to the Black-Scholes Model

Put-call parity is built into the Black-Scholes options pricing model, a widely used framework in quantitative finance. Developed in 1973, Black-Scholes provides a formula for pricing European options, and put-call parity is structurally embedded in it.

If you use Black-Scholes to price a call option, you can rearrange the equation using put-call parity to derive the corresponding put price — and the two will always be consistent. This consistency check validates whether a pricing model is producing coherent outputs. Longbridge's market data services allow traders to track options pricing and other market instruments in real time.

Practical Takeaways for Options Traders

Put-call parity has several direct applications for traders at all experience levels:

- Valuing options: If you know a call price, use parity to estimate the fair value of the corresponding put — and vice versa.

- Spotting mispricings: Significant deviations in liquid markets may signal a temporary pricing inefficiency worth investigating.

- Building hedges: Parity relationships underpin standard hedging strategies, including protective puts, covered calls, and collars.

- Interpreting quotes: Options market makers use parity continuously. Understanding this helps you read the prices you encounter when trading.

For traders looking to deepen their knowledge, the Longbridge Academy offers educational resources covering options, derivatives, and broader investment strategies.

Frequently Asked Questions

What is put-call parity in simple terms?

Put-call parity is a rule that links the price of a call option and a put option on the same stock, with the same strike price and expiry date. The two options, combined with the stock and a cash position, must be priced in a way that, in theory, leaves no room for arbitrage. If the prices fall out of balance, market forces tend to self-correct.

Does put-call parity apply to all options?

Put-call parity applies strictly to European-style options, which can only be exercised at expiration. For American-style options, which allow early exercise, the relationship holds as an inequality rather than an exact equation. Most index options are European-style; equity options in markets such as the United States are typically American-style.

How do dividends affect put-call parity?

Dividends affect put-call parity because a stock's price is expected to drop by roughly the dividend amount on the ex-dividend date. The standard formula must be adjusted by subtracting the present value of expected dividends from the current stock price. Failure to account for dividends is a common source of apparent — but non-exploitable — parity violations.

Conclusion

Put-call parity is one of the foundational principles in options trading. It establishes a precise, mathematically grounded relationship between call prices, put prices, the underlying asset, and the risk-free rate. When this relationship holds, it reflects efficient, coherent pricing. When it breaks, market forces restore balance.

For traders, its practical value lies in verifying fair value, constructing synthetic positions, and understanding how options pricing models are structured. It is also a gateway to more advanced options strategies, from protective puts to complex arbitrage structures.

Building a solid understanding of put-call parity is an essential step for any investor looking to engage with derivatives markets with clarity and discipline.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.