Warrant Premium Calculation: Hong Kong Market Guide

Understand how to calculate warrant premium in Hong Kong markets with step-by-step formulas, practical examples, and key factors that impact warrant pricing.

TL;DR: Warrant premium measures how much the underlying asset price needs to move to reach break-even at expiry. For call warrants, calculate using: {[(Exercise Price + (Warrant Price × Conversion Ratio)) / Underlying Price] - 1} × 100%. While premium is useful for understanding break-even points, implied volatility is more reliable for evaluating whether a warrant is expensive or cheap.

When trading derivative warrants in Hong Kong, understanding warrant premium is essential for making informed investment decisions. The premium tells you exactly how much the underlying stock price needs to move before you break even at expiry. However, many investors misuse this metric when comparing warrants. This guide explains how to calculate warrant premium hk accurately and use it appropriately in your trading strategy.

Hong Kong's derivative warrant market offers diverse opportunities for investors seeking leveraged exposure to stocks and indices. Longbridge provides access to investment products including warrants across Hong Kong markets, enabling Singapore-based traders to participate in this dynamic market segment.

What Is Warrant Premium?

Warrant premium represents the degree by which the price of the underlying asset needs to move before reaching the break-even price at expiry. According to guidance from major HKEX, if a call warrant has a premium of ten percent (10%), the underlying stock price must rise by ten percent (10%) at expiry for the warrant holder to break even.

Think of premium as the "hurdle rate" your investment needs to clear. This metric directly impacts your break-even point and helps you assess whether the warrant's pricing aligns with your market outlook.

Premium Versus Implied Volatility

A common misconception is that warrant premium indicates whether a warrant is expensive or cheap. In reality, implied volatility serves this purpose more effectively. Premium is influenced by multiple factors including time to expiry and whether the warrant is in-the-money (ITM) or out-of-the-money (OTM).

Generally, ITM warrants display lower premiums while OTM warrants command higher premiums due to gearing effects. A warrant with longer time to expiry typically has higher premium than one with shorter duration. These relationships make premium unreliable for direct price comparisons across different warrant structures.

Understanding the Premium Formula

The calculation method differs between call and put warrants, requiring specific formulas for each type.

Call Warrant Premium Calculation

For call warrants and bull Callable Bull/Bear Contracts (CBBCs), use this formula:

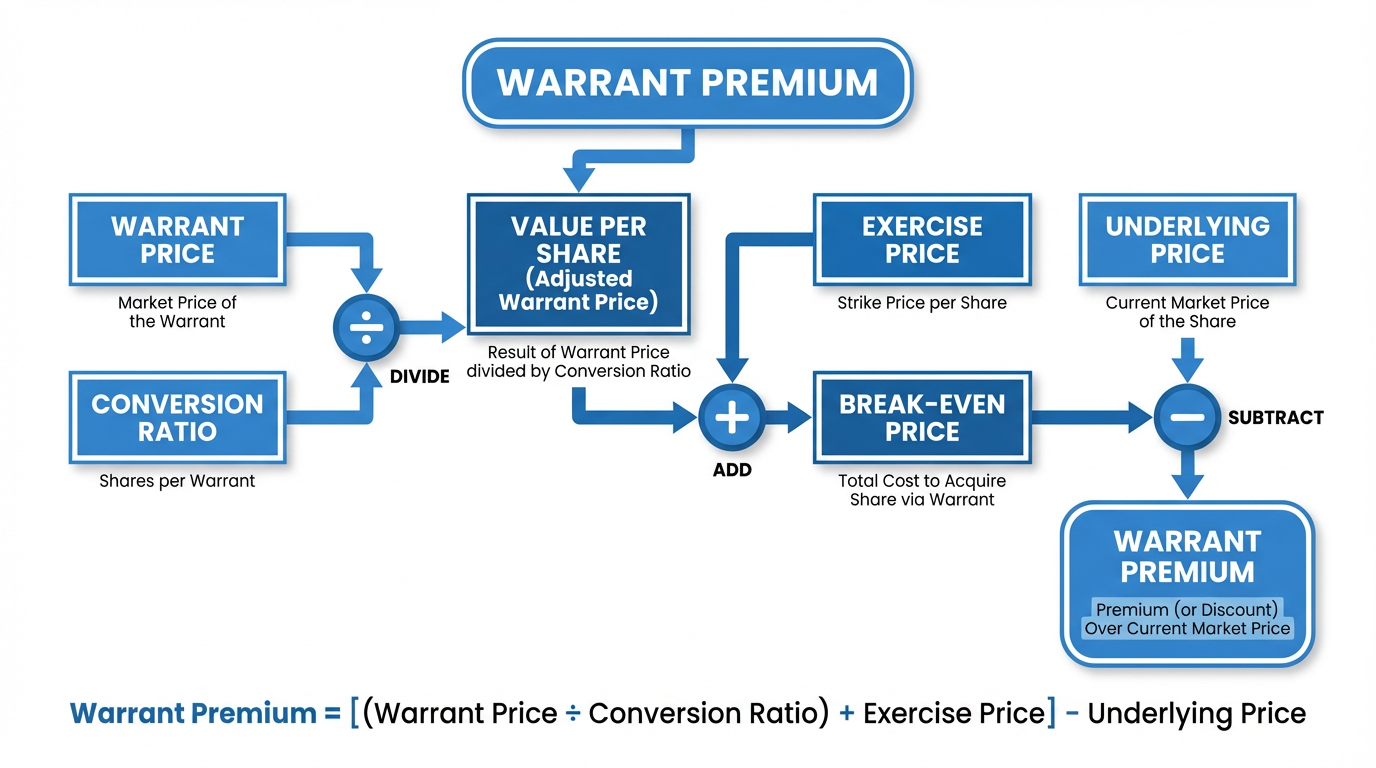

Premium = {[(Exercise Price + (Warrant Price × Conversion Ratio)) / Underlying Price] - 1} × 100%

Let's break down each component:

-

Exercise Price: The price at which you can buy the underlying asset

-

Warrant Price: The current market price of the warrant

-

Conversion Ratio: How many warrants equal one share of the underlying (for example, 10:1 means ten warrants equal one share)

-

Underlying Price: The current market price of the underlying stock or index

Put Warrant Premium Calculation

For put warrants and bear CBBCs, the formula inverts the relationship:

Premium = {1 - [(Exercise Price - (Warrant Price × Conversion Ratio)) / Underlying Price]} × 100%

This formula accounts for the fact that put warrants profit when the underlying price falls rather than rises.

Worked Example: Calculating Call Warrant Premium

Understanding the formula is easier with a practical example. Consider this scenario:

-

Underlying stock price: HKD 100

-

Call warrant price: HKD 0.50

-

Exercise price: HKD 105

-

Conversion ratio: 10:1 (ten warrants per share)

Applying the call warrant premium formula:

Premium = {[(105 + (0.50 × 10)) / 100] - 1} × 100%

Premium = {[(105 + 5) / 100] - 1} × 100%

Premium = {[110 / 100] - 1} × 100%

Premium = {1.10 - 1} × 100%

Premium = 0.10 × 100% = 10%

This means the underlying stock must rise from HKD 100 to HKD 110 (a ten percent increase) by expiry for you to break even, excluding transaction costs.

Understanding Break-Even Price

The break-even calculation connects directly to premium. In the example above:

Break-even price = HKD 100 × (1 + 0.10) = HKD 110

If the stock trades at HKD 110 at expiry, the intrinsic value of your warrant position equals your initial investment. Any price above HKD 110 generates profit, while prices below result in losses.

Key Factors That Influence Warrant Premium

According to the Hong Kong Exchanges and Clearing Limited (HKEX), derivative warrant prices are affected by multiple variables beyond the underlying asset price. Understanding these factors helps you interpret premium values correctly.

Time to Expiry

Longer-dated warrants typically display higher premiums than near-expiry warrants because more time provides greater opportunity for favourable price movements. As expiry approaches, time value decays, potentially reducing premium.

Moneyness (ITM, ATM, OTM)

In-the-Money (ITM) warrants typically show lower premiums while Out-of-the-Money (OTM) warrants command higher premiums due to greater gearing. This relationship explains why simply comparing premium percentages across warrants can be misleading.

Volatility and Other Factors

Implied volatility significantly impacts warrant pricing. Higher volatility increases the probability of large price movements, making warrants more valuable. Access to real-time warrant pricing data helps you monitor these changes.

Interest rates and expected dividends also affect premium. For call warrants, higher expected dividends may reduce premium since warrant holders do not receive dividends.

Using Premium to Compare Warrants

While premium has limitations for warrant comparison, understanding when and how to use it appropriately remains valuable.

When Premium Comparison Works

Premium comparison is most useful when evaluating warrants with the same underlying asset, similar expiry dates, and comparable moneyness levels (all ITM, all OTM, or all ATM). Under these conditions, premium differences may indicate relative value opportunities.

When to Use Implied Volatility Instead

For comparing warrants with different expiry dates, strike prices, or underlying assets, implied volatility provides a more reliable measure. Experienced warrant traders prioritize implied volatility over premium when assessing whether a warrant is attractively priced.

The Conversion Ratio Effect

The conversion ratio significantly impacts premium calculations but does not affect your percentage returns. Consider two call warrants on the same underlying with identical terms except:

-

Warrant A: Conversion ratio 10:1, price HKD 0.50

-

Warrant B: Conversion ratio 5:1, price HKD 1.00

Both warrants provide identical economic exposure and percentage returns, though Warrant B appears more expensive per unit. The premium calculation accounts for this through the conversion ratio multiplier, ensuring accurate break-even analysis.

Common Misconceptions About Warrant Premium

Several misunderstandings about warrant premium can lead to poor investment decisions. Lower premium does not necessarily mean better value as ITM and OTM warrants have different risk-return profiles and gearing levels. Premium measures break-even hurdles, not time value alone. Zero or negative premiums are rare and typically involve deep ITM warrants with dividend or transaction cost factors rather than genuine arbitrage opportunities.

Practical Applications in Warrant Trading

Understanding warrant premium supports several practical trading applications. Use premium to set objective profit targets above break-even levels. For example if you buy a call warrant with twelve percent (12%) premium on a stock at HKD 50, break-even is HKD 56, so you may want to consider targeting HKD 60 or higher for profit.

Higher premium warrants face steeper time decay challenges, particularly as expiry approaches. This awareness helps you select appropriate holding periods and exit strategies. When comparing deep ITM call warrants to margin trading, remember that warrant holders do not receive dividends, which offsets some apparent premium advantages.

Important Risk Reminder: Derivative warrants are complex instruments with substantial risks including potential total loss of investment. Always assess your risk tolerance and investment objectives before trading warrants.

Frequently Asked Questions

What does a high warrant premium indicate?

A high warrant premium means the underlying asset needs a larger percentage move to reach break-even at expiry. High premiums typically occur with out-of-the-money (OTM) warrants or longer-dated warrants. However, high premium does not automatically mean poor value as these warrants often provide higher gearing and leverage. Evaluate implied volatility alongside premium to assess true value.

How often should I recalculate warrant premium?

Recalculate warrant premium whenever the underlying price, warrant price, or other variables change significantly. For active traders, monitoring premium daily or even intraday helps track how close you are to break-even as market conditions evolve. Most trading platforms display current premium automatically, eliminating manual calculation needs.

Can warrant premium be negative?

Yes, premium can be negative for deep in-the-money (ITM) warrants, particularly calls on high-dividend stocks. Negative premium indicates the break-even price is below the current underlying price, reflecting factors such as dividend payments that warrant holders do not receive. Negative premium situations may present opportunities but require careful analysis of carrying costs and dividends.

Is premium more important than delta for warrant selection?

Premium and delta serve different purposes. Premium indicates the break-even hurdle, while delta measures price sensitivity to underlying movements. Delta helps you understand leverage and risk exposure, making it crucial for position sizing and risk management. Use premium for break-even analysis and delta for understanding how your warrant behaves as the underlying price changes. Both metrics are important for comprehensive warrant evaluation.

How does conversion ratio affect my actual returns?

Conversion ratio does not affect your percentage returns when comparing equivalent economic exposures. A warrant with 10:1 ratio at HKD 0.50 provides identical returns to a warrant with 5:1 ratio at HKD 1.00, assuming all other terms are equal. The conversion ratio adjusts the units you trade but not the underlying economics. Always calculate premium using the conversion ratio to ensure accurate break-even analysis.

Conclusion

Warrant premium is a fundamental metric for understanding break-even requirements in Hong Kong's derivative warrant market. By mastering the calculation formulas for both call and put warrants, you gain clarity on the price movements needed to achieve profitability at expiry.

Remember that premium primarily serves break-even analysis and should not be your sole criterion for warrant selection. Complement premium analysis with implied volatility assessment and delta evaluation. Understanding when premium provides useful insights versus when other metrics matter more distinguishes informed traders from those who misapply this important concept.

Explore the Longbridge app to access Hong Kong warrants and market data. Learn more about warrant trading through our educational resources.