CPF Investment Scheme: Using CPF for Stock Investments

The CPF Investment Scheme (CPFIS) lets eligible Singaporeans invest OA and SA savings in stocks, ETFs, bonds, and unit trusts. Discover how it works and what to consider before you start.

TL;DR: The Central Provident Fund Investment Scheme (CPFIS) allows eligible Singapore residents to invest their Ordinary Account (OA) and Special Account (SA) savings in approved products such as stocks, exchange-traded funds (ETFs), bonds, and unit trusts. Participation requires a minimum balance of SGD 20,000 in the OA (or SGD 40,000 in the SA), plus completion of a mandatory Self-Awareness Questionnaire. Because CPF accounts already earn guaranteed interest, investing through CPFIS carries real risk and demands careful consideration.

For many Singaporeans, the Central Provident Fund (CPF) represents the bedrock of retirement planning. But beyond the familiar Ordinary Account (OA) and Special Account (SA) interest rates, there is an avenue that lets you put those savings to work in the financial markets: the CPF Investment Scheme (CPFIS). Introduced in 1986, CPFIS has evolved into a framework that encompasses stocks listed on the Singapore Exchange (SGX), ETFs, unit trusts, bonds, Treasury Bills (T-bills), and more. Whether you are a first-time investor exploring your options or an experienced trader looking to diversify your portfolio, understanding how the CPF investment scheme works, what the rules are, and what risks you take on is essential before committing any funds.

What Is the CPF Investment Scheme?

The CPF Investment Scheme is a government-endorsed programme that allows CPF members to invest their OA and SA savings in a range of Monetary Authority of Singapore (MAS)-regulated financial products. The central idea is straightforward: by taking on measured investment risk, members may achieve returns that exceed the default CPF interest rates, thereby growing their retirement nest egg at a faster pace.

Since its inception, CPFIS has expanded to cover a broad spectrum of asset classes. According to the CPF Board's investment statistics, as of 30 September 2025, members collectively held SGD 21.4 billion in CPFIS investments, a figure that reflects the scheme's scale within Singapore's retirement landscape.

Important note: All investments under CPFIS carry risk. It is possible to lose some or all of the capital invested. Past performance of any product does not guarantee future returns.

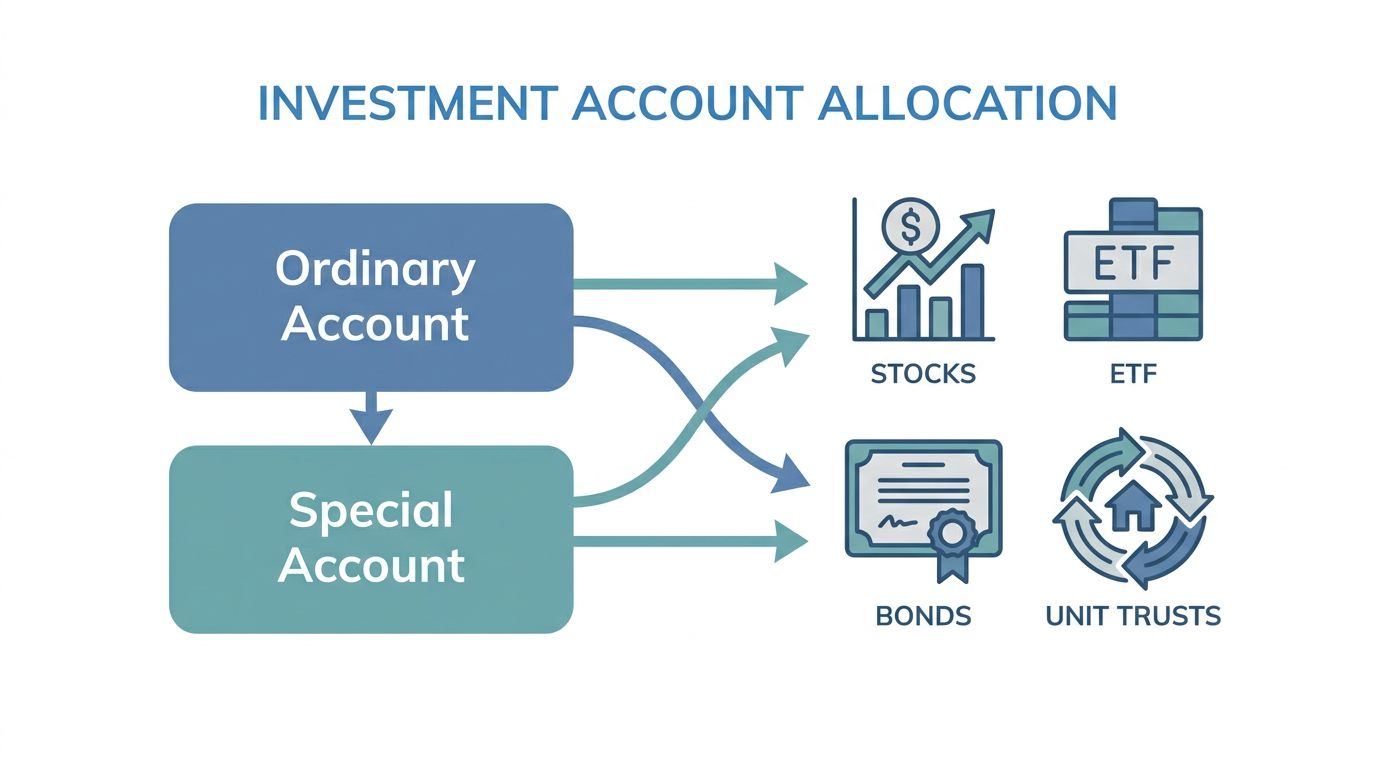

Two Distinct Components

CPFIS operates through two separate components:

- CPFIS-OA: Uses savings from your Ordinary Account. Offers a broader range of eligible products, including stocks and ETFs.

- CPFIS-SA: Uses savings from your Special Account. Limited to lower-risk products such as unit trusts and Singapore Government Securities (SGS) Bonds. Stocks, corporate bonds, and many ETFs are not available for SA investments.

Understanding this distinction matters because the SA currently earns a floor interest rate of 4% per annum, as set by the CPF Board. Any CPFIS-SA investment must therefore aim to outperform a 4% annualised return simply to break even against leaving funds in the account, a benchmark that has historically proven difficult to achieve consistently.

Who Is Eligible for CPFIS?

To participate in CPFIS, you must meet all of the following criteria as set out by the CPF Board:

- You are at least 18 years old.

- You are not an undischarged bankrupt.

- You have more than SGD 20,000 in your OA (for CPFIS-OA) and/or more than SGD 40,000 in your SA (for CPFIS-SA).

- You have completed the Self-Awareness Questionnaire (SAQ), a mandatory step for new CPFIS investors introduced on 1 October 2018.

The SAQ is designed to help you evaluate your financial knowledge and assess whether investing your CPF savings is appropriate given your circumstances. It is not a pass-or-fail test, but it does serve as a structured checkpoint before you begin.

How Much Can You Invest?

Your investible savings under CPFIS-OA are calculated as the sum of your current OA balance plus any amounts already withdrawn for investment or education purposes, minus the SGD 20,000 minimum balance you must retain.

For stock investments specifically, the CPF Board applies two additional caps:

- Stocks: Limited to 35% of your investible savings.

- Gold-related products: Limited to 10% of your investible savings.

To illustrate: if you have SGD 100,000 in your OA, your investible amount is SGD 80,000 (after the SGD 20,000 retention). Of that, you can allocate a maximum of SGD 28,000 (35% of SGD 80,000) to stocks. No such percentage caps apply to lower-risk products like T-bills or SGS Bonds.

There is no upper cap on the proportion of investible savings you can place into other approved products such as unit trusts or fixed deposits, beyond the total investible amount itself.

What Can You Invest In Under CPFIS?

CPFIS-OA offers the widest product range. The following categories are approved under the scheme, according to the CPF Board:

Stocks (Shares)

Eligible stocks are those listed on the SGX and specifically included on the CPFIS approved list. Stocks offer the potential for capital growth and dividend income, but they also carry a relatively high level of risk within the CPFIS framework due to market volatility and company-specific factors. Assessing valuation metrics such as the P/E ratio can help you evaluate individual SGX-listed shares before investing. The 35% cap on stock investments reflects this higher risk profile.

Exchange-Traded Funds (ETFs)

ETFs are funds listed on an exchange that track an index, commodity, or basket of assets. They combine diversification with trading flexibility and generally carry lower fees than actively managed unit trusts. CPFIS allows investment in a selection of SGX-listed ETFs, including an approved gold ETF for gold exposure (subject to the 10% gold cap).

Unit Trusts

Unit trusts are professionally managed pooled investment funds. The CPFIS-approved list covers a range from conservative fixed-income strategies to higher-risk equity funds. Each fund carries a Total Expense Ratio (TER) that varies by strategy and provider, so fee evaluation is important; the current TER for any specific fund can be confirmed on the CPF Board's CPF Investment Scheme options page.

Bonds

- Singapore Government Securities (SGS) Bonds: Government-backed, fixed-income instruments with maturities from 2 to 50 years, according to the Monetary Authority of Singapore.

- Treasury Bills (T-bills): Short-term government securities with maturities of up to one year.

- Corporate Bonds: Available under CPFIS-OA only, offering potentially higher yields than government bonds but with greater credit risk.

Fixed Deposits

Fixed-return products with a lock-in period that provide a defined return over the deposit term, with the trade-off of reduced access to the funds during that period.

Tip: For investors who find the product list overwhelming, checking the CPFIS-approved product list on the CPF Board's CPF Investment Scheme options page is the most reliable way to confirm current eligibility before placing any trades.

How to Get Started: A Step-by-Step Overview

The process for accessing CPFIS differs slightly depending on whether you are investing OA or SA savings.

Investing Your OA Savings

- Complete the SAQ: Log in to CPF's My CPF digital services via Singpass and complete the Self-Awareness Questionnaire.

- Open a CPF Investment Account (CPFIA): Visit one of the three designated CPFIS agent banks — DBS Bank, OCBC Bank, or United Overseas Bank (UOB) — and open a CPF Investment Account. Bring your National Registration Identity Card (NRIC) and a copy of your CPF statement.

- Engage a product provider or broker: For stocks, approach an SGX-approved broker. Your CPFIA is linked to your brokerage account, and the agent bank coordinates the settlement of trades with the CPF Board.

- Monitor your holdings: Log in to your CPF digital services under "My CPF" > "My Dashboards" > "Investment" to review your available investible savings and current holdings.

Investing Your SA Savings

You do not need to open a separate CPFIA for SA investments. Instead, approach the relevant product provider directly. Because the SA's approved list is more restricted, investment in stocks and most ETFs is not permitted via CPFIS-SA.

Key Risks and Considerations

The CPFIS can be a meaningful part of your broader investment strategy, but it is equally important to approach it with clear eyes about the risks involved.

You Are Competing Against Guaranteed Returns

Your OA currently earns 2.5% per annum, while your SA earns 4% per annum (the prevailing floor rates, per the CPF Board). Any CPFIS investment must generate returns above these rates, net of all fees and charges, to be worthwhile. Stock trades may incur broker commissions and minimum charges, while certain products carry annual wrap or management fees. These costs compound over time and erode returns, so it is worth confirming the applicable charges with your agent bank or product provider before investing.

Historical Participation Data

According to CPF Board data reported by the Ministry of Finance, 45% of CPFIS investors recorded losses over the period from 2013 to 2022, and around 25% of investors managed to outperform the CPF OA interest rate over that period. These figures are not a prediction of future outcomes, but they do underscore the importance of informed decision-making.

Long-Term Horizon Is Key

As with any equity investment, a longer time horizon allows you to absorb short-term market fluctuations. If you are approaching retirement age and your investment timeline is short, higher-risk CPFIS investments such as individual stocks may not align with your overall retirement readiness goals.

What Happens to Gains and Losses?

Investment gains made through CPFIS are credited back to your respective CPF account. Losses, however, reduce the balance in that account. Unlike CPF funds used to purchase property, there is no requirement to repay CPF if you incur investment losses through CPFIS; the loss simply reduces your account balance.

Is the CPF Investment Scheme Right for You?

There is no universal answer. For investors who have a long time horizon, a solid understanding of financial markets, and the discipline to monitor and manage a portfolio, CPFIS can offer meaningful diversification beyond the default interest rates. For others, particularly those with shorter time horizons or lower risk tolerance, leaving CPF savings to compound at their guaranteed rates may be the more prudent choice. Those exploring tax-advantaged retirement investing more broadly may also wish to look at SRS investment options and tax-advantaged funds alongside CPFIS.

Before proceeding, consider the following questions honestly:

- Do you have sufficient financial knowledge to evaluate the products you intend to invest in?

- Can your retirement plans withstand potential losses in your CPF account?

- Have you accounted for all fees and charges, including broker commissions and fund management costs?

- Are you prepared to review and manage your CPFIS portfolio regularly?

If you decide to explore CPFIS, platforms like Longbridge provide access to SGX-listed stocks and a range of investment products with transparent pricing, allowing you to review your options before committing. You can also explore the full range of investment products available and use tools such as a stock screener and market data services to research potential investments before making any decisions.

Frequently Asked Questions

What is the difference between CPFIS-OA and CPFIS-SA?

CPFIS-OA uses your Ordinary Account savings and allows investment in a wider range of products, including stocks, ETFs, bonds, and unit trusts. CPFIS-SA uses your Special Account savings but is restricted to lower-risk products such as unit trusts and SGS Bonds; stocks and most ETFs are not eligible. The SA also earns a higher guaranteed interest rate (4% per annum), making the hurdle rate for CPFIS-SA investments more demanding.

Can I invest all my CPF savings in stocks?

No. Stock investments under CPFIS-OA are capped at 35% of your investible savings (your OA balance minus the mandatory SGD 20,000 retention). You must also retain at least SGD 20,000 in your OA at all times. There is no provision to invest SA savings in stocks.

What happens to my CPFIS investments when I reach 55?

When you turn 55, a Retirement Account (RA) is created and the CPF Board transfers savings from your OA and SA to meet the Full Retirement Sum. Any CPFIS investments held at that point are not automatically liquidated, but the reduced OA and SA balances may affect your overall retirement planning. You should review your CPFIS holdings in advance to ensure they align with your retirement needs.

Are CPFIS investment gains subject to income tax in Singapore?

Under Singapore's tax regime as administered by the Inland Revenue Authority of Singapore (IRAS), capital gains are generally not taxed. Dividends from SGX-listed stocks received into your CPF account are also not subject to personal income tax. However, the tax treatment of specific products may vary, and you should consult a qualified tax adviser for guidance relevant to your situation.

Do I need to repay CPF if I lose money on CPFIS investments?

No. Unlike property purchases using CPF, where accrued interest must be returned to the CPF account upon sale, investment losses through CPFIS do not require repayment. The loss simply reduces your account balance. However, this also means your retirement savings are directly affected by those losses.

Conclusion

The CPF Investment Scheme gives eligible Singaporeans a structured path to potentially grow their retirement savings beyond the default CPF interest rates. By understanding the eligibility requirements, investment limits, approved product categories, fee structures, and the risks involved, you can approach CPFIS with a clear, informed perspective rather than treating it as a guaranteed route to higher returns.

The core question to ask yourself is whether the potential upside justifies the risk of reducing the guaranteed growth already built into your CPF accounts. If you decide to proceed, start with a disciplined approach: complete the SAQ, open the necessary accounts, research your chosen products thoroughly, and review your portfolio on a regular basis.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.