Guide to Multi-Currency Accounts in Singapore

Learn how a multi-currency account works in Singapore, who benefits, what fees to expect, and important deposit insurance considerations before opening one.

TL;DR: A multi-currency account lets you hold, send, and receive money in several different currencies from a single account, helping you avoid repeated conversion fees and gain greater control over your foreign currency funds. Singapore residents who invest internationally, travel frequently, or deal with overseas income will find these accounts particularly useful. Understanding how they work, what they cost, and where their limitations lie is key to deciding whether one suits your circumstances.

Managing money across borders has become a common reality for many people in Singapore. Whether you are an investor trading in overseas markets, an expat receiving income in foreign currencies, or a frequent traveller, dealing with multiple currencies can quickly become complicated and costly. A multi-currency account offers a practical solution, allowing you to consolidate several currencies under one account on your own terms.

This guide explains what a multi-currency account is, how it works, who benefits from one, and what to keep in mind before opening one.

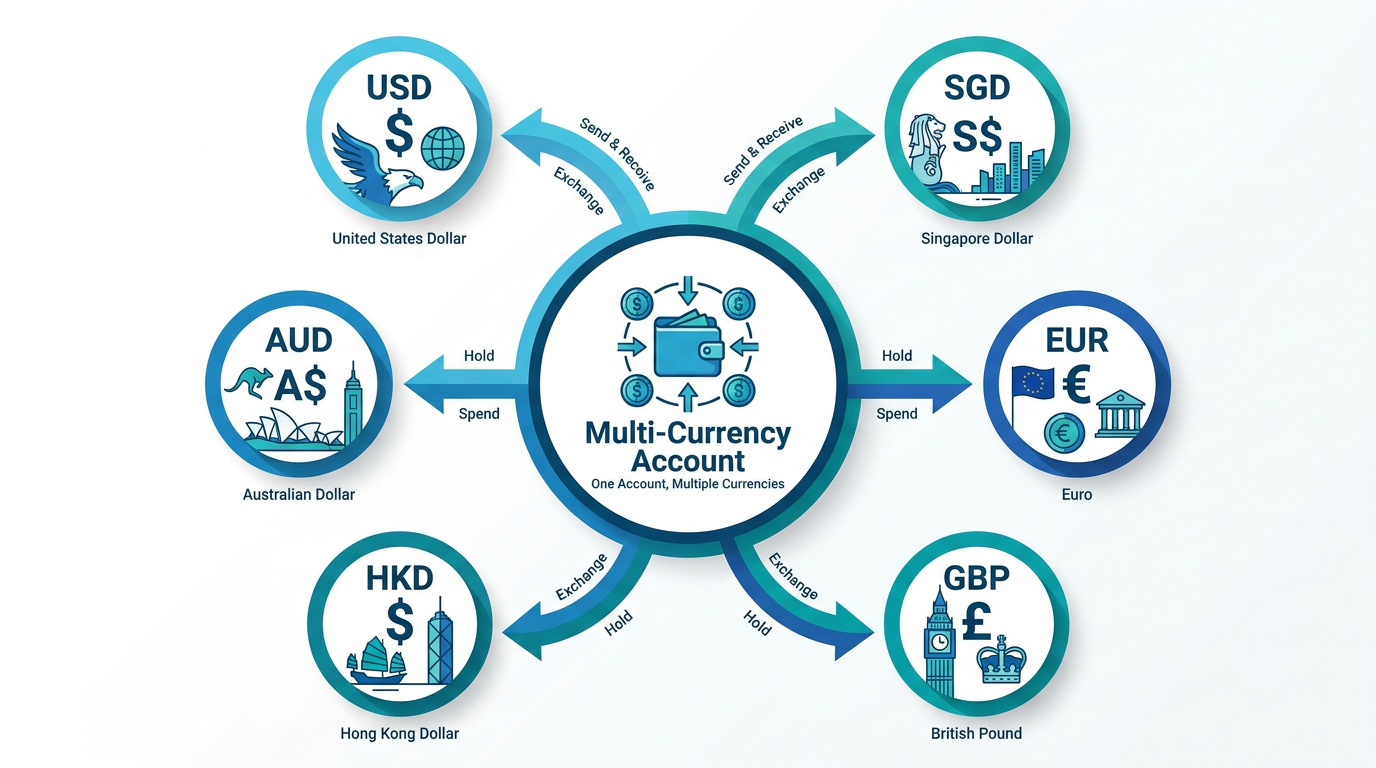

What Is a Multi-Currency Account?

A multi-currency account is a financial account that allows you to hold balances in more than one currency at the same time, within a single banking relationship. Instead of holding only Singapore Dollars (SGD), you can also maintain balances in currencies such as the United States Dollar (USD), Hong Kong Dollar (HKD), Euro (EUR), British Pound Sterling (GBP), or Australian Dollar (AUD), all in one place.

The key distinction from a standard bank account is that funds received in a foreign currency are not automatically converted into SGD. You choose when to convert, giving you flexibility to respond to favourable exchange rate conditions rather than being forced into conversions the moment a payment arrives.

How It Differs from a Regular Bank Account

With a standard account, receiving an overseas transfer typically triggers an automatic conversion at your bank's prevailing rate, which may include a markup over the mid-market rate. You pay conversion costs when money comes in and again when it goes out in another currency.

A multi-currency account separates receiving and converting into two distinct steps. You receive foreign currency, hold it, and convert when it suits you. This is not a guarantee of better rates, but it gives you greater agency over the timing.

Account Structures: What to Expect

Providers typically structure multi-currency accounts in one of two ways: a single account number with multiple currency wallets underneath it, or sub-accounts each with its own account details. Both allow you to hold and transact in several currencies, though the experience of managing them may differ depending on the platform.

Who Benefits from a Multi-Currency Account?

Multi-currency accounts are not a universal necessity. They tend to be most useful in specific situations where foreign currency transactions are a regular part of daily life or financial planning.

International Investors

If you invest in overseas markets — such as United States or Hong Kong equities — you are routinely dealing with currencies other than SGD. Receiving dividends in USD or settling trades in HKD without being forced to convert each time can reduce friction and costs. Longbridge offers access to Singapore, United States, and Hong Kong markets through a single platform, which means investors regularly manage multi-currency settlement flows. Holding the relevant foreign currencies ready in a dedicated account allows for smoother investment activity.

Tip: Even if you invest only in Singapore-listed stocks, indirect currency exposure can exist if those companies earn a significant portion of their revenue overseas. Understanding how currency movements affect your investments is as important as holding foreign currency itself.

Frequent Travellers and Expatriates

People who travel internationally regularly, or who live as expatriates receiving income in a currency different from SGD, often find it cost-effective to hold those currencies rather than converting every transaction. A multi-currency account can remove the need for repetitive exchanges.

Individuals with Overseas Income or Expenses

Freelancers paid in foreign currencies, property owners with overseas rental income, or individuals supporting family members abroad may also find value in holding foreign balances rather than converting on receipt.

Key Benefits of a Multi-Currency Account

Understanding what these accounts genuinely offer helps set realistic expectations.

Avoiding Repeated Currency Conversions

Without a multi-currency account, money moving through international transactions may be converted multiple times. Receiving USD, converting to SGD, then converting back to HKD for another payment means paying conversion costs at each step. Holding balances in the original currency eliminates unnecessary round-trips.

Flexibility in Timing Currency Exchange

Exchange rates fluctuate continuously. Holding a foreign currency balance means you can convert when rates are more favourable for your purposes, rather than converting at the moment a payment arrives. This is a practical advantage, though it also means you carry the risk that rates may move against you while you wait.

Simplified Account Management

Managing overseas investments, income, and expenses through one account rather than several separate ones reduces administrative complexity. Having USD, HKD, and SGD visible in one place makes it easier to track your overall financial position. For investors accessing multiple asset classes and geographies, keeping the relevant currencies consolidated supports a more integrated portfolio management approach.

Risks and Limitations to Consider

Every financial tool comes with trade-offs, and multi-currency accounts are no exception. Understanding the limitations is just as important as understanding the benefits.

Currency Risk

Holding foreign currency means your purchasing power in SGD terms can change based on exchange rate movements. A balance held in USD will be worth more or less in SGD depending on how the rate moves. This is not a risk that a multi-currency account eliminates; it is one the account helps you manage, but which you still carry.

Deposit Insurance Considerations

According to the Singapore Deposit Insurance Corporation (SDIC), Singapore Dollar deposits are insured for up to SGD 100,000 per depositor per Deposit Insurance Scheme member. Foreign currency deposits held with banks in Singapore are generally not covered by this scheme. For more details, refer to the Singapore Deposit Insurance Corporation (SDIC) scope of coverage.

Important: Foreign currency deposits are not covered by the SDIC deposit insurance scheme. Always check what deposit protection applies to the account type you are considering.

Fees and Minimum Balance Requirements

Multi-currency accounts may carry monthly maintenance fees, transaction fees, inactivity fees, or minimum balance requirements. Fee structures vary between traditional banks and financial technology providers, so reviewing the full fee schedule before opening an account is important, as fees can offset conversion savings.

Exchange Rate Markups

Even with a multi-currency account, the rate you receive when converting currencies is rarely the mid-market rate. Providers apply a spread or markup, the size of which varies and is worth examining when evaluating any account.

Multi-Currency Accounts and Investing in Singapore

For investors in Singapore, a multi-currency account is often one piece of a broader financial setup. When trading internationally, settlement currencies matter: United States equities typically settle in USD, while Hong Kong equities settle in HKD. Having those currencies readily available can remove delays associated with last-minute conversion.

Platforms like Longbridge support currency conversion as part of the investment process. Staying informed is equally essential; tools such as market data services can help you make better-informed decisions. The Longbridge Academy also provides educational resources on managing investment exposure across multiple markets.

What to Consider Before Opening a Multi-Currency Account

Before opening a multi-currency account, it is worth reflecting on a few practical questions.

How frequently do you transact in foreign currencies? If your international activity is occasional, a multi-currency account may not be necessary. Travel cards or one-off remittance services may be sufficient.

Which currencies do you actually need? Not all accounts support the same currencies. Confirm the account covers the currencies most relevant to your activity before committing.

What is the total cost? Monthly fees, transaction fees, and foreign exchange markups all contribute to the true cost. Weigh these against the savings you expect from reduced conversions.

Is the provider regulated? In Singapore, financial institutions and payment services are regulated by the Monetary Authority of Singapore. Confirming that any provider you consider is properly licensed is an essential step.

What level of deposit protection applies? Foreign currency deposits do not carry the same Singapore Deposit Insurance Corporation (SDIC) protection as SGD deposits. Understanding what protections apply to your funds is a fundamental part of the decision.

Frequently Asked Questions

What is a multi-currency account used for?

A multi-currency account is used to hold, send, and receive money in several currencies without being forced to convert immediately. It suits international investors, frequent travellers, expatriates, and anyone with ongoing overseas income or expenses.

Are foreign currency deposits in Singapore covered by deposit insurance?

No. According to the Singapore Deposit Insurance Corporation (SDIC), foreign currency deposits are not covered under Singapore's deposit insurance scheme. Only SGD deposits with scheme members are insured up to SGD 100,000 per depositor.

What are the typical fees associated with a multi-currency account?

Fees may include monthly maintenance charges, minimum balance requirements, transaction fees, inactivity fees, and foreign exchange markups. Always review the full fee schedule before opening an account.

Is a multi-currency account the same as a foreign currency account?

These terms are sometimes used interchangeably, but a multi-currency account supports several currencies within one account, whereas a foreign currency account is typically dedicated to a single currency.

Do I need a multi-currency account to invest in overseas markets?

Not necessarily. Some brokerage platforms handle currency conversion during settlement, so you can invest internationally without maintaining separate foreign currency balances. A multi-currency account can, however, offer greater flexibility and reduce the frequency of conversions over time.

Conclusion

A multi-currency account offers a practical way to manage foreign currencies with greater flexibility and control. For Singapore residents who invest internationally, receive foreign income, or deal with overseas expenses, understanding how these accounts work, what they cost, and where their limitations lie is valuable groundwork.

The decision to open one should be based on your financial activity, the currencies you regularly use, and a careful assessment of fees, exchange rate markups, and the deposit protection considerations specific to foreign currency balances.

The choice of financial instruments depends on your investment objectives, risk tolerance, market outlook, and experience level. Regardless of the method selected, it is essential to fully understand its mechanics, risk characteristics, and execution rules, while maintaining a robust risk management plan. You can learn more about investment strategies through the Longbridge Academy or by downloading the Longbridge App.