GF Securities: Optical

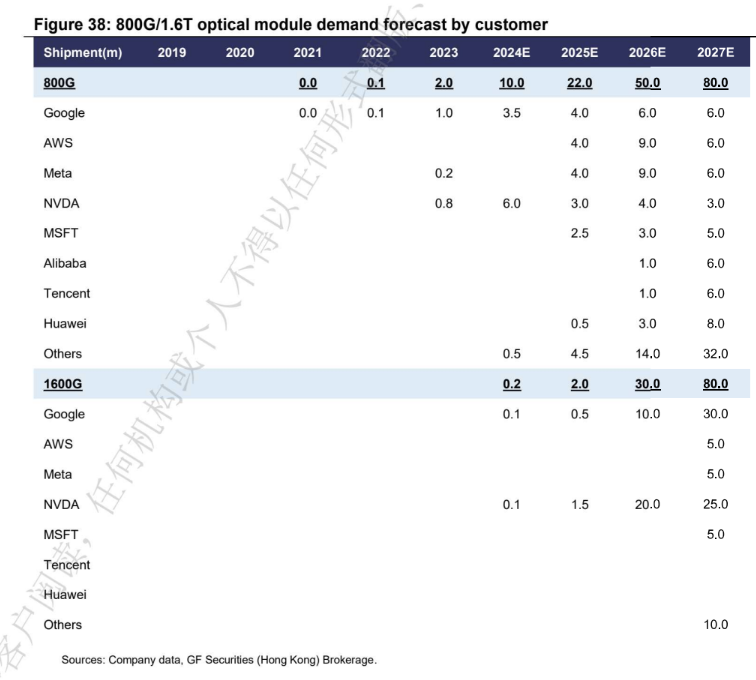

> Strong Demand Projections: Total demand for 800G/1.6T is expected to reach 80 million units each in 2027, driven by ramping accelerator demand from Nvidia, Google, AWS, and other ASICs, as well as rising GPU/ASIC scale-out bandwidth and optical module ratios.> CPO/NPO Adoption Timelines: CPO and NPO are being developed side-by-side in next-gen infrastructure, with CPO acting as the long-term design for lower power and latency, while NPO offers better short-term manufacturability and deployment flexibility starting around 2H27.> Nvidia Architecture Shifts: Each Rubin GPU is equipped with two CX9 NIC chips (doubling scale-out bandwidth versus Blackwell), and Rubin Ultra is estimated to adopt four CX9 chips per GPU, shifting the 1.6T optical module ratio from 1:2.5 up to 1:5.> Google's Scale-Up and Scale-Out Transition: Google is expected to fully transition to large-scale clusters in 2026 where the scale-up layer adopts optical interconnects, resulting in an overall TPU-to-optics ratio of approximately 1:4 (1.6T equivalent).> Supply Chain and Component Value Impacts: NPO shifts signal conditioning to system designs, lifting the value of TIAs and laser drivers to tens of dollars per 3.2T optical engine, benefiting supply chain players like Marvell and SMTC.$Applied Optoelectronics(AAOI.US) $Marvell Tech(MRVL.US) $Coherent Corp.(COHR.US) $Lumentum(LITE.US) $Alphabet(GOOGL.US) $NVIDIA(NVDA.US)

Equity research

Equity researchSuggestions for you to follow

E

Astera Labs on NPO/CPO:

"Once NPO gets deployed and database continues to increase, we will start to see CPO getting deployed. We look at it as 2027 being the year where NPO gets deployed, and then 2028 and beyond is when CPO gets deployed."$Applied Optoelectronics(AAOI.US) $Lumentum(LITE.US) $Tower Semicon(TSEM.US) $Coherent Corp.(COHR.US) $NVIDIA(NVDA.US) $Taiwan Semiconductor(TSM.US)E

$Arista Networks(ANET.US): "copper if you can, optics if you must. You're going to see a lot of copper in that two meter, three meter distance."

E![图片 1,共 2 张]()

![图片 2,共 2 张]()

RBC: Memory

DRAM Supply & Demand Forecast > Structural Deficit Trend: Sufficiency (measured as supply relative to demand) turns increasingly negative starting in mid-2025 and deepens through 2026, indicating that demand growth consistently outpaces supply expansion.> Peak Tightness: The market hits its most severe structural deficit in 1Q26A, where sufficiency drops to roughly -6.6%.> Volume Expansion: Both DRAM demand and supply scale significantly throughout 2026, with total market volume projected to climb from under 8,000 million GB in early 2024 to over 13,000 million GB by 4Q26E.NAND Supply & Demand Forecast > Transition to Deficit: After experiencing a period of oversupply with positive sufficiency peaking near +6.5% in 1Q25, the NAND market pivots sharply into a structural deficit by late 2025.> Deepest Deficit in Early 2026: Similar to DRAM, the NAND market bottoms out in terms of sufficiency at 1Q26A, reaching a deficit trough of approximately -7.5%.> Volume Scale: Demand and supply volumes steadily recover and expand through the remainder of 2026, approaching 330,000 million GB by 4Q26E.$Micron Tech(MU.US) $DRAM $EWY $Sandisk(SNDK.US)

E![图片 1,共 2 张]()

![图片 2,共 2 张]()

Morgan Stanley: Impact of Potential China Ban Reports

> News Overview: Reuters reported that the Trump administration and FCC are preparing restrictions on new Chinese data center components, with optical transceivers specifically targeted and potential rules going into effect this year.> Positive for Non-Chinese Suppliers: The potential ban is viewed as a positive read-through for non-Chinese optical component supply chains, alleviating near-term concerns regarding margin ceilings.> Top Beneficiaries:Coherent Corp (COHR) stands out as the clearest scaled beneficiary due to its vertical integration, given that Chinese suppliers Innolight and Eoptolink represent about 50% of the transceiver market.Lumentum Holdings (LITE) will benefit from longer-lasting tight EML (electro-absorption modulated laser) supply, though this is partly offset by potential Chinese restrictions on Indium Phosphide (InP) substrates.AAOI and FN are also positioned to absorb incremental demand.> Limited Impact Companies: Ciena (CIEN) has limited upside as it does not heavily compete in the data center space, and Corning (GLW) has limited upside since there is already minimal Chinese fiber deployed in US data centers.> Feasibility & Supply Chain Bottlenecks: Executing these restrictions is challenging due to tight existing supply and the reliance on Chinese firms (such as AXTI) for InP substrates, though cloud providers have increasingly qualified alternative suppliers over the past couple of years.$Ciena(CIEN.US) $Lumentum(LITE.US) $Applied Optoelectronics(AAOI.US) $Coherent Corp.(COHR.US) $Fabrinet(FN.US)E![图片 1,共 2 张]()

![图片 2,共 2 张]()

Goldman Sachs: CapEx Spend

Rapid Growth in Long-Term Estimates> Massive Scaling Through 2028: Consensus estimates show hyperscaler capex growing dramatically over time, starting from $154 billion in 2023 and climbing to an expected $1,298 billion (+24%) by consensus 2028.> Near-Term Acceleration: Spending for 2026 is projected to reach $792 billion (+92%) compared to 2025 levels ($412 billion).Upward Revisions During Reporting Seasons> Climbing Expectations for 2026 & 2027: Consensus capex estimates for 2026 and 2027 have continued to rise throughout the reporting season.At the start of 2026, estimates stood at $546 billion (2026) and $630 billion (2027).By the start of Q2 earnings, projections jumped to $757 billion (+84%) for 2026 and $929 billion (+23%) for 2027.Current Estimates sit even higher at $793 billion (+93%) for 2026 and $1,053 billion (+33%) for 2027.$Microsoft(MSFT.US) $Alphabet(GOOGL.US) $Amazon(AMZN.US) $Meta Platforms(META.US) $Oracle(ORCL.US)

E

$Palantir Tech(PLTR.US): "The assumption that the frontier is actually the best performing is just not borne out in practice. Within 24 hours of bringing Nemotron Ultra into our stacks, we found five production tasks where a standard Nemotron Ultra model without post-training beat frontier models."

E![图片 1,共 2 张]()

![图片 2,共 2 张]()

Morgan Stanley: Cloud CapEx

Cloud Capital Expenditure (Capex) Surges > Massive Uptick in 2027 Forecasts: Following recent US hyperscaler earnings, consensus for 2027 cloud capex has jumped significantly. The forecast is now tracking at approximately $1.2 trillion, a growth of around 30% year-over-year. This is a dramatic increase of about $170 billion and 15 points higher than predictions made just before the recent earnings. > A "too conservative" Consensus? While the current forecast predicts a slowdown in growth (to 29% Y/Y) for 2027 after an incredibly strong 2026, the report suggests this may be an underestimate. Morgan Stanley's own estimate is even higher at $1.4 trillion. The authors also note that aggregate estimates for the top 14 spenders have gone up in each of the last ten quarters.> The AI Impact: The sharp increase in spending, which is ~4x the historical capital spending intensity average for the sector, is clearly fueled by investment in artificial intelligence. The text notes that the current 2027 growth forecast of 29% implies that non-AI cloud capex growth would be just 7%.> Historical Spending Patterns: A historical chart shows the highly cyclical and recently explosive nature of this spending. Growth was modest for years, with negative growth as recently as 2019 and 2023, before skyrocketing to a projected 97% in 2026 and then potentially cooling to 29% in 2027 (though, as mentioned, that 29% figure is up significantly from a forecast of 14% just a month ago).$Alphabet(GOOGL.US) $Amazon(AMZN.US) $Microsoft(MSFT.US) $Meta Platforms(META.US)

E![图片 1,共 1 张]()

Morgan Stanley: "60%+ of enterprises use open-weights models as part of their stack, largely isolated to specific use cases requiring speed, security, or frequent use."

$NVIDIA(NVDA.US) $Microsoft(MSFT.US) $Alphabet(GOOGL.US) $Amazon(AMZN.US) $Meta Platforms(META.US)E![图片 1,共 3 张]()

![图片 2,共 3 张]()

![图片 3,共 3 张]()

J.P. Morgan: Memory TAM

DRAM TAM Forecast> Revenue Trajectory: Expected to grow from $77B in 2022 to $1,237B ($1.24T) by 2028E.> Peak Growth Year: 2026E marks a massive spike with a 346% year-over-year growth rate, jumping revenue to $636B.> Recent Trend: After market dips in 2022 (-16%) and 2023 (-36%), recovery began with a strong 91% growth surge in 2024 ($95B).NAND TAM Forecast> Revenue Trajectory: Projected to increase from $55B in 2022 to $454B by 2028E.> Peak Growth Year: Similar to DRAM, 2026E represents the steepest climb with a 322% year-over-year growth rate, pushing revenue from $71B in 2025 up to $300B.> Prior Performance: Following a downturn in 2022 and 2023 (-37%), the market rebounded sharply in 2024 with 101% growth ($70B).HBM TAM Forecast> Explosive Growth: High Bandwidth Memory (HBM) shows the most aggressive expansion, scaling from just $4B in 2023 to a projected $225B by 2028E.> Sustained Momentum: Year-over-year growth remains exceptionally high throughout the forecast period, peaking at 317% in 2024 ($17B) and maintaining high triple-digit or near-triple-digit growth through 2025 (98%), 2026E (94%), and 2027E (99%) before moderating to 74% in 2028E ($225B).E![图片 1,共 1 张]()

Barclays believes Google can generate $252.7 billion in sales of TPU externally in 2028 by shifting TPUs from internal GCP rentals to an off-platform merchant model, backed by JVs with Blackstone and Broadcom scaling past 11 GW.

External ASP would grow from $20,000 in 2026 to $53,333. $Alphabet(GOOGL.US)

E![图片 1,共 1 张]()

Speedrun | Upcoming Events This Week - [August 3 - August 7, 2026]

🌐 Geopolitical & Macro Updates: Iran Conflict & EnergyCeasefire Confusion: President Trump initially announced he was calling off planned strikes on Iran after requests from Middle Eastern countries and claims that a preliminary deal—including opening the Strait of Hormuz and ending nuclear threats—had been reached. However, Iranian state media quickly denied that any such deal exists.Oman Negotiations: Iran and Oman are in the final stages of negotiations regarding transit through the Strait of Hormuz, though Iran claims it is separate from closing or reopening the strait.Human & Economic Toll: The conflict has resulted in 653 U.S. military casualties (including 64 high-ranking officers).Gas & Inflation: Elevated gas prices (trending lower at $3.11/gallon from recent highs of $3.50) continue to drive inflationary concerns, which may prompt the Federal Reserve to consider a rate hike before year-end.📊 Earnings Calendar Highlights (August 3 – August 7)While major hyperscalers wrapped up earnings last week, several market-moving names are reporting this week:Monday ($Palantir Tech(PLTR.US),$ON Semiconductor(ON.US)): Focus on Palantir's high-growth sustainability and AI platforms, alongside ON Semiconductor's power semi demand.Tuesday ($AMD(AMD.US),$Arista Networks(ANET.US), $Astera Labs(ALAB.US),$Caterpillar(CAT.US)): Key items include AMD's sales growth and CPU demand, Arista Networks' networking demand, Astera Labs' supply dynamics, and Caterpillar's generator sales.Wednesday ($Sandisk(SNDK.US), $Western Digital(WDC.US),$TTM Tech(TTMI.US)): Sandisk and Western Digital will offer insight into NAND/HDD demand, margins, and outlooks, while TTM Technologies reports on PCB demand for AI.Thursday & Friday ($Applied Optoelectronics(AAOI.US), $Himax Tech(HIMX.US),$Aecom(ACM.US), $Oklo(OKLO.US),$Vistra(VST.US)): Focus areas include transceiver demand (AAOI), WFE spending in China (ACM), and AI power needs (Oklo, Vistra).📈 Market Sentiment & TechnicalsSemis Oversold: Semiconductors are currently experiencing their most oversold conditions since the late March bottom. However, the SOX index remains 19% off its peak, suggesting caution against FOMO buying.Risk/Reward: Many stock names are perceived as having a much better risk/reward profile compared to April and May.📅 Economic Calendar (Friday, August 7)Jobs Report: Nonfarm payrolls are expected to come in at 91K (up from prior), and the unemployment rate is expected to edge up to 4.3% (from 4.2%).Market Implication: A stronger-than-expected labor market could give the Fed more reason to implement a future rate hike, potentially driving bond yields higher.Link 👇

E![图片 1,共 3 张]()

![图片 2,共 3 张]()

![图片 3,共 3 张]()

Jensen Huang: "no HBM for you, I need HBM!"

Overall Market & Demand Growth> Massive Expansion: Total HBM demand is projected to scale dramatically, reaching over 6 million k GB (approx. 48,618 mn Gb) by 2027.> Rapid Multi-Year Trajectory: Historical and projected growth shows a steep upward curve from 2023 through 2027, driven heavily by increasing deployment in AI GPUs and AI ASICs.NVIDIA's Market Dominance> Leading Consumer: NVIDIA remains the single largest consumer of HBM supply, commanding the largest share of the demand stack in 2027.> Key Products: High-demand products like the Rubin R200 stand out with massive total HBM demand (projected at over $1.7 million k GB), utilizing advanced HBM4 12hi configurations.> CoWoS Allocation: NVIDIA dominates advanced packaging allocations, notably with massive wafer distributions for products like the Vera CPU and Rubin series.Key Competitors and Ecosystem Players> Google: Google represents a massive portion of the AI ASIC HBM demand, particularly driven by TPU lines such as the TPU v8i (Sunfish), which demands over 1.1 million k GB of HBM.> AMD: Competes strongly with advanced offerings like the MI455 and MI350 series, utilizing HBM3e and HBM4 configurations sourced primarily through Samsung and Micron.> Cloud Service Providers (ASICs): Other major tech giants like AWS (Trainium 3) and Microsoft (Maia 300) account for significant shares of the total specialized hardware demand footprint.> NVIDIA holds the largest single share of projected HBM consumption at 36%.> Google represents a massive segment of demand at 35%, nearly matching NVIDIA due to its heavy reliance on custom TPU deployments.> AMD follows as the third-largest consumer with 16% of the market share.> AWS accounts for 5%, GUC's customers make up 3%, while Microsoft and Meta each take 2% of the projected 2027 consumption.$NVIDIA(NVDA.US) $Meta Platforms(META.US) $Microsoft(MSFT.US) $AMD(AMD.US) $Alphabet(GOOGL.US) $Micron Tech(MU.US) $DRAM $EWYE![图片 1,共 1 张]()

Nvidia's announcement of co-packaged optics entering mass production provides a boost to optical communications.

"Gilad Shainer, Senior Vice President of NVIDIA, announced that Co-Package Optics (CPO) has entered mass production." "According to foreign media reports, Gilad Shainer announced at a recent technology forum that CPO has begun mass production. Switches developed by Nvidia in collaboration with its supply chain have been delivered to close customers and are also being deployed at Nvidia's own facilities. It is expected that a large number of switches with CPO technology will be introduced into AI factories around the world this year."E![图片 1,共 1 张]()

CMB International: CPO

> CPO Market Growth: Co-packaged optics (CPO) are projected to experience rapid expansion with a 219% revenue CAGR over 2025–30E, including 300%/350% YoY growth in 2026E/27E, driven primarily by early adopters.> Pluggable Optical Modules: Traditional pluggables will continue steady volume and technology growth, posting a 30% CAGR over 2025–30E alongside 58%/33% YoY growth in 2026E/27E.> Market Dynamics & Roles: CPO is not an immediate replacement for pluggables. Pluggables remain the near-term volume engine, while CPO/NPO act as faster-growing extensions addressing escalating AI network power, density, and copper-reach constraints.$Lumentum(LITE.US) $Coherent Corp.(COHR.US) $Applied Optoelectronics(AAOI.US) $Marvell Tech(MRVL.US) $Broadcom(AVGO.US)

E![图片 1,共 1 张]()

GF Securities is forecasting global WFE to reach $236 billion in 2027 and then $295 billion in 2028.

$ACM Research(ACMR.US) $KLA(KLAC.US) $ASML(ASML.US) $Lam Research(LRCX.US) $Applied Materials(AMAT.US)

E![图片 1,共 4 张]()

![图片 2,共 4 张]()

![图片 3,共 4 张]() +1

+1

BofA: Hyperscalers

Massive Capital Expenditure (Capex) Surge> Record Growth in 2025–2026: Combined capex for the top US tech companies (Amazon, Microsoft, Alphabet, Meta, and Oracle) is projected to grow ~65% YoY in 2025 to reach a massive scale, followed by an additional ~100% YoY jump in 2026 to hit $730 billion.> Hitting the $1 Trillion Milestone: Combined annual capex is expected to surpass $1 trillion per annum by 2027 and 2028.> Individual Hyperscaler Breakdown (2026E): Oracle and Alphabet lead the YoY percentage growth chart for 2026E with triple-digit increases (around 120% and 118% respectively), closely followed by Microsoft and Meta.Robust Cloud Revenue Growth> Consistent Expansion: Cloud revenue across major providers (AWS, Microsoft Azure, and Google Cloud) remains structurally strong, maintaining a solid 35–45% YoY growth trajectory through 2026–2028.> Revenue Trajectory: AWS continues to hold the top spot in total revenue terms heading into 2028, with Microsoft Azure and Google Cloud tracking closely behind on steep upward curves driven by surging AI infrastructure demand.Temporary Free Cash Flow (FCF) Pressure> Short-Term Dip: Driven by unprecedented AI infrastructure investments, several hyperscalers are expected to experience temporarily negative Free Cash Flow (FCF) through 2026 and 2027 as spending outpaces near-term cash flow growth.> Quarterly Volatility: Quarterly trends highlight notable dips into negative FCF territory for companies like Amazon and Alphabet during peak spending quarters before stabilizing.$Oracle(ORCL.US) $Microsoft(MSFT.US) $Meta Platforms(META.US) $Alphabet(GOOGL.US) $Amazon(AMZN.US)E![图片 1,共 3 张]()

![图片 2,共 3 张]()

![图片 3,共 3 张]()

BofA: Memory

DRAM Pricing Trends > Record Highs: DRAM spot and contract prices climbed to record highs of approximately US$35–40 following a strong rally in 4Q25 and 1Q26.> Growth Trajectory: After the sharp surge, prices are exhibiting moderate growth moving into 2Q26.> Spot vs. Contract: Both 16Gb DDR5 spot and contract prices remained relatively flat between 1Q23 and 3Q25 before experiencing a steep vertical breakout starting in late 2025.NAND Wafer Pricing Trends > Record-High Levels: Both 512Gb wafer spot and contract prices are currently at record-high levels.> Contract vs. Spot Dynamics: NAND wafer contract prices have surged significantly ahead of spot prices during the recent upswing.> Historical Baseline: Prices hovered stably between US$2 and US$5 from early 2023 through late 2025 before skyrocketing sharply into mid-2026.DDR4 vs. DDR5 Contract Price Comparison> Disappearance of Price Premium: DDR4 and 16Gb DDR5 contract prices have converged at similar levels (US$35–50 by mid-2026); the traditional DDR5 price premium no longer exists.> Driver of Convergence: The collapse of the price gap is driven primarily by an acute DDR4 shortage.Timeline: Both technologies tracked closely below US$10 until mid-2025, after which they escalated rapidly through July 2026.$Micron Tech(MU.US) $EWY $DRAME![图片 1,共 1 张]()

Lumentum leads in market share of laser chips

$Lumentum(LITE.US) $Broadcom(AVGO.US) $Coherent Corp.(COHR.US) $Macom Tech(MTSI.US)

E

Kioxia $258A.T earnings:

Consolidated Financial Performance (Q1 FY2027)Driven by robust demand centered on generative AI applications and strong average selling prices, the company achieved significant year-over-year growth: > Net Sales: 1,767,117 million yen (an increase of 415.5% or +1,424.3 billion yen compared to Q1 FY2026). > Operating Profit: 1,270,017 million yen (compared to 44,899 million yen in Q1 FY2026). > Non-GAAP Operating Profit: 1,326,216 million yen. Profit Before Tax: 1,234,720 million yen. > Quarterly Profit Attributable to Owners of the Parent: 842,165 million yen (a massive surge from 18,284 million yen in the same period last year).Sales Breakdown by Application> SSD & Storage: 1,174,719 million yen (up from 217,411 million yen in Q1 FY2026). > Smart Devices: 525,656 million yen (up from 79,040 million yen in Q1 FY2026). > Other: 66,742 million yen (up from 46,348 million yen in Q1 FY2026).Stock Split Resolution: The Board of Directors resolved on July 31, 2026, to execute a 3-for-1 stock split of common stock, with an effective date of October 1, 2026. Q2 FY2027 Outlook: Anticipating continued strong demand from data centers, Kioxia projects further sequential growth for Q2 (July 1 to September 30, 2026), forecasting net sales of 2,390,000 million yen and an operating profit of 1,890,000 million yen.E![图片 1,共 1 张]()

Situational Awareness is down around 67% so far in July. Including July's losses, the fund remains up about 80% on the year.

Impressive...E

$Amazon(AMZN.US): "We see a strong linkage between AI spend and core growth as customers invest in AI."

E

$Amazon(AMZN.US) Jassy: "it takes a little less than three years to break even on that investment [servers and networking equipment]."

E

$Amazon(AMZN.US) Jassy: "We've long believed AWS could become a few hundred billion dollars revenue business and now believe it will be at least double that and very possibly be $1 trillion annual revenue business for us in time with very appealing accompanying free cash flow and return on invested capital."

E

$AXT(AXTI.US): "We're seeing high demand from the industry migration to 800G and 1.6 T transceivers modules for which any phosphate based lasers and detectors are essential for higher performance optical links. Longer term hyperscalers are advancing towards near packaged and co-packaged optics, which will continue to drive increasing demand for our material overall."