Current market sentiment is absolutely unhinged.

1. Do you do anything related to AI? — Sell!2. Do you not do anything to do with AI? — Buy!Brutal market open with semis like $Aehr Test(AEHR.US), $Sandisk(SNDK.US), $Lumentum(LITE.US), $Coherent Corp.(COHR.US) and $Applied Optoelectronics(AAOI.US) all down -10% so far.Rough!

Paradi Lab

Paradi LabSuggestions for you to follow

P

Huge overreaction to the news that China has started mass producing DUV lithography machines.

The Information reported that these Chinese-made DUV machines are expected to be delivered this year to Chinese chipmakers such as: SMIC, Hua Hong Semiconductor, and CXMT.But is this really new information?Export controls on $ASML(ASML.US)'s EUV and DUV made indigenization inevitable, especially when you consider that SMIC has been trialling domestic immersion tools since Q3'25, and Reuters reporting on Chinese EUV prototype machines back in Dec'25.Plus, we already know that ASML's China sales have been declining recently: ~50% in 2024, 33% in 2025, ~20% guided for 2026.So the sell-off essentially double counts ASML's own guidance of falling Chinese sales.Overall, I am left scratching my head at this market reaction.P

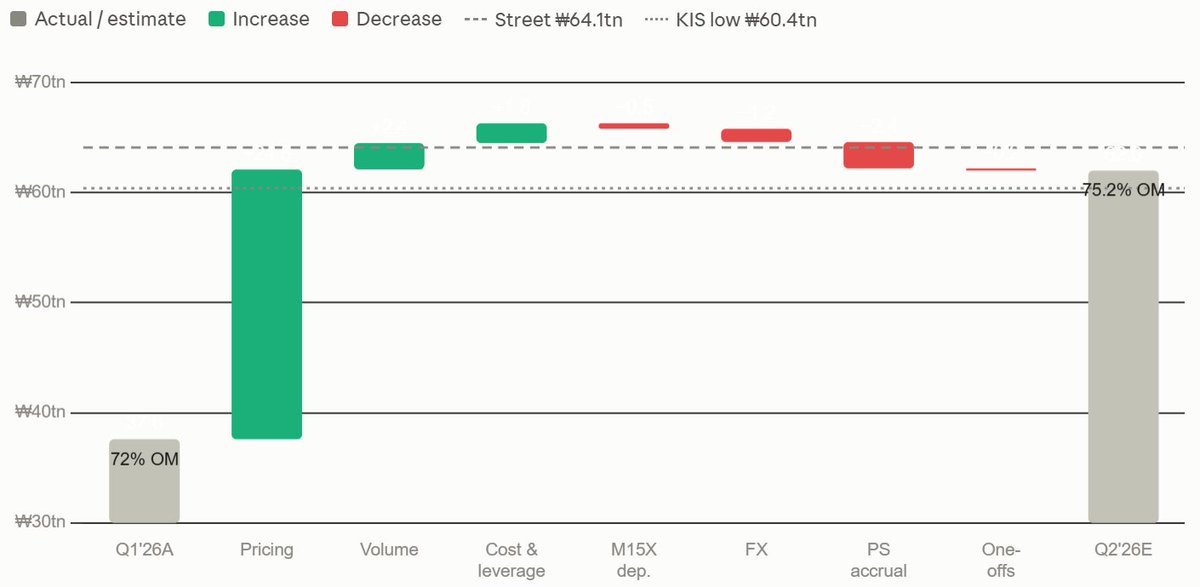

SK Hynix Q2 Earnings Preview & Explanations:

Q1 -> Q2 profit walk based on things like: revenue accruals, wafer economics, utilization game theory, etc.- Revenue: ₩82.5tn- Operating profit: ₩63.0tn- Margin: 76%Just sharing my estimates based on my ongoing research and assumptions.Q2 operating profit walk:1. Q1 2026 operating profit reported: ₩37.6T2. Pricing (DRAM blended ASP of plus low-40s%, NAND plus ~55%): +₩24.5T3. Volume (DRAM bits +6%, NAND bits +17%): +₩3.4T4. Cost-down & operating leverage: +₩1.8T5. M15X early-ramp depreciation & start-up costs: -₩0.5T6. FX (won appreciation reversing Q1 tailwind): -₩1.2T7. Profit-share accrual: -₩2.4T8. One-offs e.g. Nasdaq listing costs: -₩0.2T= Q2E operating profit of ₩63.0TMy operating profit is slightly below ₩64.1tn consensus, yet above KIS Securities of ₩60.4tn.Probably because of more conservative pricing numbers which I explain below.-> Pricing: +₩24.5TReally, this is where most estimates differ due to SK Hynix's DRAM book being repriced with the spot rate.Essentially, their book is split in two parts where roughly half is under multi year LTAs and the other half rides against the spot rate, which ran up 50-60% for convential DRAM in Q2.When you blend them, DRAM ASP comes to the low 40% range.NAND is a little cleaner w/ eSSD mix-shift + QLC contract momentum putting blended ASP at roughtly +55%. No LTA drag on this side either vs. DRAM.So just very conservatively assuming that volumes are flat, and then repricing the Q1 base (DRAM ~₩41.5tn, NAND ~₩10.5tn):Means that pricing along contributes ~₩25tn of revenue at the low end. Which flows down to OP at ~97% before any incentive lines kick in as price carries no wafer costs, only things like freight and royalty crumbs attach.Meaning that price is essentially pure margin (as we've become accustomed to).That's why pricing is probably way more important than volumes for memory companies right now. On sensitivity analysis also:Each "point" of blended DRAM ASP is worth ~₩0.42tn of operating profit.Which is why I have a gap to consensus estimates.The entire gap between me and consensus (₩2.1tn) is 4-5 points of DRAM ASP assumption.So consensus at ₩64.1tn is a bet that the spot-exposed half of SK Hynix's book is materially larger than half, or that LTA resets were more material than +15-25%.E.g. KIS Securities' model ₩60.4tn OP, which is essentially them using way more conservative pricing assumptions where they carry DRAM ASP nearer to +30%.Which means that they assume that the LTA portion of the book is more dominant. I believe that the real "truth" about the LTA structure, which SK hynix has never fully disclosed, gets revealed on Wednesday's earnings by the ASP numbers itself.So this quarter is a bit of an experiment into my modelling that actually measures their contract business.Regardless, it'll be fun to see how far off I was based on my limited info + static assumptions through Q2.P

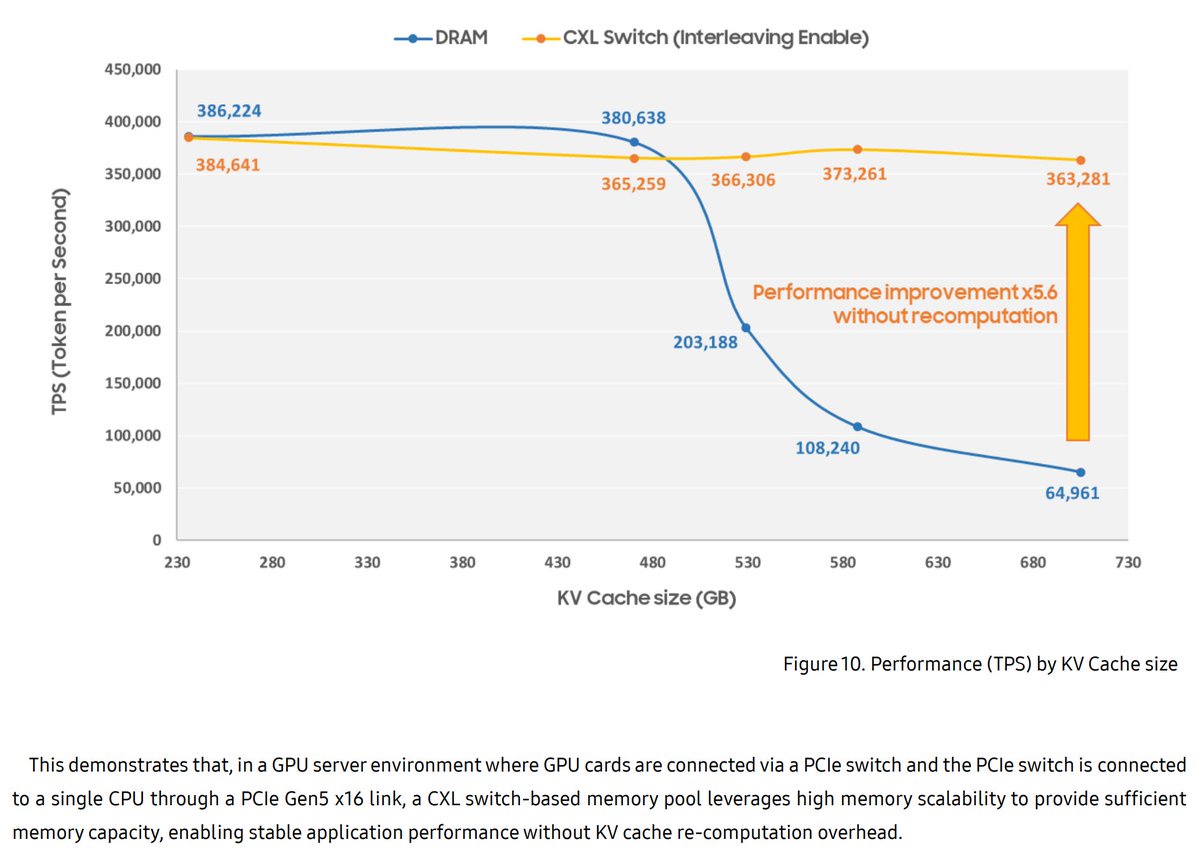

Samsung published their research on solving KV Cache scaling challenges with CXL-based memory pooling.

Question: Can a CXL memory pool support large-scale KV Cache offloading while maintaining performance comparable to DRAM?Evaluation: CXL memory pooling can deliver both near-DRAM performance and substantial memory scalability for AI inference workloads. Therefore, a CXL memory-based pool can be effectively utilized as a memory expansion solution for KV cache offloading.I would highly recommend reading Samsung's paper for more info on the specific system configurations used, and various performance evaluations.P

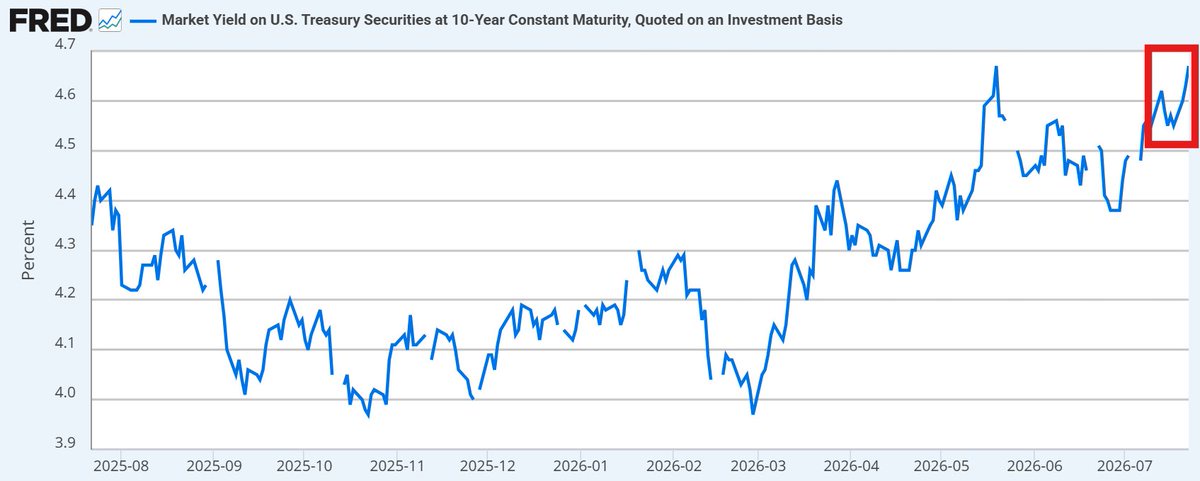

Macro uncertainty is what's driving semis equities right now.

More than hyperscaler capex forecasts and other earnings releases.The Fed's policy meeting next week could lead to a hawkish surprise, which is resulting in institutional investors playing things cautiously at the moment. Ongoing US/Iran escalations -> rising oil prices -> prolonged inflation -> potential rate hike.- Brent crude up 35% in three weeks- US 10Y yield set for its biggest weekly increase since early May- Fed funds futures traders now price in a 36% chance of a rate hike decision next week by the Fed (up from just 13% last week) So ultimately, the prolonged war is having a negative second-order impact on semis. Which is why all your favourite names - from $Nebius(NBIS.US) to $Sandisk(SNDK.US) to $Applied Optoelectronics(AAOI.US) - are all moving in lockstep regardless of their individual sub-sector or any sort of business fundamentals.Another example is $Intel(INTC.US) erasing all it's post-market gains today after reporting solid earnings yesterday. That would not happen under any sort of clear/stable macro conditions.Business fundamentals for the semis will certainly superceed all macro uncertainty in the long-run.

P

There is unprecedented demand for compute.

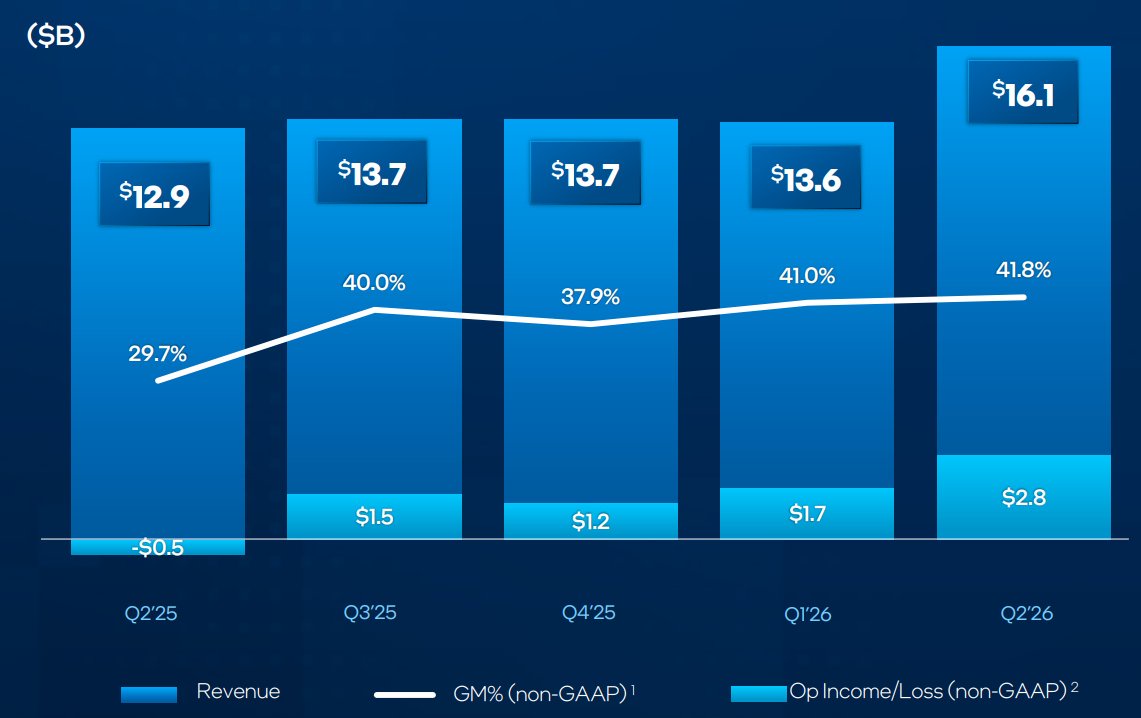

Very good $Intel(INTC.US) Q2 earnings, as expected: “Our Q2 results represent our strongest revenue growth in more than fifteen years.”- Revenues: $16.1B vs. $14.45B expected (beat by 12% and up 25% YoY) - EPS: $0.42 vs. $0.22 expected (beat by 91% and up 520% YoY)Q2 revenue by segment:- Client Computing and Physical AI revenue: $8.9B (up 13% YoY)- Data Center and AI: $6.3B (up 59% YoY)- Intel Foundry: $5.8B and the business advancing process technology including Intel 18A-P entering risk production.- AI driven demand accelerating- Intel Foundry: Improved yields and cycle time driving supply upside- Intel Foundry: Expanding across all nodes to meet strong demandQ3 revenue guidance of $15.8B-16.8B.As Intel “meaningfully increasing our investments in equipment, clean room space, and substrates.”

P

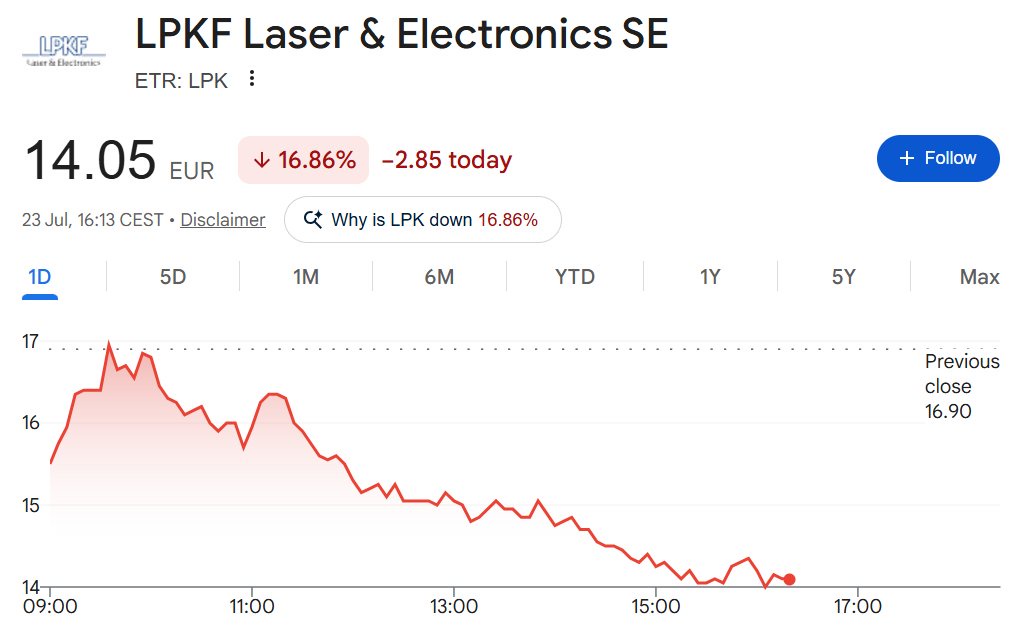

Just some thoughts on LPKF Laser / $LPK / $LPKFF earnings:

If you just look at H1 financials, it's pretty ugly:- Revenue fell 38.3% to €36.5M- Adjusted EBIT swung to -€10.4M- FCF at -€11.5M- Cash fell to €4.0m from €10.0m at end-2025But it's a little more nuanced than just the financials:It's all about volume ramp commentary with $LPK and whether they stick to their H2 2026 claims from earlier in the year:1. "2026 is the positioning year"The CEO reframed 2026 as positioning, with the ramp in 2027-28. With first ramp-up orders being placed in H2 2026, which is something they mentioned last quarter also.Q2 added a LIDE system order from a "leading specialty-glass manufacturer" and one from Penn State University. Positive read-through imo because a glass maker tuning its materials to $LPK's structuring process presumes $LPK's relative dominance even though the orders are small.2. TAM$LPK tripled their 2030 TAM estimates from ~€500M to ~€1.7B.Attributing the jump to AI-driven HPC wafer start growth + a broadened portfolio spanning glass structuring, package singulation and glass-to-glass bonding.Seems pretty wild to 3x your TAM, not sure if it's accurate lol.But seems directionally defensible since $Taiwan Semiconductor(TSM.US) raised its own 2030 global semis forecast from around $1T to over $1.5T with AI/HPC expected to drive ~55% of that. Just feel like the $LPK number is more of a narrative lever which they self-calculated "on the basis of external studies and own analyses." Seems very convenient to raise your TAM so much while the stock is down over 50% in a month.3. CEO hedgeTo the CEO's credit, his letter warns that it would be "premature to conclude" a breakthrough or that $LPK is firmly established in the supply chain. Imo, that is the correct posture since nothing in the order book proves any sort of ramp up yet.Since, as mentioned, volume ramp for $LPK should come in H2 2026 in advance of glass core substrate volume production in 2027.4. Guidance confirms that H2 rampFY26 guidance of €105-120M revenue.The low end implies H2 revenue of roughly €68.5M against a backlog of just €34.7M, which is essentially a 2x step up on H1 with backlog covering only half. Again, just confirming what they've said last quarter and this quarter r.e. their H2 production orders increasing. I do however see some potential dilution risks due to only €4M cash.Not ideal timing exactly when the thesis inflects in the latter end of 2026...I don't think a raise into the ramp would be automatically bad though especially since the wider ecosystem corroborates the 2027 framing. - On 2 July, Samsung Electro-Mechanics signed an agreement to form a glass-core JV with Dongwoo FineChem. Full scale operation targeted for the second half of 2027. - On 6 July, JNTC signed a TGV commercialisation agreement with Toppan. CEO said the company is targeting mass production in 2027 and Toppan is itself partnered with $AMD(AMD.US) on advanced packaging. - SKC/Absolics mass production targeted 2027 - $Taiwan Semiconductor(TSM.US) CoPoS pilot line slated for 2027So I don't think that there's much basis right now to scepticism that the glass narrative is running out of steam before any orders have really even begun. So in terms of timelines: - H2 2026 first ramp orders- 2027 glass core mass production + first $LPK revenue conversion - 2028+ high volume and sustainable margins - CPO on glass post-2029? Which is rightly excluded from the €1.7B TAM given that CPO architectures remain relatively immature even as $Taiwan Semiconductor(TSM.US) COUPE begins its own ramp.

P

This Google earnings release makes all the fear in semis from the past month look hilariously stupid.

They will all print crazy earnings, from $Lumentum(LITE.US) to $Coherent Corp.(COHR.US) to $Sandisk(SNDK.US) to $Nebius(NBIS.US).- Cloud revenue growth is accelerating- Gemini 950M MAUs vs. 750M in Q1- Raise 2026 capex guidance to ~$200B from ~$185BDon't forget who held your hand through choppy waters, anon.P

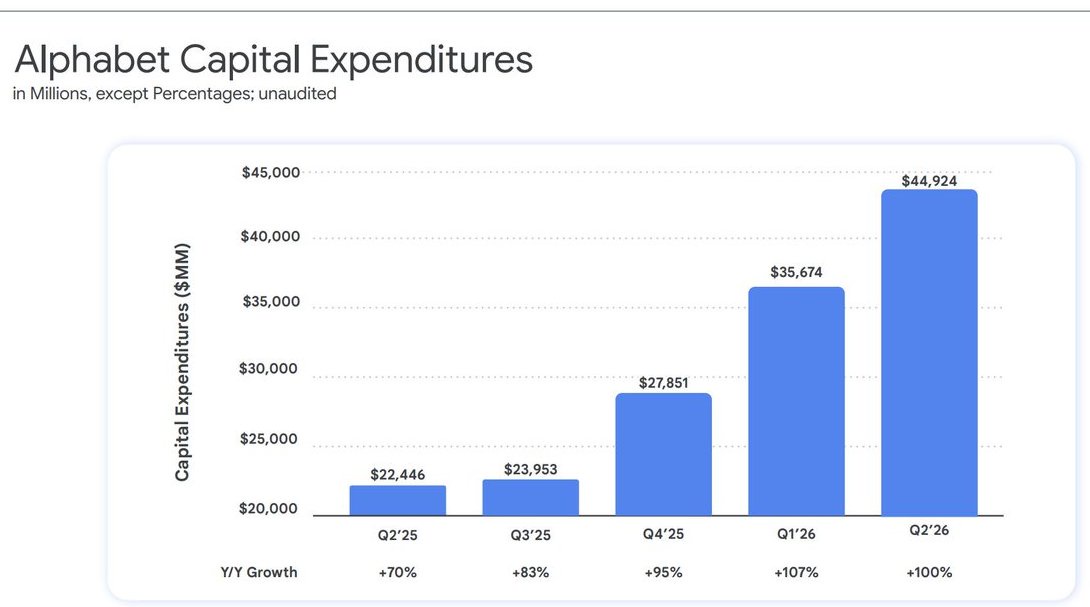

$Alphabet(GOOGL.US) upgrade 2026 capex guidance to $195B-$205B.

Up from previous estimate of $180B-$190B."We expect our capex to increase significantly in 2027"$300B capex in 2027...?

P

AI is not replacing $ServiceNow(NOW.US).

No credible CTO will offboard ServiceNow for a random AI solution with uncertain ROI.Q2 Earnings:- Subscription revenues: $3.9B (up 23% YoY)- Operating Margin: 30% vs. Est. 27%- EPS $0.90 vs. Est. $0.86Q3 Guidance:- Subscription revenue: $4.0B vs. Est. $4.1BP

There is no AI bubble.

Strong $Alphabet(GOOGL.US) Q2 Earnings:- Revenues: $119.8B vs. $117.0B (beat by 2% and up 24% YoY) - Google Cloud revenue: $24.8B (up 82%, accelerating from 63% last quarter)- Operating margin: 34% (expanded 2%)- EPS: $9.11 vs. $2.91 expected (beat by 213%)- Capex: $44.9B vs. $44.2B expected- Gemini 950M MAUsAccelerating cloud growth.....P

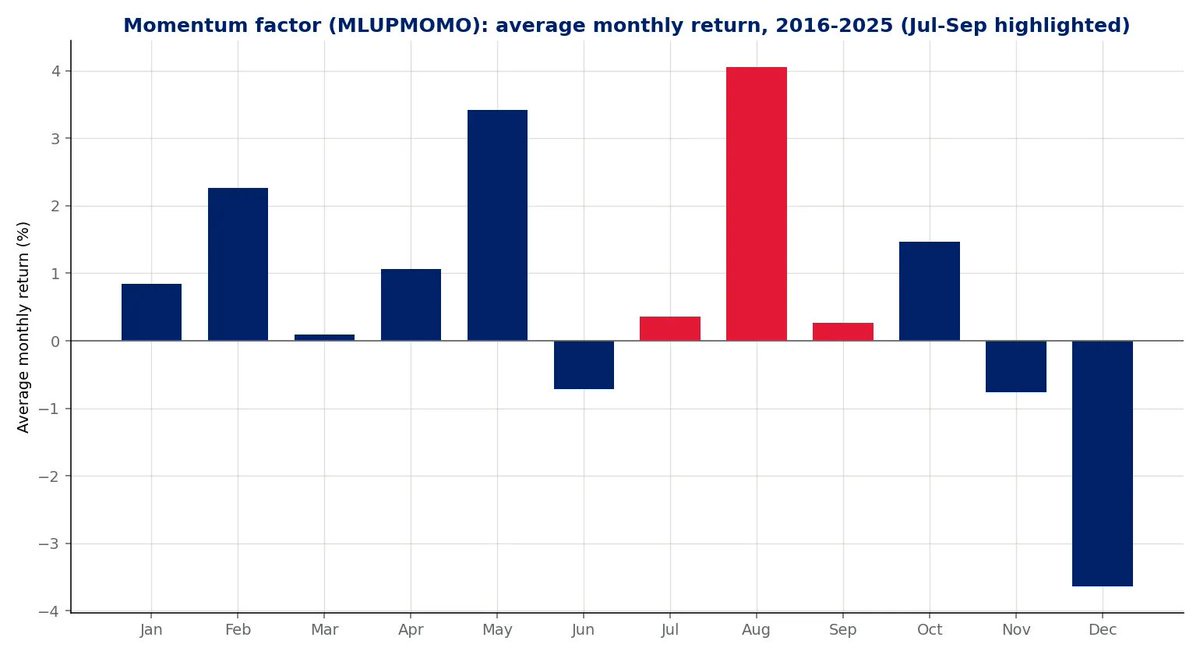

BofA & UBS are advising clients to buy AI momentum stocks:

BofA - August is historically the best month for their basket of momentum names such as $AMD(AMD.US), $Sandisk(SNDK.US) and $Micron Tech(MU.US).UBS - "Improving AI fundamentals are a signal to buy the dip."According to UBS' brokerage data, hedge funds have cut long positions in US semis by ~5% of gross market value (one of the biggest reductions on record).Which has resulted in net positioning in semis at Q1 levels, leading to both BofA and UBS positioning themselves as more bullish than earlier on. Probably because of the downside momentum unwind / profit taking easing up now.Cool to see institutional trading desks broadly align with retail sentiment on X.With many AI names now back at more compelling levels.

P

Tough to say if semis have bottomed now.

With most AI infra names having green days.- From $SIVE, $Aehr Test(AEHR.US), and $IQE up over 20%. - To $Sandisk(SNDK.US), $Micron Tech(MU.US) and $Applied Optoelectronics(AAOI.US) up over 10%.Regardless of today's returns, the next couple of weeks will certainly be more important for more clarity:- 22 Jul: $Alphabet(GOOGL.US) Q2: first proper gauge of the ~$750B hyperscaler capex year.- 22-23 Jul: $AMD(AMD.US) Advancing AI event: Roadmap read through for foundry loading + advanced packaging + laser type demand into 2027.- 23 Jul: $Intel(INTC.US) Q2: 18A yields + foundry commitments are probably the main variables w/ reads on US onshoring & packaging momentum.- 23 Jul: $IBM(IBM.US) Q2: already lost a ~25% of its MC so let's see how brutal the market is on guidance misses.- 24 Jul: 10% global tariff expires & new tariffs on dozens of countries expected. It'd be a stagflationary factor that feeds the overarching Fed hike narrative.- 27 Jul: Kimi K3 full weights released- 28-29 Jul FOMC: rate hold expected per experts + Polymarket. Important to bear in mind that rate hikes (or signals of one) would be the AI trade's first genuine regime shift.- 29-30 Jul: $Meta Platforms(META.US), $Microsoft(MSFT.US), $Amazon(AMZN.US) earnings: more capex datapoints.- 30 Jul: June core PCEAnd any day we could get a US-Iran ceasefire. There's still a 10 day proposal on the table while strikes keep happening. A proper/confirmed truce would help oil prices and helps semis.Just for a high level timeline of the "main" important events coming up soon.All have some kind of impact on semis to varying degrees. AI capex of course will be most important when the hyperscalers report earnings.

P

Memory market update:

- Counterpoint forecast a 20% QoQ increase for DRAM.- Trendforce are more conservative at 13-18% for conventional DRAM and 10-15% for NAND. - Morgan Stanley raised Q3 PC DRAM forecast to 15-20% increases QoQ from 3-8%.These aren't perfectly comparable baskets but the main conclusion is that tightness still persists.SK Hynix CEO and Chairman both confirmed supply tightness post-US IPO, potentially into the 2030s.- Samsung is reportedly seeking a Q3 DRAM ASP increase of up to 20% QoQ, with LPDDR increases potentially exceeding 20%.That would be their third consecutive quarterly hike after +90% in Q1 and +60% in Q2. This is above TrendForce's forecast but if price increases stick, $Micron Tech(MU.US) and SK hynix would likely follow.- TrendForce expects Q3 server DRAM contract prices to rise 13-18%. Multi year supply agreements limit price increases for some large volume US cloud customers. Which means customers without LTAs and incremental volumes sold outside those agreements would absorb the largest hikes. - SK hynix reportedly plan to scrap price caps in its new LTAs so that spot upside flows straight through, while $Micron Tech(MU.US)'s SCAs carry floors and ceilings.- TrendForce estimates HBM will consume 22% of the top three suppliers' DRAM wafer input in 2026 while producing only 9% of DRAM bits. Those figures rise to 30% & 13% in 2027. This disproportionate wafer consumption is the main structural reason why conventional / server DRAM can remain scarce, even as capex increases. - On HBM4 itself, 2027 contract negotiations land around Q4'26 and Digitimes model HBM4 moving from ~$2/Gb in 2H26 toward $4-5/Gb next year.- Morgan Stanley suggest NAND remains undersupplied through 2027.- TrendForce expects mature SLC NAND pricing to rise 120-170% in 2H26, driven by shrinking mature-node capacity & MLC -> SLC migration. Positive read-through for $Sandisk(SNDK.US), Kioxia and $Micron Tech(MU.US), while $Silicon Motion Tech(SIMO.US) offers controller leverage.- Worth noting Kioxia has filed for a US ADS listing, and $Sandisk(SNDK.US) has raised NAND product pricing double digits while extending the JV with Kioxia to 2034.- $Micron Tech(MU.US) also recently broke ground on a ¥1.5 trillion Hiroshima expansion, targeting advanced DRAM & HBM shipments around summer 2028.

P

$Nebius(NBIS.US) will become a "hyperscaler" very soon:

Via two axes:1. Cost of capital2. Cost per tokenEverything else about a hyperscaler is downstream of those two variables.Looking at cost of capital alone:- Neoclouds are basically a spread business where they raise capital at one rate + earn a contracted return above it.- Most neoclouds fund expansion via equity (v. expensive) and enter into a loop of dilute -> deploy -> depreciate -> repeat.- Nebius's new $775M debt facility from last week breaks that loop. - Their debt facility is collateralised against contracted cash flows from an "investment-grade" customer, so the lenders are essentially pricing off $Meta Platforms(META.US) / $Microsoft(MSFT.US) receivables rather than Nebius's own credit.- That's v. bullish for Nebius if lenders price them in that way. Especially since early GPU collateralised neocloud debt was at double-digit rates.- The structure repeats. Management says it will replicate the facility against >$40 billion of contracted backlog.- Every new "investment-grade" contract therefore becomes a collateral factory and not just revenue. It manufactures cheap borrowing capacity -> which funds capacity -> which wins contracts.- Customers also pre-fund the machine: deferred rev rose $3.2B in Q1, driving $2.3B of op. cash flow on $399M of revenue. - Ofc that's a delivery obligation and not free money. But it's an obligation funded interest-free vs funding the same buildout w/ debt.Despite what Burry will say, this isn't financing circularity:- $NVIDIA(NVDA.US) $2B equity stake is a rounding error against a broader $20B+ capex programme. - And the backlog is cash contracts paid out of $Meta Platforms(META.US) / $Microsoft(MSFT.US) opco's and not roundtripped semis money.This "new" loop is essentially how AWS became AWS where they funded at bond rates while everyone else funded at much higher equity rates for like 15 years.P

The deadliest mountain in the world is K2 in Pakistan.

But how deadly will the new K3 model by Moonshot be?In my view, this is not another "DeepSeek" moment. Kimi K3 is net-positive for the AI trade and compute demand, while being a net-negative for Western fronteir labs.After reading many reviews on X, my understanding is that Moonshot are just a few months behind the fronteir, rather than a full generation behind. I will caveat that I am far from being an AI "expert". However, I believe I understand the commercials at a high enough level to comment on and summarize.So from a commercial point of view, K3 comes out at roughly half the cost of Opus 4.8 for a slightly better model overall. Moonshot is charging ~$3 per million input tokens and ~$15 per million output tokens, the same rate card as Anthropic's mid-tier Sonnet and nearly 4x its own previous model.In my opinion, these pricing dynamics are what makes the DeepSeek comparisons I've seen on X to be very lazy. DeepSeek in Jan 2025 was a deflation event where they had near frontier capability built very cheaply and effectively given away at such low prices which implied that Western AI capex was excessive. Moonshot is doing the opposite. It's charging Western prices because it believes it is selling capability, not cheapness, most likely because Chinese labs are starving for compute and actually need the revenue to continue building and serving demand. The business model for fronteir labs like OpenAI and Anthropic is essentially the monetisation gap between their own leading models and everyone elses. Both of those companies are raising money at valuations that assume that gap stays wide and highly monetisable for years to come (at growing rates).However, many AI experts on X say that the Kimi K3 gap can now be measured in months, and that the tier just below the frontier, where the bulk of real commercial workloads actually run, is potentially about to be served up at very low commodity prices. As a result, the labs' defensible ground shrinks to the true frontier, to enterprise trust and security, and to distribution. Revenue can keep growing while pricing power erodes, and in my view, it is the pricing assumption (not the demand assumption) that carries Anthropic's and OpenAI's lofty valuations.Using SoftBank as a proxy for OpenAI, we saw today that their stock price fell a huge 9% after Kimi K3 was released. I believe, now, that this valuation-digest was and is warranted. I know many of my followers will care about the AI trade in upstream names though. However, I do not view the latest Kimi K3 model as having a fundamentally negative impact on those companies. Every K3 token will still consume chips, memory and power that remain effectively sold out into next year. Moonshot will certainly need to secure additional compute to facilitate growing demand for their models. As of right now, it does seem like exposure to model-layer margins, lab valuations and their listed proxies looks worse.Conversely, exposure to the infra in upstream supply chain names that serves tokens regardless of whose model wins looks cheaper, all things considered, for no fundamental reason.However....to be slightly more contrarian - you could argue that if cheaper Chinese models come to market at a rate of knots and leads to margin compression for the likes of OpenAI and Anthropic ---> will that not have a negative effect on their spend in the long-term? As a result, a negative effect on the upstream AI supply chain?I am yet to think through this in much detail, but it certainly deserves exploring. I want to finally mention some of the technical experts I have enjoyed reading since Kimi K3 came out, as a non-technical person:- @zephyr_z9 - @scaling01 - @FundaAI If you want to be someone who is constantly learning about AI, these guys are must-follows in my opinion.Of course, as always, I would encourage anyone to correct me or debate me if I am wrong in any area.P

Oof, $SpaceX(SPCX.US) Starship launch aborted just now.

Per Elon: "Next launch attempt hopefully in a few days."Just highlights how risky the space business is.Goes hand in hand with stock price volatility across the entire sector.P

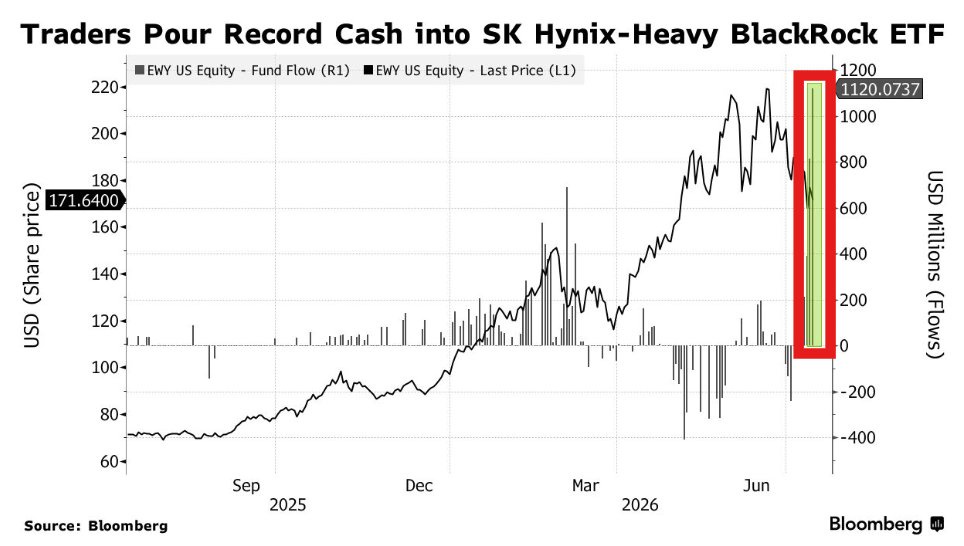

Appetite for the memory trade is still super high:

Record inflows for the South Korea ETF $EWY this week.Tuesday: $814 million (previous record high)Wednesday: $1.1 billion (new record high)Investors are back to using $EWY as a proxy for the South Korea SK Hynix listing, just like in Q1.Rather than paying the ~25% premiums for the US listed SK Hynix ADR.And for added context on the demand for memory stocks:The memory ETF $DRAM is currently at record-high AUM levels at ~$25 billion, despite only being released three months ago.P

AI and semiconductor names are down significantly over the past couple of weeks.

However, what matters right now is for me to provide some useful context and "advice" on constructing your own investment philosophy.There's no better time to learn about yourself than when times are rough.Personally, my portfolio has taken a huge hit for a few reasons. Primarily because I pivoted around this time last year from a slightly more diversified base of stable technology compounders into a slightly higher concentration of higher beta and smaller market cap AI names.However, if you're an inexperienced investor, what I can tell you is that market drawdowns are normal and expected (even though we can never time them exactly).So if you plan to invest for decades, you should certainly expect to sit through many bear markets and many corrections.The first thing to internalise is the arithmetic of losses where a 20% loss needs a 25% gain to get back to even. Similarly, a 50% loss needs a 100% gain to recover your losses. This is why position sizing matters just as much as stock picking, and is a key reason why I'm against risky tools such as options or leverage for *most* investors. Your primary goal when playing this game is to keep playing. A blown-up account via excessive leverage or backfired options trading is the worst case scenario, no matter how attractive or easy "gurus" online might make it seem. That said, I do firmly believe in running a concentrated book of high conviction names that you can reliably track daily.The specific number of positions varies person to person depending on a few factors like your individual ability to keep on top of latest events for each holding, including second and third order effects from other company's news.However, every legendary investor's track record was built on a handful of high conviction positions. Sure, spreading capital across many names you barely understand can in theory reduce risk just because of the law of large numbers.But in my opinion (and experience), it just guarantees mediocrity. That said, concentration is a discipline of its own and is something I could write books on. With the aim of keeping thing consise, concentration only works if you can name, very precisely, what you're concentrated in.In simple terms: have you researched the company, sector and market to the point where you have utmost confidence in the trade?But with concentration, you *need* diamond hands if all things are equal with the company and nothing has changed. For example, $NVIDIA(NVDA.US) fell more than 50% in 2018 and ~65% in 2022. Anyone who capitulated in Oct 2022 sold one of the greatest companies of all time, probably because they lacked conviction in the trade.And in turn, did not have any sort of investment philosophy.So, you need to really sit down and talk to yourself right now, during this current AI drawdown, and ask yourself what your investment philosophy is.You could probably run the exercise with Claude or ChatGPT and get some pretty enlightening outcomes for yourself.But you must be honest for the good of your future self. There's no better time to learn what kind of investor you are than during red days and weeks.P

$IQE has unfortunately not been performing well recently.

However, we've only had net-positive news since May:- $Tower Semicon(TSEM.US) multi year InP epiwafer agreement in June w/ minimum purchase commitments from year two- $14M multi year PO from a "strategic global technology leader" for AI/datacentre applications this week- $Macom Tech(MTSI.US) board involvement after anchoring a £81M raise to strengthen balance sheetThat said, it does seem like IQE is simply resetting (similar to other high beta names like $SIVE) after going up parabolically in a few months.And Chinese export curbs on gallium + InP feedstock are inflating input costs with management also saying that they're sharing that pain with customers. I'm also looking at the fact that their balance sheet almost ruined them a few years ago - which is now solved thanks to £45M from MACOM as a strategic investor tied to LTAs. IQE is one of the only Western epi houses that can supply InP epiwafers at a scale that actually matters.And InP sits under every optical interconnect going into datacentres. Tower didn't sign a multi year supply deal and settle a long standing patent dispute in the process because it had alternative routes to source supply...So currently, you've got:1. A repaired balance sheet.2. An anchored strategic partner w/ Macom. 3. Contracted InP volumes.4. An option on photonics too.However, risks are definitely real and please do not act on my words alone...They've had execution issues in the past e.g. too much internal resource in their wireless segment which has been dying a slow death over the past couple years. (They're correcting that now just by going from their investor decks).Plus of course a long dilution history. And China risks impacting input costs.Drawdowns like the one we're in currently are all part of the game. Where highly volatile businesses = highly volatile returns.P

HUGE $Nebius(NBIS.US) news today, showcasing why they're the premier neocloud:

-> Nebius announces a new business model that lets infrastructure partners deploy Nebius’s AI cloud platform in their own AI data centers.This is so f*cking good.Simply:- Nebius will let partners (e.g. DC developers, infra funds, sovereign AI projects) build + pay for data centres.- Then pair that partner capacity with Nebius's systems, software stackm and customer book. - Meaning that Nebius can expand their capacity "pool" even faster.- With no capex or financing risks like debt/dilution.Also, for Nebius: they get a very high margin rev stream w/ minimal financing requirements.Since the partners will fund all the expensive stuff like the actual building / power / GPUs. And then Nebius supplies genuinely scarce stuff like systems architecture / $NVIDIA(NVDA.US) supply chain access / software stack. And ofc, the GTM strategy w/ access to Nebius's customers.Meaning that Nebius would sell a partner's DC capacity via their own in-house Nebius sales org. With identical service levels to their owned sites.Then, Nebius takes a revenue cut / licensing fees / commissions / committed capacity deals.Unbelievable from Nebius lol.Nebius sells out capacity every quarter and sits on ~$46B of contracted backlog (mainly $Microsoft(MSFT.US) and $Meta Platforms(META.US)).So their main constraint is nothing to do with customers or tech. Rather, their limiting factor has been capital + energized power where every GW costs upwards of billions of dollars. But...this announcement removes the capital constraints to crazy high expansion.P

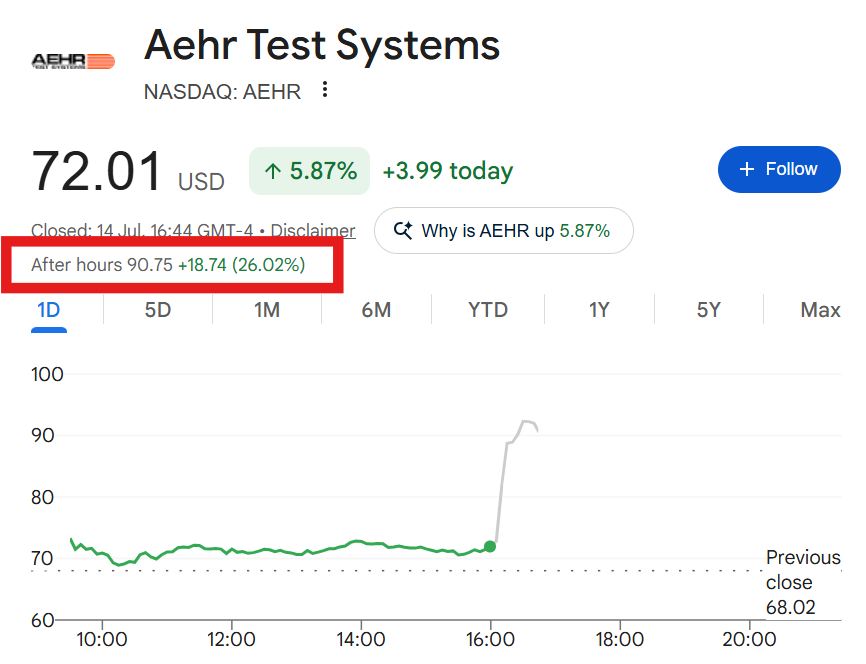

Wow, unreal $Aehr Test(AEHR.US) Q4 earnings and FY2027 outlook, +26% after-hours.

I have high conviction that Aehr is well positioned for many years of very strong growth:- Multiple customers entering/expanding production- Huge backlog- Opportunities in new markets e.g. NAND and HBM applications for their WLBI system roadmap.-> Q4 2026 earnings:Revenue: $18.8M vs. Est. $18.7MEPS: $0.11 vs. Est. ($0.01)Bookings: $61MBacklog: $101M-> FY27 Guidance:Revenue: up to $150M vs. Est. $85M (+200% YoY)- WLBI demand from AI applications is expected to accelerate.- AEHR also engaged with additional AI processor suppliers that are evaluating WLBI to improve product reliability and reduce yield loss from production burn-in.With qualification testing for their WLBI exceeding all of their major customers' expecations. With their major customers ultimately saying that they want to buy even more systems from Aehr."The potential revenue opportunity from any one of these devices is significant to Aehr in terms of near and long-term revenue streams related to the WLBI systems."Then on their package-level burn-in systems:- Record follow-on orders recently from Aehr's lead hyperscale customer.- Customer wants to buy more PLBI systems.- Aehr also engaged w/ multiple new customers for PLBI qualification incl. AI customers and robotics. So overall, very significant TAM expansion if they can capture new customers across AI and robotics. And since they pass qualification cycles with ease, I have high confidence that they'll capture these newer markets also, driven by years and years of in-house process knowledge + patents.I've mentioned a few times, but Aehr's lead SiPho customer is also ramping w/ follow-on orders over the last year. And more orders coming soon from them for additional WLBI systems. "Our newest major silicon photonics customer...has provided us a forecast for additional systems this calendar year as it ramps capacity to support next-generation hyperscale data center deployments."All basically meaning that SiPho + optical test and burn-in market has huge potential to grow significantly and be a major long-term growth driver for Aehr.And very interesting to see the CEO mention the memory market roadmap for their WLBI systems also!"We continue to work with multiple memory suppliers to align our solutions to meet the production needs of these companies' new capacity coming online."Very exciting times for Aehr, and they remain one of my higher conviction names all throughout the AI supercycle.High demand for Aehr solutions + Great execution = BullishP

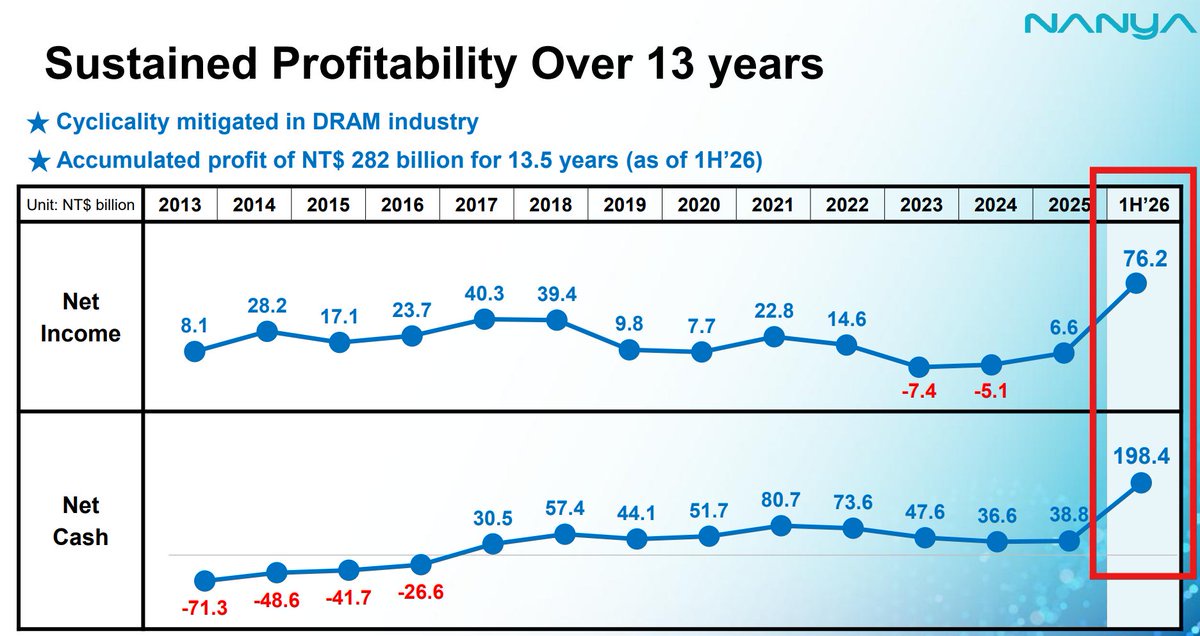

Nanya Q2 Earnings highlights:

Revenue: NT$82.5m (+68% QoQ)EBITDA: NT$63.8m (+93% QoQ)EBITDA Margin: 77.3% vs. 67.2% last QuarterBut of course, there's a lot of retail worry w/ the memory trade rn, mainly thanks to volatility with SK Hynix and Samsung.From Nanya, their DRAM market outlook/commentary looks like this:- AI driven structural change is mitigating memory market cyclicality.- Supply tightness is expected to persist over the next several quarters.- Multi-year LTAs aligning supply-demand expectations.Overall, aligned w/ SK Hynix CEO comments post-US IPO, confirming lack of supply for the forseeable future across the market. With Nanya, you do get some drag from legacy rev lines though like from smartphones/PCs/consumer elecs. Where AI is only ~20% of revenue rn which will be higher in the future.But they've confirmed that the structural shift towards AI is "intensifying memory shortages", shown by their shipments being flat for the quarter but ASPs increasing more than 60%. Which looks set to continue for the coming quarters with continued lack of supply since their new fab only starts ramping in 2028.P

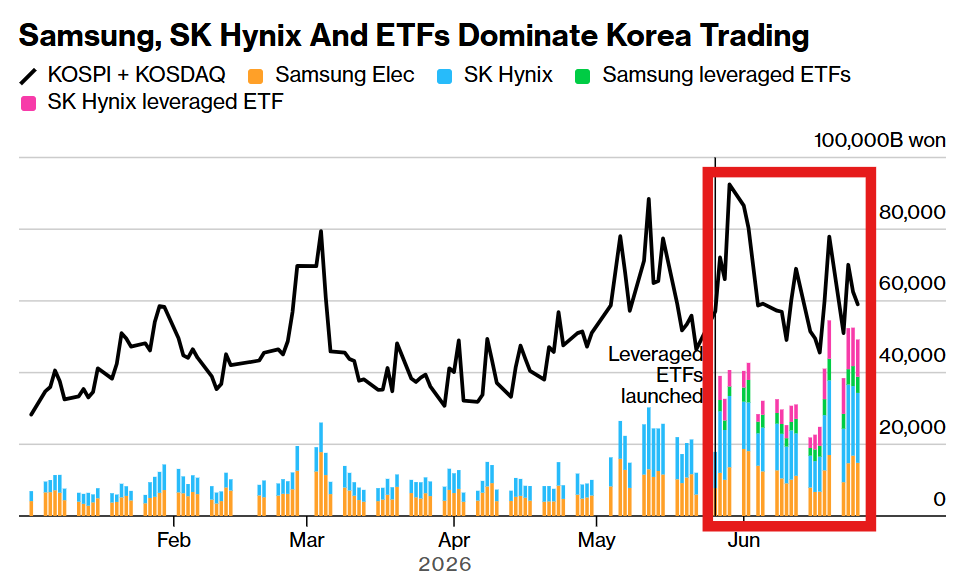

This is a shocking statistic:

SK Hynix & Samsung shares/leveraged ETFs make up over 70% of trading volume in South Korea.I think the memory concentration is rational.But over 70% of daily volumes with ~15-20% in leveraged ETFs just reeks of a gambling mindset.I can also guarantee that most of those "investors" don't know what SK Hynix do, and probably think that Samsung are going up cos of phones/TVs.Then there was that WSJ article a few weeks ago that interviewed people who full-ported their life savings into 2x leveraged SK Hynix.All paints a pretty stark picture around the state of Korean investment culture imo.P

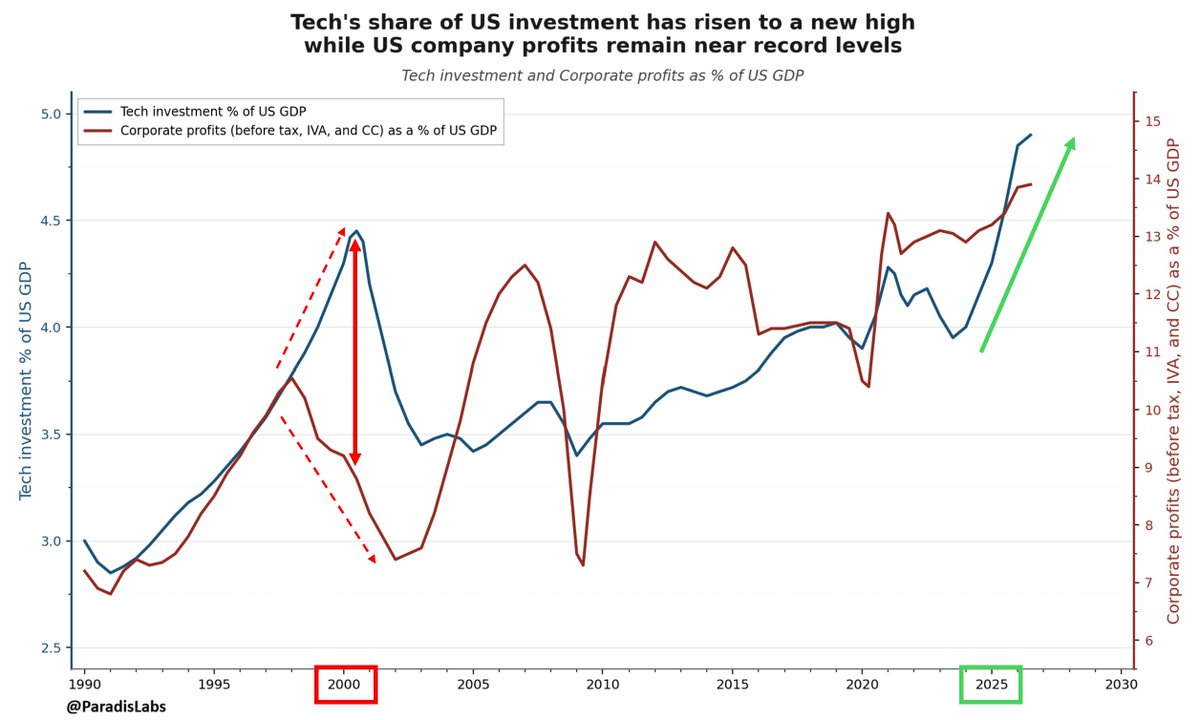

AI is not a bubble.

Lazy AI bears point to $NVIDIA(NVDA.US)'s market cap and through PTSD, claim it resembles $Cisco(CSCO.US) in March 2000.However, any useful bearish analysis should look at what actually made the 1990s market a bubble from a macro sense, and whether those conditions exist today.I now refer you to the attached chart.In the late 1990s the two lines veered apart. Tech investment went vertical toward ~4.5% of GDP, while the economy-wide profit share rolled over from its 1997 high and fell hard into 2000. Investment surged while profitability eroded...bubble!Today, the lines rise in tandem. Tech investment has pushed to roughly 4.9% of GDP, above the dotcom peak and climbing more steeply, while pre-tax corporate profits sit near 14% of GDP. Meanwhile leverage has (mostly) stayed contained and the US current account deficit is shrinking. However, bears point to record levels of investment in isolation, choosing to ignore the growing profitability in addition. Are they dumb, or are they ignorant?Probably both.In the run up to March 2000, share prices rose and multiples exploded. The market paid more and more for each dollar of invisible earnings. This time, forward P/Es have barely moved even as share prices rocketed, because earnings expectations rose alongside them. For example, the Nasdaq 100 trades around 23x forward earnings, near its own 10Y average versus ~60x in March 2000.But...but....the market is so concentrated!! 1! 1!Yes, the ten largest S&P 500 companies account for ~40% of the index, above the dotcom peak. But those ten companies contribute around 30% of total market earnings, compared to under 20% in 2000, and trade at roughly a 50% premium to the rest of the market against a premium north of 100% at the prior peak. Now, bears will say: "If the rally is earnings driven, everything depends on whether the earnings persist!"Correct.But unfortunately for the bears, this is where things get uncomfortable.AI type names have added on the order of $27 trillion in market value since late 2022, up from roughly $19 trillion just seven months earlier. Set that against any weak attempt to discount the additional profit streams AI can plausibly generate for US companies (estimates cluster in the trillions) and the market has capitalised a multiple of the realistic prize. Not all of that $27 trillion is AI (the hyperscalers run enormous non-AI businesses), and more aggressive assumptions on adoption and productivity can lift the number. But closing the gap requires increasingly heroic assumptions: - that recent shifts in earnings shares are highly persistent- that the boom's suppliers capture an outsized slice of AI's total economic gains- that the economy-wide profit share keeps climbing indefinitelyAlright, cool. But what about all the circular financing?!- Nvidia has committed tens of billions to OpenAI while remaining its primary chip supplier- OpenAI has signed a cloud commitment with $Oracle(ORCL.US) reported around $300B- Oracle in turn buys from Nvidia- $Microsoft(MSFT.US) is simultaneously OpenAI's largest investor and one of its largest vendorsTrue, this somewhat resembles the dotcom vendor financing where Cisco booked loans to cash stricken carriers as revenue (roughly a tenth of sales at the peak), much of it later written off. However, today's arrangements are mostly equity stakes in counterparties with genuinely fast growing revenue rather than disguised loans to fund purchases, and Nvidia has lately been unwinding parts of its ecosystem book.And according to analyst reports, even the AI labs like Anthropic have now turned profitable. A feat many thought would be impossible only a year ago.Personally, I treat this circularity as risk rather than a point to build a bear case around since it's all ultimately leading to greater earnings across the board. Even for fronteir labs. Shock!This then leaves the one key question:Will barriers to entry protect today's profits from erosion? This entirely depends on each company's position in the AI supply chain. - At the model layer, barriers are relatively fragile where frontier models will almost certainly converge longer-term, and open source alternatives have the ability to reset price floors. However, AI soverignty will ultimately result in the likes of OpenAI/Anthropic winning.- At the hyperscaler layer, $Amazon(AMZN.US), $Alphabet(GOOGL.US), $Meta Platforms(META.US), and $Microsoft(MSFT.US) are set to spend (currently) $750B for 2026 AI capex where falling behind is not an option. These companies are led by people smarter than you or I - do you think they'll risk their entire business collapsing for AI? No. In fact, you can already see that AI is boosting their earnings measurably in recent earnings.- Going further down, you've got irreplaceable companies such as $ASML(ASML.US) (EUV machines), $Taiwan Semiconductor(TSM.US) (CoWoS packaging), and HBM with $Micron Tech(MU.US), SK Hynix and Samsung who are gated by long qualification cycles and multi year LTAs where demand > supply up to the 2030's.The risk of a 2000 style valuation bubble is massively lower than the bearish consensus believes.The world is revolving around AI, and that'll continue for the forseeable future.