Kuaishou core revenue only +3% but Kling AI +300%. the base business is mature but the AI product is growing fast enough to shift the revenue mix. if Kling can compound to USD 2B+ ARR by 2027, the val......

Kuaishou Q1: overall revenue +3%, Kling AI +300%, annualized ARR approaching USD 500M. this is the classic "mature core, high-growth satellite" structure. the short video business funds the AI moonsho...

Kling AI going from zero to near USD 500M annualised ARR while nobody was watching. Chinese generative AI is not just catching up, it's monetising at a speed that's genuinely surprising. adding $KUAIS......

I've been dismissing Kuaishou as a slow-growth short-video also-ran for a year and they quietly built an AI video product doing USD 500M ARR. I was very wrong, lah 😶🌫️

The following is Dolphin Research's Trans of the $Kuaishou-W(01024.HK) 1Q26 earnings call. For our earnings analysis, cf. 'Kuaishou: Comeback rides on Keling'.

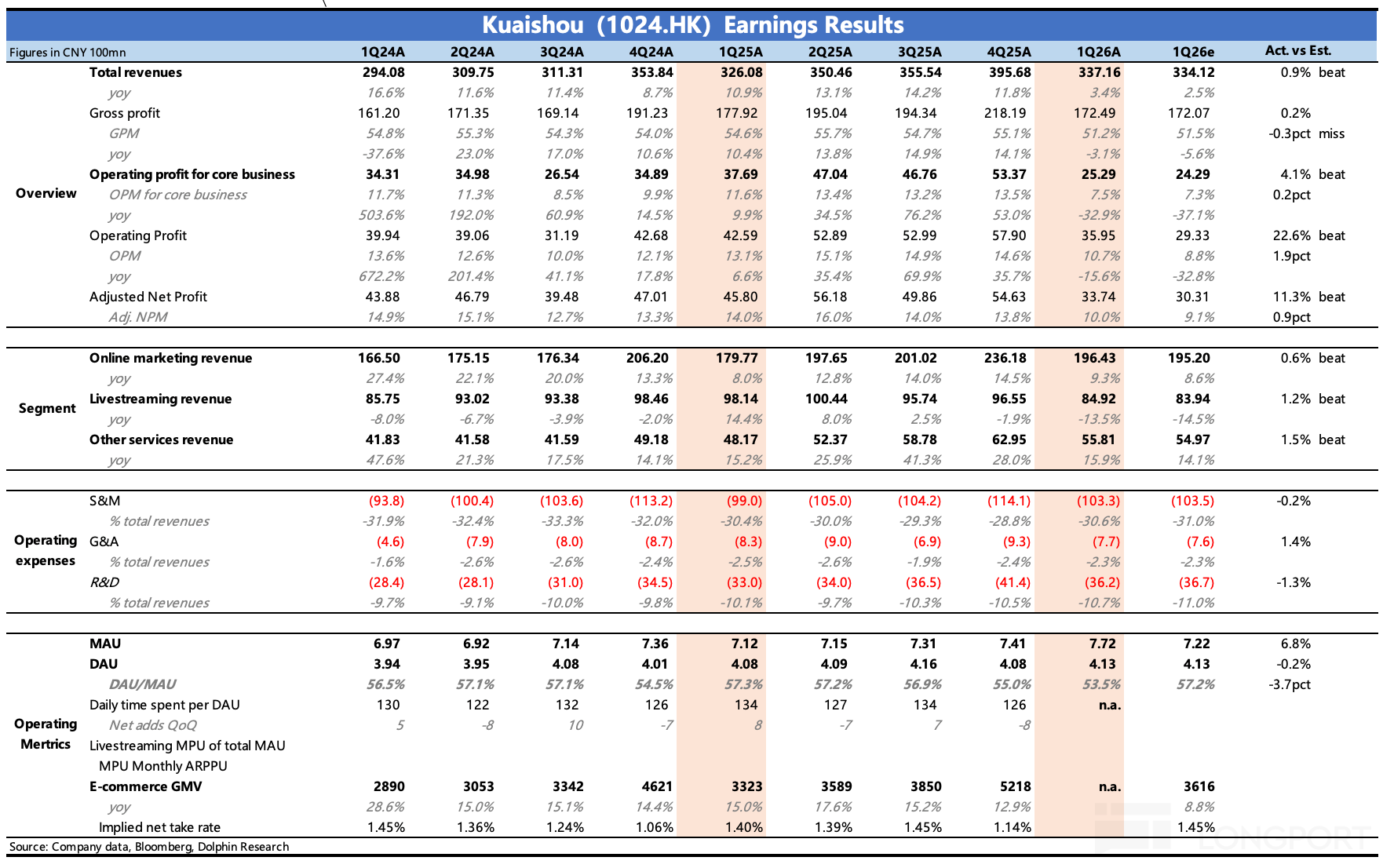

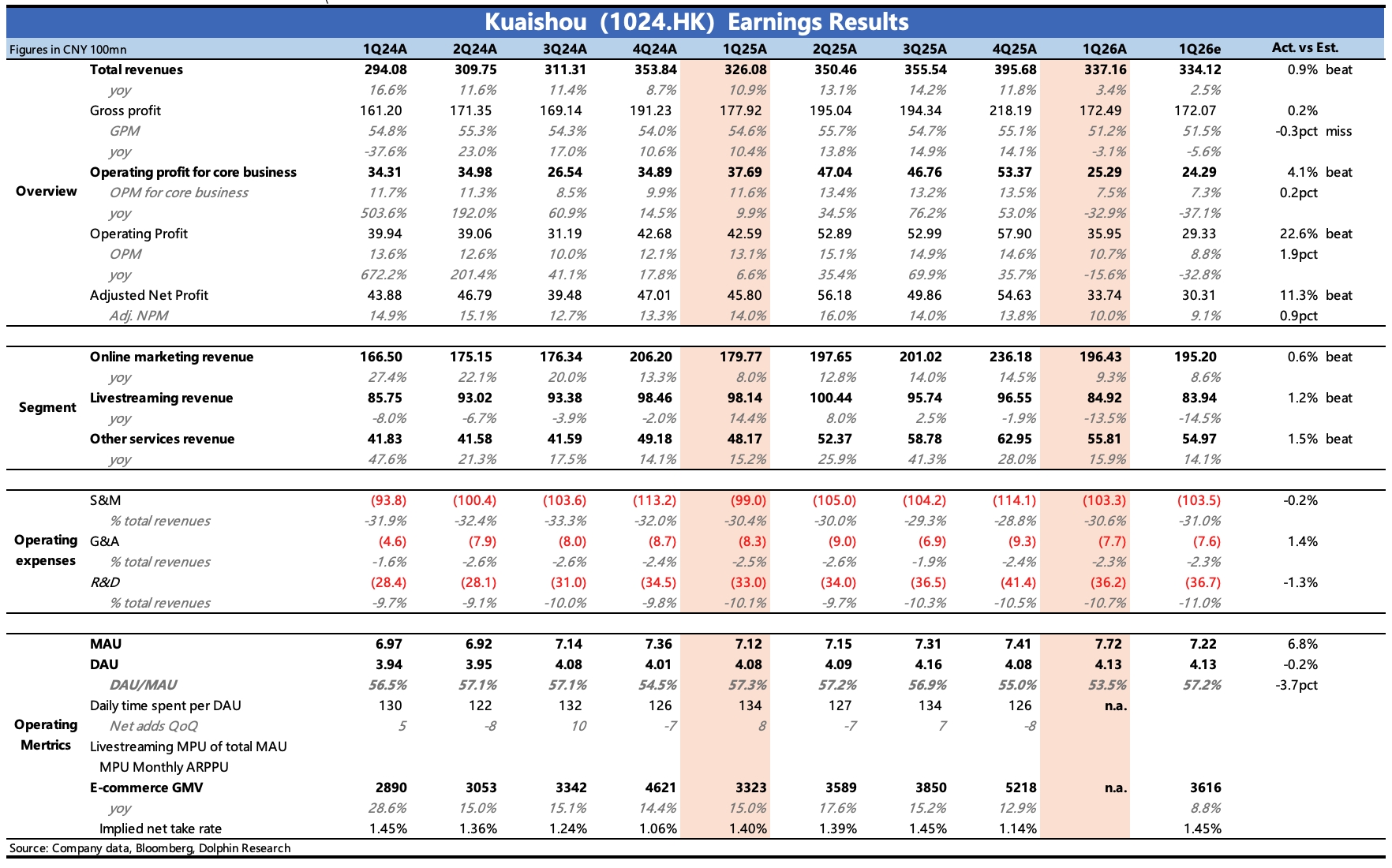

I. Key earnings highlights recap1) Shareh...

$KUAISHOU-W(01024.HK) released its Q1 results after the Hong Kong close on May 27 (Beijing time). Overall, the quarter was broadly in line. The operating profit beat was driven by non-core other gains...

......

+6

AI memory demand likely is a real multi-year super cycle driven by AI growth, but markets have already priced in much of the optimism, leaving mixed upside.

Kuaishou 1Q26 First Take: Results were broadly in line; the OP beat was mainly driven by other income unrelated to the core biz., which is not sustainable.

1) Revenue was RMB 33.7bn, up 3.4% YoY. This...

Two of China's biggest consumer platforms drop Q1 2026 results today. PDD Holdings (Nasdaq: PDD) and Kuaishou (HKEX: $KUAISHOU-W(1024.HK)) are heading into very different earnings fights. Here's what ...

the world's top 3 semicon memory heavyweights: SK hynix, Samsung elec & micron. SK share price returns at 800% in a year so Micron has to catch up.