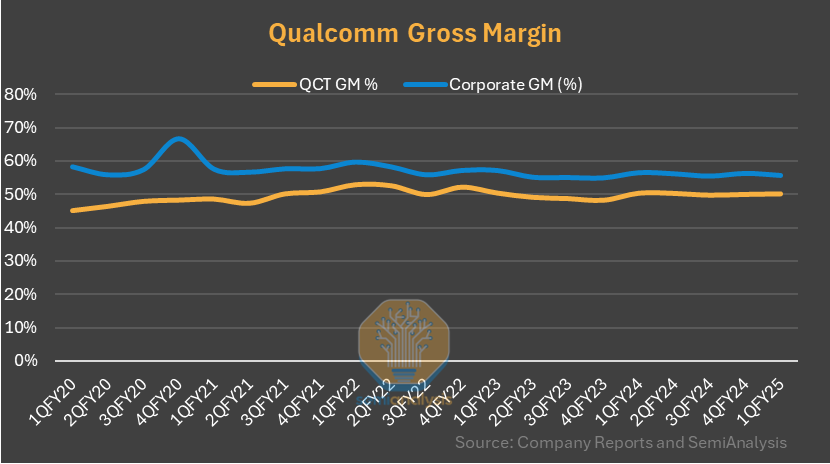

Qualcomm's chip division QCT has below corporate gross margins and barely have 50% GM. This is below Intel, NVIDIA etc. product GM. Despite its lower GM, it brings >2x higher EBT than licensing division. Premium tier gains didn't move chip GM much and there seems less room for GM expansion in smartphone. Non-smartphone chips might improve but still too small.

Source: Sravan Kundojjala

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.