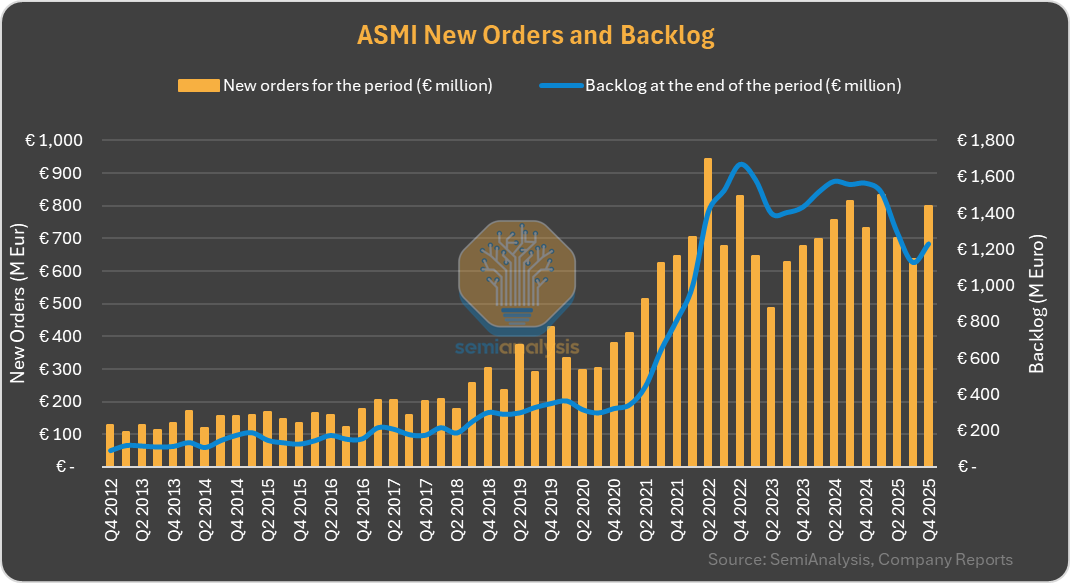

ASMI QDec25 revenue up 8% higher vs guidance but down -13%q/q and -14% y/y to €698M. Upside was driven by advanced logic/foundry and spares. Orders up 26% q/q and backlog up 9%. Better than expected China drove order upside. CY25 revenue up 8% y/y to €3.2B. Original expectation for CY26 China to decline by DD% but with new orders China could be better in CY26.

Source: Sravan Kundojjala

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.