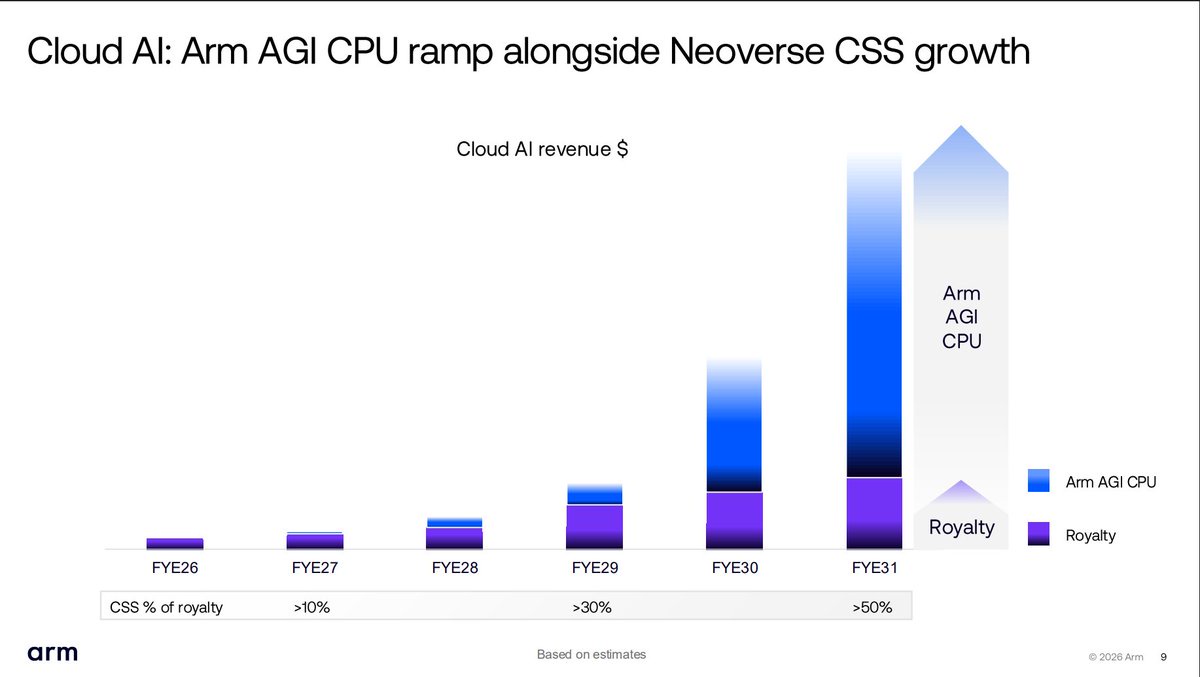

Arm's pivot to become a competitor to its customers may come at the expense of margins (from current 99% to 73% by FY31) but offers higher incremental revenue and gross profit. The ramp is stunning. FY28 $1B, FY29 $2B, FY30 $4B and FY31 $15B. ASP increases a factor too. Arm sees >55% margins on CPUs and implied upside on revenue. Rambus is probably close example of IP/product company and Rambus has >60% margins on product.

Source: Sravan Kundojjala

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.