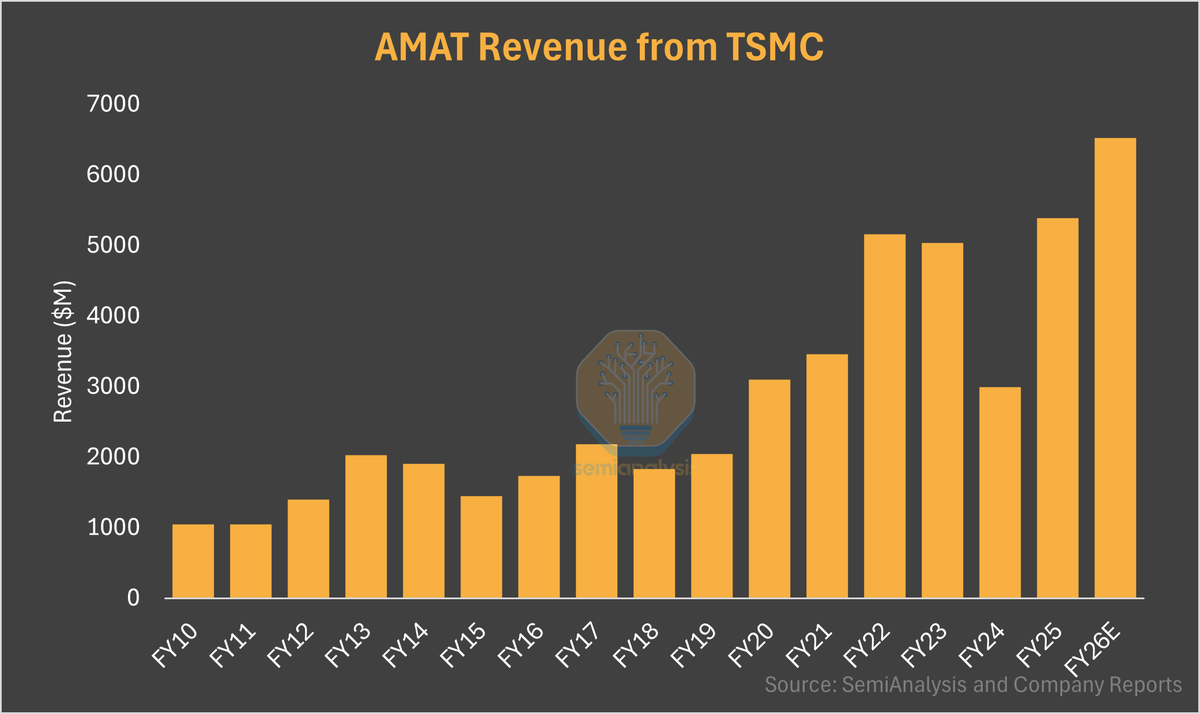

AMAT guided its semi equipment revenue will grow at least 20% in FY26. With China down, most of it has to come from leading-edge logic and DRAM/HBM. AMAT's TSMC revenue will likely see a good jump in FY26, driven by TSMC's capacity expansion across FinFET and GAA nodes. TSMC is an important customer (19%) for AMAT. Each cycle's trough is now higher than the prior cycle's peak. FY18 trough roughly flat vs FY13 peak. FY24 trough > FY17 peak.

Source: Sravan Kundojjala

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.