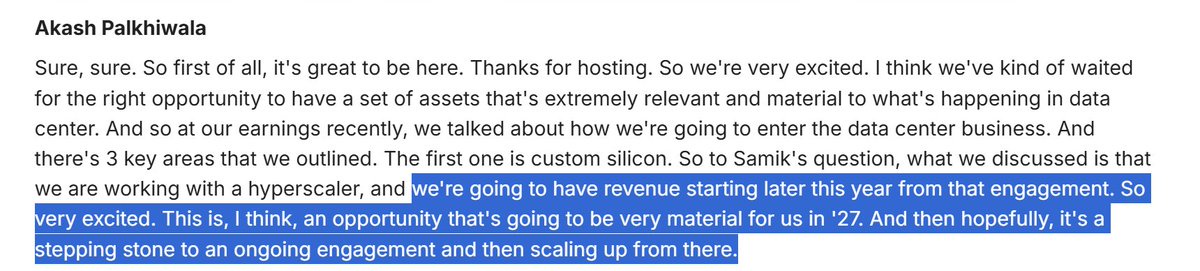

Qualcomm's elusive search for growth driver coming to an end. Custom silicon revenue kicks from 2HC26 and sees 'very material' revenue in '27. Broadcom and Marvell target competition. Layering on top of this, CPU and AI accelerator which will roll out from '27 and beyond. QCOM is ready to take lower GM to get into the DC space but sees OPM accretive opportunities. Wouldn't be surprised if QCOM's DC revenue overtakes handset revenue in a few years time if they follow-up with a strong roadmap. QCOM is also working with hyperscalers on personal intelligence devices, a well suited effort.

Source: Sravan Kundojjala

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.