Tesla accelerates mass production, Chinese manufacturers race ahead collectively—is the 'EV moment' for humanoid robots arriving?

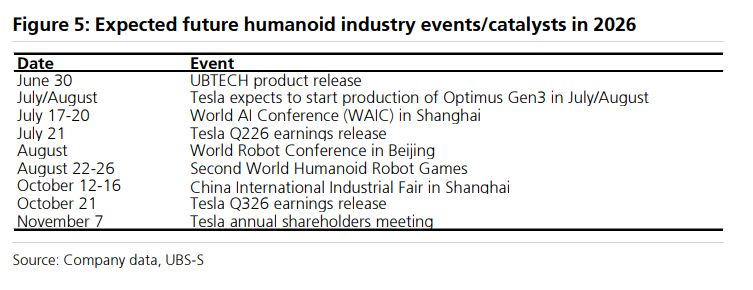

According to Nomura, Tesla is transitioning its Optimus Gen 3 from initial assembly into full-scale production, establishing the baseline for global manufacturing velocity. The company has adjusted its annualized capacity target for the Fremont facility (repurposed from the Model S/X production lines) upward to roughly 70,000 units. Furthermore, Tesla intends to build an additional 70,000 units of capacity in Austin by 2028, aiming for a long-term total capacity of 1.5 million units. Supply chain data indicates that 2026 Optimus shipments will reach approximately 25,000 units (+/- 10,000), with weekly production goals in September potentially rising to 1,000 units. UBS Group identifies the official rollout window for the Optimus Gen 3 between July and August, marking it as a pivotal market driver for the latter half of the year.Outside of China, manufacturers continue to trail domestic production speeds. Figure AI and Boston Dynamics are both tracking annual shipments of roughly 500 to 1,000 units, while other international builders are averaging 100 to 200 units. Notably, Figure’s BotQ line has publicly achieved a manufacturing takt time of one unit per hour.Nomura has upwardly revised its 2026 shipment forecast for Chinese humanoid robots to 40,000–50,000 units. This growth is propelled by intensified government procurement for embodied AI bases and a late-year consumer demand inflection point triggered by the introduction of cheaper models.Market share is distributed across distinct tiers:Tier 1 (Top 2 firms): Each shipped roughly 10,000 to 15,000 units (representing a 2x to 3x year-over-year increase).Tier 2: Several mid-tier companies shipped approximately 3,000 units each.Tier 3: Smaller players shipped between 500 and 1,000 units each.Downstream application allocations for 2026 shipments are structured as follows:Consumer Applications: 30%Performance & Entertainment: 30%Government Procurement (Data Collection): 20%Education: 15%Commercial & Industrial Applications: 3%–5%UBS Group notes that state policy is actively shifting the Chinese robotics industry from experimental showcases to practical operational deployment across industrial, logistics, healthcare, and residential environments. The Ministry of Industry and Information Technology (MIIT) intends to deploy more than 10,000 units across over 100 scenarios by late 2027, while the Shanghai municipal government targets 100,000 factory-deployed units by 2030.Investment Trends and Market DragStrategic capital activity in the global robotics sector intensified during the first half of 2026. Despite this momentum, overall market sentiment faces clear headwinds. UBS data reveals that China’s Humanoid Robotics Index has lagged behind the broader machinery index by roughly 9 percentage points year-to-date. This underperformance stems from delays in Optimus Gen 3 mass production, weak trading momentum, and capital shifting toward data centers and commercial aerospace.Upcoming CatalystsUBS highlights several milestones in the second half of the year capable of shifting market momentum:> The official mid-summer launch of Optimus Gen 3 (July–August).> Progress regarding Unitree’s IPO.> The World Artificial Intelligence Conference in Shanghai (July).> The World Robot Conference in Beijing (August).Nomura highlights a major paradigm shift in how systems are trained: data acquisition is migrating toward "robot-free" methodologies, such as teleoperation, Universal Manipulation Interface (UMI), and first-person perspective (Ego) collection. These alternative techniques cost only 20% of physical robot-based methods and operate at a much faster pace.As a hybrid training model consisting of 90% non-robotic data and 10% physical robot data becomes the industry norm, the demand for physical hardware dedicated to data collection will contract through 2026. Government entities remain the primary backers of these large-scale data collection hubs; establishing a single facility with a 1,000-unit capacity demands an investment of RMB 50–100 million and carries a 3-to-5-year payback period. While this reduces immediate hardware procurement pressure for OEMs, it elevates the demand for cross-platform standardization, data consistency, and high quality. Actual industrial integration still faces verification friction regarding cycle times, precision, and training costs.Contract Manufacturing vs. In-House Supply ChainsField research indicates a clear trend toward full-system contract manufacturing. Because hardware supply chains require heavy capital and feature long payback horizons, the majority of second- and third-tier OEMs are opting to outsource production. Over the long term, contract manufacturing's market share is expected to expand. Conversely, OEMs maintaining vertically integrated supply chains (such as Unitree Robotics) gain a direct pricing advantage by lowering their bill-of-materials costs.Entrants coming from automotive supply chain backgrounds hold a long-term competitive edge due to their large-scale assembly experience and end-to-end management capabilities. Meanwhile, 3C electronics manufacturers currently hold a minor advantage in brand equity.Nomura projects that mainstream, full-sized humanoid models will retail between RMB 150,000 and 300,000, while compact models will cost between RMB 10,000 and 100,000. Though prices have fallen by over 50% year-over-year in 2026, the rate of price deflation is projected to slow down in 2027.Global Ecosystem ExpansionsStrategic moves from major technology and automotive players are accelerating across the industry:NVIDIA & OpenAI: NVIDIA $NVIDIA(NVDA.US) is actively funding an ecosystem that includes Chinese startup Unitree and South Korean enterprises like Hyundai. Concurrently, OpenAI renewed its focus on the sector in June by forming an "OpenAI Robotics" unit, initiating aggressive recruitment for AI, systems, and hardware engineering talent.Corporate Financing & SPACs: Germany’s Neura Robotics secured a Series C funding round of up to USD 1.4 billion, aiming to manufacture 6,000 units this year and top 10,000 units annually by 2027. Agility Robotics announced its intention to go public via a merger with Churchill Capital Corp XI, establishing a pre-transaction valuation of USD 2.5 billion, with closure targeted for Q4 2026.Automotive Integration: In June 2026, XPeng’s CEO assumed direct leadership of the company’s robotics branch, aiming to mass-produce its "IRON" humanoid robot by the end of the year. BYD also confirmed its own humanoid development program, planning an internal factory deployment of up to 20,000 units by year-end—marking one of the largest operational rollouts globally.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.

Post your comment

No Comments