CICC: SiC to the left, GaN to the right—third-generation semiconductors emerge as the inevitable solution for high-voltage architectures in data centers

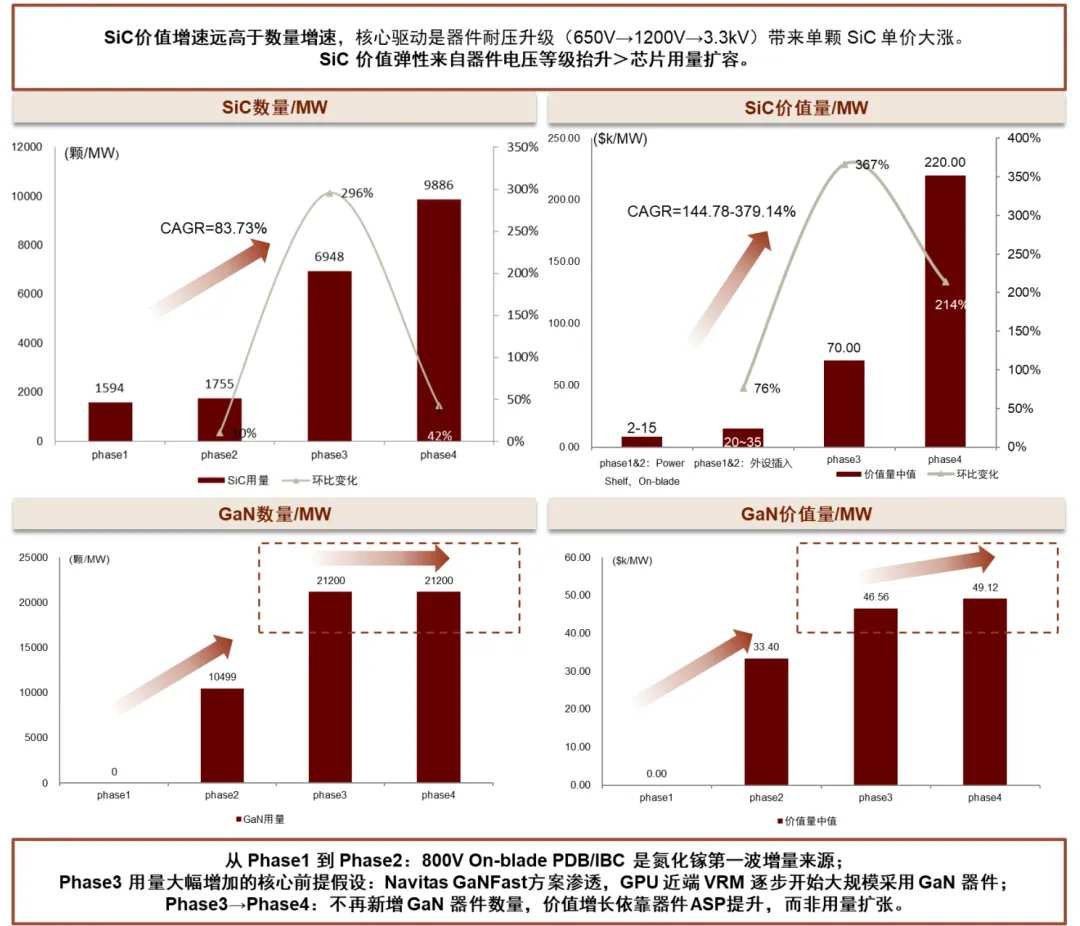

> Our estimates suggest that by 2030, a single MW of data center deployment could require approximately 10,000 SiC devices and 21,000 GaN devices, corresponding to per-MW values of $220,000 and $49,000, respectively—indicating considerable market opportunities.> Between 2026 and 2030, rack-side (white zone) and server-room-side (gray zone) systems are expected to be progressively upgraded to 800V/±400V DC configurations, thereby driving demand for third-generation compound semiconductors. In the short term (1–2 years), transitional architectures led by 800V sidecar units may offer limited upside for SiC demand. However, as the following developments materialize: (1) blade-level voltage step-down or even high-density 800V-to-6V power conversion at the rack side, (2) centralized rectification at the server room side, and (3) implementation of solid-state transformer (SST) solutions, we believe the long-term optionality of SiC/GaN-related companies warrants proper pricing.> We believe Chinese companies have already established deep positions in the SiC/GaN space, with continuously strengthening competitiveness. Going forward, Chinese firms across the third-generation compound semiconductor value chain stand to benefit substantially from the adoption of high-voltage data center architectures.> Legacy data center racks average around 7 kW. In comparison, NVIDIA’s Hopper architecture consumes ~40 kW, Blackwell GB300 NVL72 reaches 134–140 kW, Rubin will exceed 200 kW, and future architectures (Kyber in 2027 and Feynman in 2028) are projected to scale to 600 kW and over 1 MW per rack.The industry is projected to move through four transitional stages to implement 800V DC setups:Phase 1 (2026/2027): White Space Retrofit with "Sidecar"Setup: Gray space (facility level) remains untouched. A custom 800V DC side-mounted power cabinet ("Sidecar") is added next to the IT rack to rectify AC to 800V DC locally.Semiconductor Impact: SiC demand is concentrated in the sidecar's front-end rectification/PFC modules.SiC Volume: ~1,594 units per MW.Phase 2 (2027/2028): Native 800V DC Computing (The GaN Inflection Point)Setup: Centralized low-voltage UPS systems are phased out in favor of distributed rack-level battery backup units (BBUs) and supercapacitors. The 800V DC bus connects directly to the compute blade.Semiconductor Impact: GaN replaces a massive portion of SiC for the main onboard power step-down stage (Intermediate Bus Converters) to meet strict space and thermal restrictions near the GPU. However, SiC finds rigid demand in high-voltage hot-swap protection and Solid-State Circuit Breakers (SSCBs).Volume: ~1,755 SiC units per MW; ~10,303 to 10,667 GaN units per MW.Phase 3 (2028/2029): Centralized Rectifiers in the Gray SpaceSetup: Power rectification moves entirely upstream into the gray space. Massive facility-level centralized rectifiers convert grid power to an 800V DC injection backbone distributed throughout the facility.Navitas GaN Transformation (June 2026): Driven by Navitas' GaNFast integration into NVIDIA’s MGX ecosystem, setups will begin converting 800V directly to 6V, entirely eliminating the traditional 48V intermediate step-down bus.Volume: SiC surges to ~6,948 units per MW (driven by massive industrial DC distribution, BBUs, and energy storage systems). GaN usage explodes to 20,800–21,600 units per MW.Phase 4 (Post-2029): The Final Solid-State Transformer (SST) ArchitectureSetup: Both the low-voltage transformer and low-voltage rectification stages are completely eliminated. Megawatt-scale Solid-State Transformers (SSTs) directly convert medium-voltage grid AC to 800V DC.Semiconductor Impact: High-frequency SST operation relies heavily on high-voltage SiC. The gray zone infrastructure captures 54% of the total SiC value chain.SiC Volume: Skyrockets to ~9,886 units per MW.Market Value> As setups transition from Phase 1 to Phase 4, the hardware value of SiC per MW jumps drastically from $10,000–$25,000 to approximately $270,000. This value growth is primarily driven by voltage rating upgrades (moving from 650V to 1200V and 3.3kV devices).> GaN addressable market value grows from $33k–$33.8k/MW in Phase 2 to $46.5k–$49.1k/MW in Phases 3/4.Silicon Carbide (SiC) Unit CostsThe unit cost for SiC scales aggressively as devices move from standard rack components to high-voltage, high-density infrastructure:Non-SST / In-Rack Devices: $2.5 – $3.5 per unit.UPS / PDU / BESS Peripherals: $3.5 – $5.0 per unit.800V Transitional / Early SST Stages: $10.0 base price per unit (utilizing mass-production 1200V-class SiC MOSFETs).Full SST Architectures:1200V SiC Modules: $15.0 – $20.0 base price per unit.3.3kV SiC Modules: $50.0 base price per unit (reflecting the severe technical premium for medium-voltage direct conversion).Gallium Nitride (GaN) Unit CostsGaN pricing is stratified by application scenario, specifically focusing on its proximity to the high-voltage bus and the GPU itself:Phase 2 (On-Blade Intermediate Bus Converters / IBC):High-Voltage IBC (800V --> 50V): $3.8 per unit(utilizing 650V integrated GaN ICs).Low-Voltage IBC (50V --> 12V): $2.2 per unit (utilizing100V-class GaN chiplets).Phases 3/4 (Centralized & GPU-Proximate): Navitas PDB Board System: $3.2 per unit.GPU-Proximate Embedded GaN: $2.2 per unit (scaled AI server order pricing).The SiC Step-Function ExplosionSiC exhibits massive value elasticity, meaning the financial value grows significantly faster than the physical unit count due to the transition to higher-priced, higher-voltage (1200kV -->3.3kV) devices.Volume Growth: Scalings jump from 1,594 units/MW (Phase 1) to 9,886 units/MW (Phase 4), representing a strong ~83.73% CAGR.Value Growth: Financial capture skyrockets from $2,000 – $15,000/MW (Phase 1) to $220,000/MW (Phase 4). This represents a staggering value CAGR of 144.78% to 379.14%.The GaN High-Volume, Steady-Value CurveConversely, GaN follows a high-volume, highly localized deployment strategy. Its volume scales rapidly, but because it operates at lower, more commoditized voltage classes closer to the compute blade, its dollar-value growth is more linear.Volume Growth: Unit counts double from 10,303 – 10,667 units/MW (Phase 2) to 20,800 – 21,600 units/MW (Phases 3/4), a CAGR of 95% – 110%.Value Growth: Financial capture shifts from $33,000 – $33,800/MW to $46,560 – $49,120/MW, representing a more modest value CAGR of 38% – 49%.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.

Post your comment

No Comments