UBS: Memory

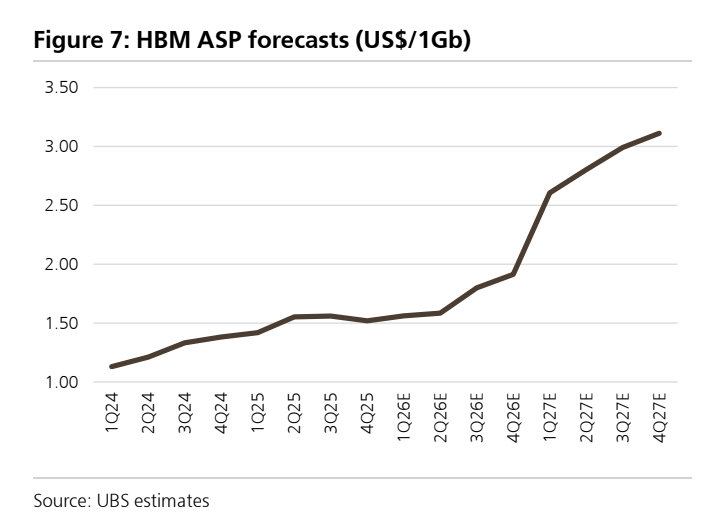

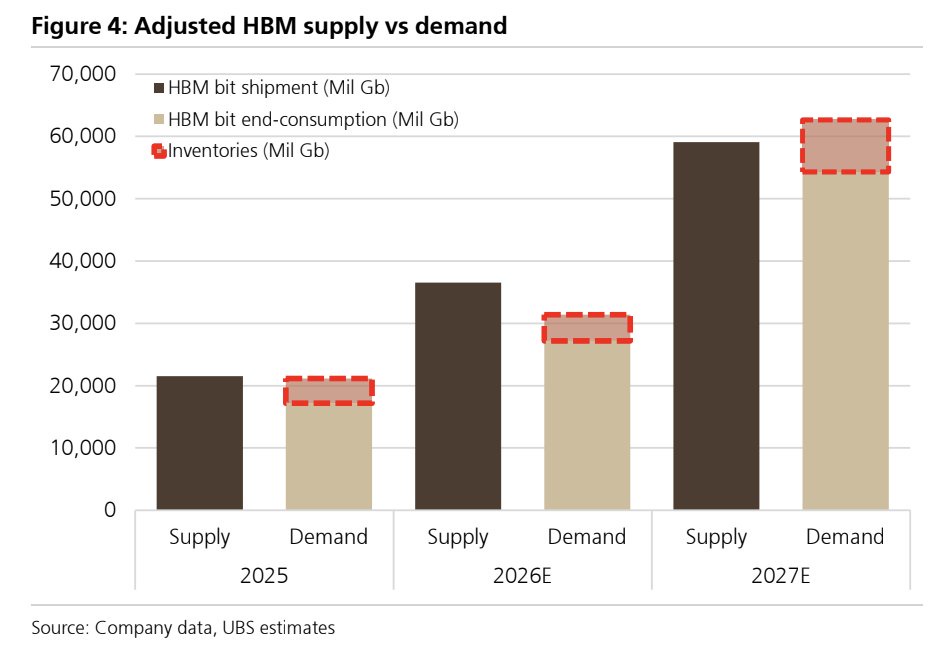

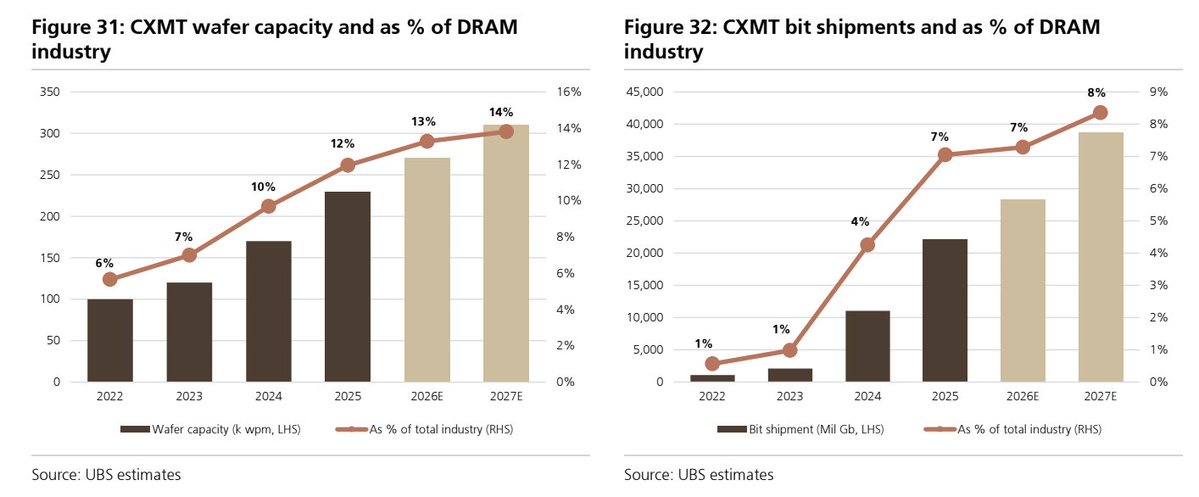

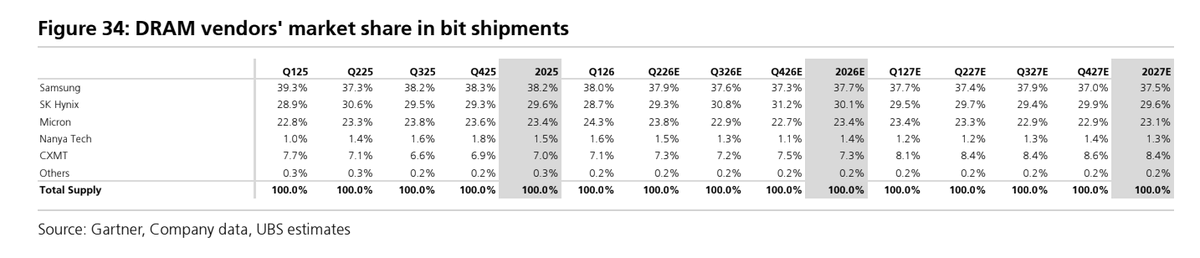

> HBM Forecast Lifted: The total HBM industry demand forecast was nudged upward to 33.1bn Gb in 2026 (+90% YoY) and 58.7bn Gb in 2027 (+77% YoY).> AI Accelerator Growth: This is driven by strong hardware procurement. UBS models HBM needs equivalent to 8.5 million Nvidia AI GPU units in 2026 (11.0 million in 2027), alongside upward revisions for Google TPUs (9.1 million units in 2027), AMD, and AWS.> DDR5 Focus: Suppliers are targeting 50–70% of DDR5 volumes to be tied up in these long-term agreements. Samsung expects to finalize revised LTAs with several major customers by 3Q26.> DDR Contract Pricing Raised: Baseline DDR contract prices are now expected to jump +32% QoQ in 3Q26 (up from the +17% previously forecasted) and +18% QoQ in 4Q26 (up from +12%). This follows a massive +67% QoQ surge in 2Q26.> Massive Structural Supply Deficit: Driven by "agentic AI" deployments, UBS forecasts a massive 17-percentage-point gap between DRAM supply (+19.3%) and demand (+36.2%) by 2027. Because of this, standard consumer electronics (like laptops, smartphones, and PCs) are facing a severe secondary memory shortage that will likely keep prices elevated through 2028.> A New Global Top 4 Player: According to UBS and recent market data, CXMT’s global DRAM revenue market share jumped to ~7.7% to 8% in early 2026. This is more than double its 3–4% share from 2025, solidifying its spot right behind the "Big Three" (Samsung at 38%, SK Hynix at 29%, and Micron at 22%).

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.

Post your comment

No Comments