Nio's Q1 2024 earnings report interpretation—Can't outcompete, can't slack off, this year relies on Ledao.

Last week, $NIO-SW(09866.HK) disclosed its Q1 2024 financial report. Overall, NIO's Q1 revenue was 9.91 billion yuan, down 7.1% year-over-year, with losses reaching 5.185 billion yuan. These figures were within expectations, as Q1 vehicle sales were already known. However, the overall gross margin was only 4.9%, lower than XPeng's, which was somewhat surprising. Additionally, the Q2 delivery guidance was worse than expected. After adjusting its battery leasing plan, NIO delivered over 20,000 new vehicles in May, a record high for a single month. But according to the delivery guidance, June deliveries are expected to decline again.

$NIO Inc(NIO.US) has been analyzed many times in previous earnings reports. Those interested can refer to earlier interpretations. Personally, I think NIO is currently in a state of "can't die from competition, but can't afford to slack off." After all, the high-end EV market has relatively few players, and NIO got an early start. The slow transformation of BBA (BMW, Benz, Audi) gave NIO an opportunity, and its strong financing capability has allowed it to invest heavily in services. As an owner, NIO's reputation is still decent. Below is a detailed look at the financial data.

1. Revenue

NIO's Q1 revenue was 9.91 billion yuan, down 7.2% year-over-year and 42.1% quarter-over-quarter. This was mainly due to a 3.2% decline in vehicle sales and a 6.2% drop in average selling price. NIO sold only 30,000 vehicles in Q1, with the ET5 accounting for a significant portion, which dragged down the average selling price.

2. Gross Margin

NIO's Q1 gross profit was 488 million yuan, with an overall gross margin of 4.9%, up 3.4% year-over-year. The automotive gross margin was 9.2%. While the gross margin improved compared to last year, it was still much lower than what the management had previously indicated. The earnings report attributed this to the higher proportion of low-margin ET5 models. During the earnings call, the management mentioned that Q2 gross margin would return to double digits, with further improvements in Q3 and Q4. I'm curious to see what the gross margin will be after the launch of the Onvo brand.

3. Losses

In Q1, NIO's net loss was 5.185 billion yuan, narrowing by 9.4% compared to Q1 2023. Last year, NIO lost over 20.7 billion yuan, while Li Auto earned over 10 billion yuan. This shows how slow NIO's path to reducing losses has been. Previously, William Li mentioned that NIO aimed to achieve breakeven in a single quarter in 2024, which is now almost impossible—it might not even happen by 2026. NIO's ability to sustain such prolonged losses without collapsing is largely due to its strong financing capabilities. For example, NIO Energy recently secured 1.5 billion yuan in funding from the Wuhan State-Owned Assets Supervision and Administration Commission.

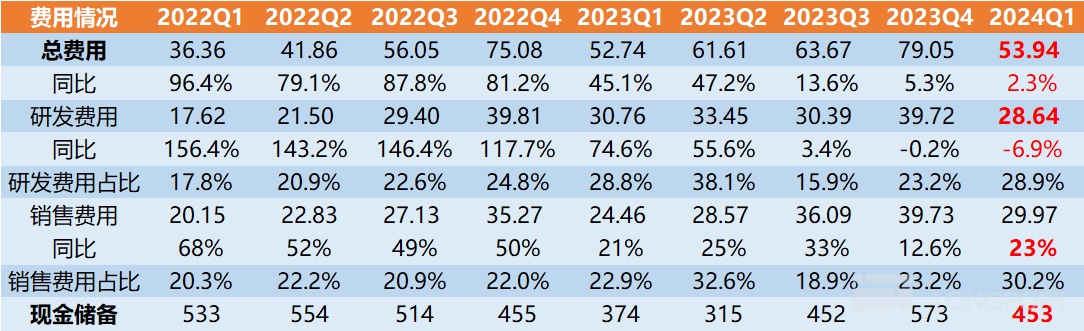

4. Expenses

In Q1, NIO's total expenses were 5.394 billion yuan, up 2.3% year-over-year. R&D expenses were 2.864 billion yuan, down 6.9% year-over-year and now lower than Li Auto's. Sales expenses were 2.997 billion yuan, up 23% year-over-year, indicating continued high growth in sales costs. Cash reserves decreased by 12 billion yuan in Q2.

It's clear that NIO's R&D expenses were once the highest among NIO, XPeng, and Li Auto, but now Li Auto has surpassed it. This highlights the importance of profitability for a company. With profits, R&D investments naturally increase, and competitive advantages expand.

5. Deliveries

This year, NIO adjusted its battery leasing policy, lowering monthly rental prices, which led to a noticeable increase in sales. However, based on the guidance, this momentum may not last long—similar to last year's price cut of 30,000 yuan, which only boosted sales for about two months.

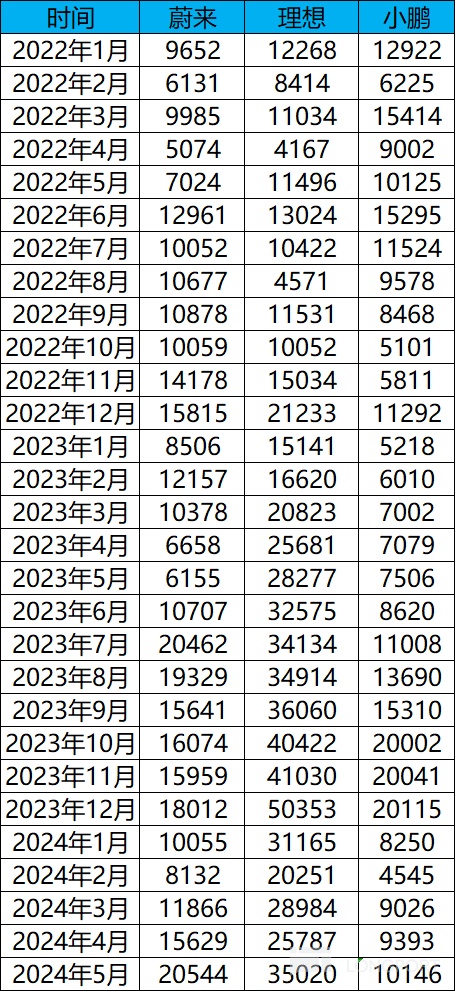

Attached: Monthly delivery data for NIO, XPeng, and Li Auto since 2022:

6. Q2 2024 Guidance

NIO's previous Q1 guidance was: vehicle deliveries between 31,000 and 33,000 units, down 0.1% to up 6.3% year-over-year; revenue between 10.499 and 11.087 billion yuan, down 1.71% to up 3.8% year-over-year. Actual deliveries were 30,053 units, and revenue was 9.91 billion yuan, missing the guidance entirely.

NIO expects Q2 vehicle deliveries to be between 54,000 and 56,000 units, up 129.6% to 138.1% year-over-year. Q2 revenue is expected to be between 16.587 and 17.135 billion yuan, up 89.1% to 95.3% year-over-year.

In April and May, NIO delivered 15,629 and 25,044 new energy vehicles, respectively, with May being a record high. Based on the guidance, June deliveries are expected to be around 17,827 to 19,827 units, a decline from May. After the battery leasing price cut in May, NIO's sales surged, but the guidance suggests this momentum won't continue into June, making it another disappointing outlook. However, given NIO's history of missing guidance, it's possible they deliberately set a conservative target this time.

II. Thoughts on NIO

NIO has always been controversial, especially among investors and owners. Even many Li Auto owners, after using NIO's charging stations multiple times, envy NIO's service and energy replenishment system. After all, Li Auto's energy network is far behind NIO's, which is likely why Li Auto isn't rushing into pure EVs yet.

But the EV industry itself is highly competitive, with new models launching almost every month. Manufacturer A holds a launch event, and Manufacturer B follows suit—completely different from the competition in the ICE era. From an investment perspective, the EV industry isn't a great one. If possible, avoid investing. Even if you do, finding alpha is much harder than in other industries, and the holding experience is worse. Investing in NIO comes with even greater volatility.

Returning to the company itself, NIO's focus this year is on its second brand, Onvo. NIO's existing models haven't seen major changes, so boosting sales relies on price cuts, including the BAAS plan. However, the effects of price cuts are usually short-lived. With the first half of the year just ending, NIO's chances of hitting its annual target with old models and price cuts are slim. Hope now rests on the new Onvo brand. The first Onvo model is positioned against the Model Y, essentially an entry-level SUV. I think the positioning is good, and the starting price of 210,000 yuan is quite affordable! Onvo's arrival brings a glimmer of hope to NIO's "can't die from competition, but can't afford to slack off" situation!

Attached: Historical NIO earnings report analyses:

NIO Q3 2024 Earnings Analysis—Is the Bottom Near?

NIO Q2 2024 Earnings Analysis—NIO's Future Still Seems Far

NIO Q1 2024 Earnings—Still Bottoming Out, Can the New ES6 Drive a Q3 Rebound?

NIO 2022 Q1 and Full-Year Earnings Analysis—Worst Times Over, Brighter Future Ahead?

NIO 2022 Q3 Earnings Analysis

Disclaimer: This article reflects personal views and does not constitute investment advice. Original content is hard work—your support through likes and follows is the best encouragement!

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.