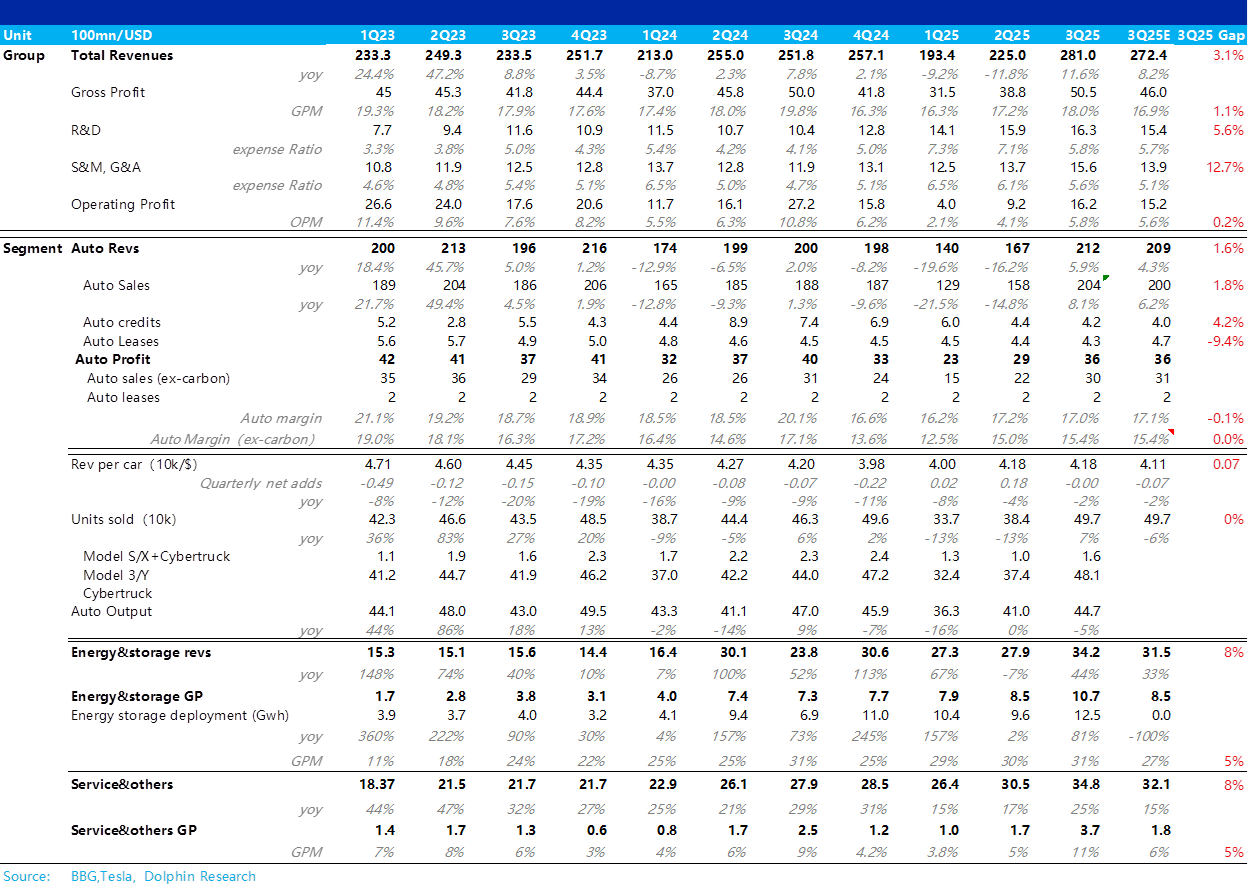

Tesla Quick Interpretation: Overall, regarding Tesla's third-quarter performance, the results are fairly decent. Both total revenue and total gross profit exceeded market expectations. However, net profit slightly fell short of expectations due to increased expenses.

From the perspective of the automotive business, which is the market's primary concern, Tesla's third-quarter vehicle sales revenue surpassed expectations. The core reason is that the market anticipated a quarter-on-quarter decline in Tesla's vehicle sales revenue, but the actual performance showed that the average selling price remained stable compared to the previous quarter.

Dolphin Research believes this is mainly due to Tesla raising the prices of Model S/X in the United States and launching the higher-priced Model L version in China, offsetting the discounts on inventory Model 3/Y vehicles and loan discount offers in various regions.

Regarding the most critical vehicle gross margin (excluding carbon credits), this quarter's vehicle gross margin improved quarter-on-quarter, aligning with market expectations. The quarter-on-quarter improvement in vehicle gross margin (excluding carbon credits) is attributed to the quarter-on-quarter increase in delivery volume, which released scale effects and reduced fixed per-unit amortized costs.

However, Tesla was still affected by over $400 million in tariffs this quarter, increasing the variable cost per vehicle. Ultimately, the automotive business gross margin was generally in line with expectations.

Since the second-quarter report, Tesla's stock price has reached a high of 439, which already reflects relatively full expectations for AI business and the upcoming mass production of Optimus. Therefore, compared to the third-quarter performance, the market is more concerned about the progress of Tesla's anticipated business.

In this earnings call, it was confirmed that the reduced configuration version of Model 3/Y has replaced the plan for the low-cost Model 2.5. Instead, Tesla is more focused on the mass production of the autonomous Cybercab (expected to start mass production in Q2 next year). Due to the U.S. IRA subsidies phasing out in the fourth quarter, U.S. demand will face significant pressure. Without the support of Model 2.5, the fundamentals of vehicle sales in the fourth quarter are expected to continue deteriorating.

Additionally, the release and mass production plan for the Optimus 3.0 prototype has been further delayed (Optimus P3 prototype release in Q1 2026, with mass production planning starting at the end of 2026), undoubtedly pouring cold water on the anticipated business. $Tesla(TSLA.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.