SPOT 2Q26 First Take: Q2 was mixed, with headline results broadly in line.

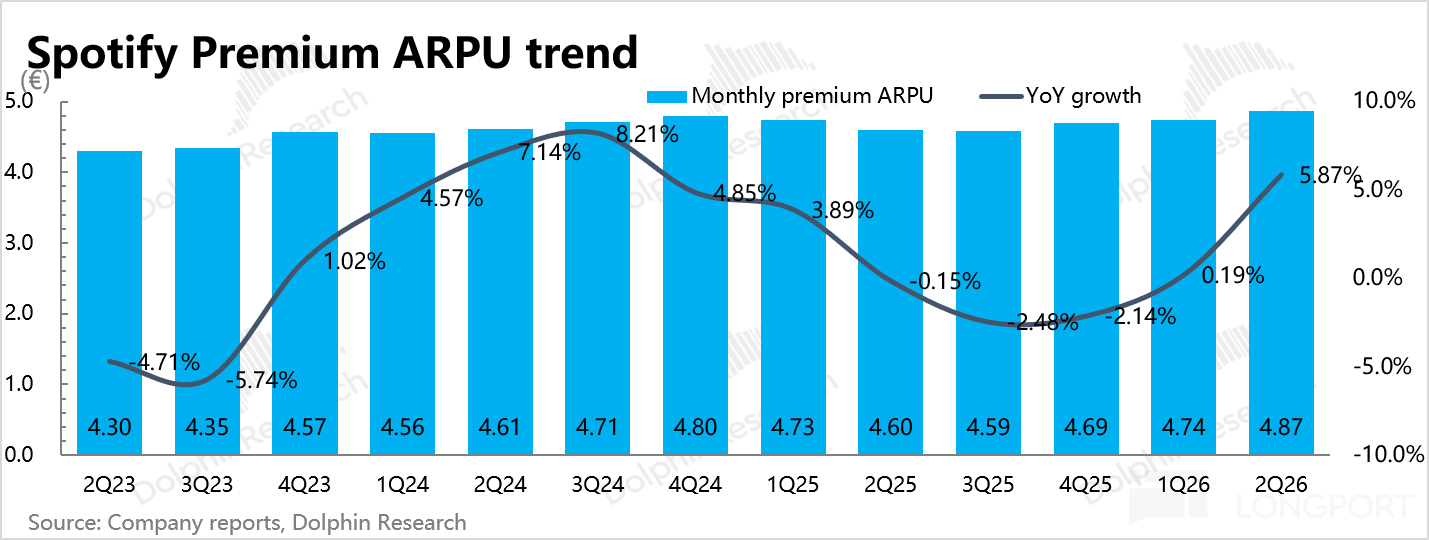

For Q3, guidance is better on revenue and monetization, but platform traffic and profitability look softer vs. expectations. Details below:(1) Price hikes are kicking in: Early-year increases in core US/EU markets started to flow through, with ARPPU up 6% YoY.

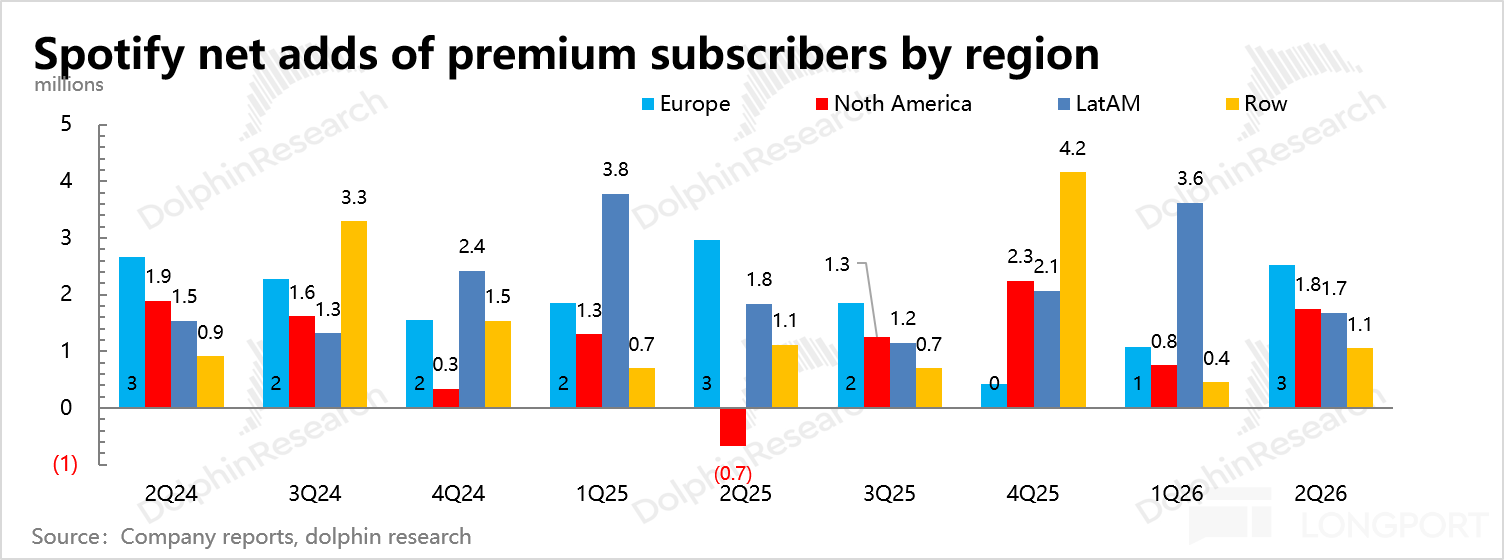

User pushback was milder than expected, as paid subs still rose by 7 mn in Q2. With both volume and price holding, subscription revenue grew 16%, accelerating QoQ vs. Q1.From Q3 guidance, the benign pricing lift should continue to support revenue.

The company guides for +6 mn paid subs, and Dolphin Research estimates ARPPU growth north of 7%.(2) Ads are stabilizing: Q2 ad revenue was 450 mn, up 1% YoY.

Trend-wise, further deterioration looks unlikely.On one hand, the FX headwind has rolled off, removing a passive drag.

On the other, the ad tech stack has been largely built out over the past ~18 months; as flagged at Investor Day, management will pursue a two-pronged approach of 'brand partnerships + automation', with double-digit growth expected in 2H.In addition, starting this year, ad revenue excludes portions not directly tied to advertising, such as podcast subscription bundles, which have been reclassified into subscriptions.

This creates a small classification gap and can skew directional reads for an ad line hovering around flat growth.(3) GPM is not keeping pace with pricing: Q2 GPM ticked up QoQ, with margin improvement in both subscriptions and ads.

The former benefited from pricing, while the latter delivered the main beat vs. guidance, consistent with progress in the ads business.However, management guides Q3 GPM down 30 bps QoQ.

We think this mainly reflects ad seasonality and subscription rev-share tied to the AI cover feature, which offsets more of the pricing uplift and caps margins.(4) Operating investment is steady: Q2 cost control remained focused on R&D, likely via headcount efficiency.

S&M grew at a low single-digit rate, mainly tied to late-Q2 product promos and anniversary events. Overall operating efficiency improved slightly, though new businesses and features require ongoing spend, limiting near-term room for further opex optimization.Overall, near-term catalysts are limited.

After the May 21 Investor Day and its long-term roadmap, sentiment is cooling as investors refocus on execution. Management is likely to provide more detail on near-term plans on the call; worth monitoring SPOT.