AAPL (Trans): New Siri to partner with Google; in-house R&D remains a priority

Dolphin Research summarized the key takeaways from AAPL FY2026 Q1 earnings call below. For our earnings read-through, cf. 'iPhone pops, Gemini assists — is Apple’s AI era finally here?'

I. Management highlights

1) Next-quarter guide: revenue to grow 13%-16% YoY, already reflecting iPhone supply constraints tied to advanced-node capacity at TSMC. Services growth rate to be similar to this quarter (+13.9% YoY). GPM guided at 48%-49%, which already factors in memory price increases.

2) Partnership with Google: the collaboration unlocks a broad set of experiences and enables key innovation. The company will keep running on-device and in private cloud, maintaining industry-leading privacy standards. No additional commercial details on the arrangement will be disclosed for now.

The company will continue select independent in-house R&D; that said, the upcoming personalized Siri is primarily powered by this Google partnership.

3) AI/cloud: both on-device and private cloud are critical, the dual approach underpins Apple’s differentiated privacy posture. On capacity, precise demand sizing is hard. Apple has acted to prepare capacity, either already in place or being deployed.

Big picture: Apple’s core franchise remains resilient. iPhone 17 is not a radical upgrade, but modest pricing concessions re-accelerated growth. Double-digit growth is back, yet legacy hardware alone is unlikely to deliver high structural growth. With AI in focus, investors will watch Apple’s progress on AI/Siri, and the Google Gemini tie-up should speed the new Siri launch cadence, potentially expanding the growth runway.

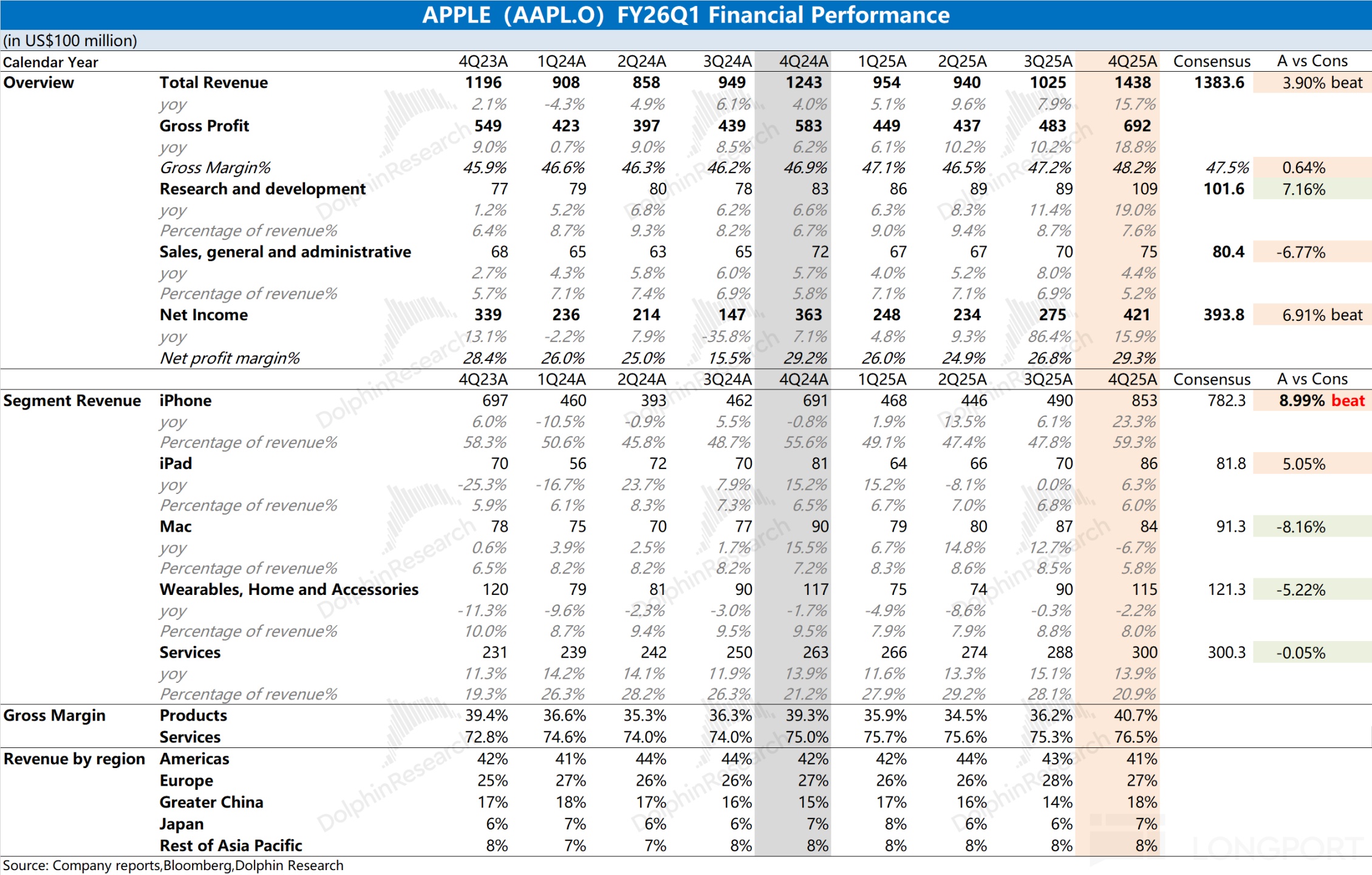

II. AAPL results snapshot

Overall:

Revenue was $143.8bn, up 16% YoY, a record high for the company.

Diluted EPS was $2.84, up 19% YoY, an all-time high. GPM reached 48.2%, above estimates; operating cash flow was $53.9bn, a record.

Net income was $42.1bn, also a record. Net cash stood at $54.0bn at quarter-end.

By segment:

iPhone revenue: $85.3bn, +23% YoY, a record.

Services revenue: $30.0bn, +14% YoY, a record.

Mac revenue: $8.4bn, -7% YoY, mainly on a tough base last year.

iPad revenue: $8.6bn, +6% YoY.

Wearables, Home & Accessories revenue: $11.5bn, -2% YoY, largely due to AirPods Pro 3 supply constraints.

III. Earnings call details

3.1 Prepared remarks

Product performance and updates:

- iPhone: upgraders hit record highs across many countries, with double-digit growth in new-to-iPhone users. Customer satisfaction remains exceptional at 99% in the U.S.

- Mac: installed base at a new high, with nearly half of buyers being new to Mac.

- iPad: revenue grew YoY, and upgraders reached a record.

Apple Intelligence (AI):

A large majority of eligible iPhone users actively use Apple Intelligence. Dozens of features are live (e.g., writing tools, cleanup tools), supporting 15 languages, with emphasis on personalization, privacy, and deep platform integration.

The company is working with Google to build the next-gen Apple foundation models, enabling more personalized intelligence over time.

Services:

- Ads, cloud, music, payments, App Store, and video all hit records.

- Apple TV delivered strong growth, with viewing up 36% YoY, award wins and nominations, and continued new shows and live sports (e.g., F1, MLS).

- Apple Music listeners and net adds hit all-time highs. Apple Pay helped partners cut fraud losses and expanded to more markets.

- App Store weekly Avg. users exceeded 850mn; since 2008, developer payouts surpassed $550bn.

- Rolling out new features, including digital IDs and more App Store search ad slots.

Enterprise and retail:

Enterprises are scaling Apple device deployments for productivity and security. Retail delivered a record quarter and continues to expand in markets like India, including a new Mumbai store.

Investments and commitments:

In the U.S., Apple committed $600bn over four years across advanced manufacturing, silicon, and AI, supporting nearly 500k jobs through the supply chain. Actions include a new Houston plant for servers; localized glass production with Corning; a supply-chain partnership with Micron targeting purchases of 20bn U.S.-made chips in 2025; and training in smart manufacturing and AI via the Detroit Apple Manufacturing Academy.

Capital returns:

Returned nearly $32bn to shareholders via dividends and buybacks. The BOD declared a cash dividend of $0.26 per share.

Outlook (Mar quarter):

- Total revenue to grow 13%-16% YoY, including iPhone supply constraints.

- Services growth rate to be similar to the Dec quarter.

- GPM of 48%-49% (including memory cost inflation).

- Opex of $18.4bn-$18.7bn.

- Tax rate around 17.5%.

3.2 Q&A

Q: With higher Mar-quarter GPM guidance, how do memory costs factor in? Are you confident in supply, and how do rising memory costs flow through the model?

A: Demand for the latest iPhones far exceeded expectations, leaving channel inventories very tight exiting the Dec quarter. We are in a catch-up supply mode and remain constrained, with timing of supply-demand balance hard to predict. The constraint is mainly advanced-node supply for our SoC (TSMC capacity).

Memory had a minimal impact on Q1 (Dec) GPM. We expect a larger impact in Q2 (Mar), already included in the 48%-49% GPM outlook. Beyond Q2, memory prices continue to rise significantly. As always, we will consider a range of mitigation options.

Q: What drove China’s strong results (near record revenue), and how sustainable is this into the Dec quarter?

A: Greater China grew 38% YoY, led by iPhone, setting a revenue record. This reflects strong enthusiasm for the iPhone 17 family. We saw strong double-digit YoY growth in foot traffic at our China retail stores. Installed base hit record highs in Greater China and the mainland, with record upgraders and double-digit growth in new-to-Apple users.

Surveys show iPhone ranked top-three among smartphones in urban China, driven by product strength and positive customer response. For non-iPhone, the majority of Mac, iPad, and Watch buyers were new customers, which is encouraging.

The same surveys indicate iPad was the best-selling tablet in urban China. MacBook Air was the best-selling notebook in the Dec quarter, and Mac mini was the best-selling desktop. Overall, it was an outstanding quarter in China.

Q: On AI, what are the incremental costs and monetization opportunities? Peers are integrating AI on-device, but revenue uplift is unclear. How will Apple monetize AI, and what is the ROI timeline?

A: We are infusing intelligence into more of what users love, deeply integrating it into the OS in a personalized and private way. This creates substantial value and opens broad opportunities across products and services. We are very pleased with the Google partnership.

Q: From current data, what are the main drivers of iPhone strength, and are they sustainable?

A: Drivers vary by customer segment. Success typically comes from a combination: display, cameras, performance, the new selfie camera, and design. The design resonates strongly. Together these factors delivered a powerful cycle, evident in our Dec-quarter results.

Q: For the 13%-16% YoY revenue guide for Mar, are there notable base effects across products, such as last year’s MacBook Air with M4 or iPhone 16E complicating comps?

A: Nothing specific to call out on base effects. We previously noted tough comps for Mac, but not in this guide. This is largely a continuation of a strong cycle, albeit impacted by the supply constraints mentioned earlier.

Q: Ads were strong within Services. Any new ad opportunities, especially the new App Store ad slots, and plans to expand ads to Maps or TV?

A: Services strength was broad-based, with records in ads, music, payments, and cloud. We continue to add services, including digital IDs in Wallet and the additional App Store search ad slots you mentioned, which offer more ways for advertisers to be discovered. Our active device base reached 2.5bn, creating exciting opportunities for Services.

Q: How was the Google decision on AI and Siri made? Is there revenue sharing like search?

A: We determined Google’s AI tech provides the strongest foundation for Apple’s models. We believe the collaboration unlocks many experiences and enables key innovation. We will continue to run on-device and in private cloud, maintaining industry-leading privacy. We are not disclosing commercial details.

Q: How can GPM be 48%-49% with DRAM/NAND rising? Is it mix shifting to higher-margin Services?

A: Dec-quarter GPM was 48.2%, up 100bps QoQ, driven by favorable product mix. A strong iPhone cycle delivered better mix and scale, lifting product GPM by 450bps QoQ. Services kept growing double digits and also contributed meaningfully.

On guidance, the range is similar to Dec. There are puts and takes: Services retain structural tailwinds from Q1 to Q2, but seasonality in hardware post-holiday offsets that. We are confident in the 48%-49% GPM guide.

Q: How do you view overall smartphone demand, given memory pricing and other OEMs/suppliers signaling component constraints and softer demand? What does this mean for iPhone demand through the rest of the year?

A: On supply, we face constraints in Q2 (Mar), which are embedded in the revenue guide. The constraint is advanced-node capacity. This follows the 23% growth in Q1 (Dec) and reduced supply-chain flexibility, limiting how fast we can ramp. We are not commenting on supply beyond Q2.

On memory pricing, we already commented. On demand, based on what we see, we gained share in the Dec quarter, given the market did not grow 23% overall. We are pleased with that, but we will not predict the market’s next move.

Q: You mentioned a range of options to address the memory market. How should we think about long-term supply agreements vs. spot?

A: We have multiple operational levers available. It is too early to size their impact, but we do have options to consider.

Q: Third-party data suggest App Store growth may have slowed to ~7% in Dec, while Services overall grew 14%. Can you confirm, and what drove the gap? Any actions to re-accelerate?

A: App Store set a quarterly record in Dec. We do not break out performance by individual service. Broadly, we saw growth across all service categories and regions, with both developed and emerging markets setting records and growing double digits. We typically do not provide more granularity.

Q: Given unprecedented memory volatility, would pricing changes be an option beyond other mitigations?

A: No comment.

Q: Capex slowed vs. last quarter. Does the Google collaboration on Gemini and next-gen Apple models change your intent to run workloads on Apple private cloud, or alter near-term plans?

A: We will not discuss deal specifics with Google. On capex, we operate a hybrid model, so capex can fluctuate independent of volume. It spans equipment, facilities, retail stores, data centers, and more.

For production equipment and data centers, we use a hybrid approach, combining owned and third-party resources. Hence it is hard to infer specifics from capex alone. Capex will ebb and flow. We built out private cloud last year, and related capex is reflected in Dec-quarter results.

Q: You cited product mix as a driver of product GPM. Any notable mix differences between iPhone 17 and iPhone 16? Also, did tariffs help, and what do you expect for next quarter?

A: For overall product GPM, we saw favorable mix and scale effects. Given the current strong iPhone cycle, those benefits may be higher than in other cycles. Also, in Q1 (Dec), new product cost structures typically play a role.

From Q4 to Q1, favorable mix and scale provided a larger offset than usual. For tariffs, we had estimated about $1.4bn headwind in Dec, and the outcome landed roughly in that range.

Q: How do Apple’s foundation models differ from third-party models like Gemini? Does Apple’s model become a distinct layer in the AI stack, and how should we think about collaboration with frontier models?

A: It is a partnership, and we will also continue some independent in-house development. To be clear, the upcoming personalized Siri is primarily driven by the Google collaboration. That is the core enabler.

Q: With memory constraints affecting smartphones and PCs, and Apple’s relative buying power, is this a chance to take share from competitors with tougher access to memory, lifting iPhone and Mac share?

A: We believe iPhone gained share in the Dec quarter. Looking at the 2025 calendar year, Mac also gained share. We are pleased with our market position.

Q: Some compare the iPhone 17 upgrade cycle to 2020-21 (iPhone 12/13 upgrades). Do you agree, and how is Apple Intelligence impacting upgrade rates?

A: Each iPhone cycle is unique, so we avoid comparing to specific cycles. The iPhone 17 family is its own product and we are pleased with it. With a large and diverse installed base, the lineup resonates across segments. We see strong demand from users on older devices and those on newer iPhones alike.

Q: Why are there constraints in advanced packaging, given your usual allocation at major foundries? How long will this limit shipments against true demand?

A: When demand is unmet, it is hard to estimate true demand, and we would not share our internal estimates. To be precise, the constraint is advanced-node capacity at 3nm, which builds our latest SoC. That is what limits Q2 supply. It follows the 23% growth in Q1, far above our internal plan, which reduced supply-chain flexibility for a period. We will not estimate when supply and demand will balance.

Q: How attractive is India for iPhone, and how do you view the opportunity given the large installed base?

A: We set a quarterly revenue record in India in Dec. Specifically, iPhone, Mac, and iPad all reached quarterly records, and Services hit an all-time high. India is the second-largest smartphone market and the fourth-largest PC market globally.

Despite a solid growth track record, our share remains relatively small, so the opportunity is substantial and exciting. The majority of iPhone, Mac, iPad, and Watch buyers were new to the product, underscoring the potential. Our installed base in India grew strongly at a double-digit rate, which is very encouraging.

Q: You have deepened in-house silicon this cycle. Should this be seen as an underappreciated support for margins, and how do you view future opportunities in custom chips?

A: Apple silicon has been an incredible innovation for us, starting with iPhone, then iPad, and in recent years Mac. We view it as a breakthrough and a major competitive advantage. Beyond cost and margin opportunities, it delivers critical product differentiation and greater control of the roadmap. Strategically this is very important, and we also see core tech investments positively impacting margins.

Q: Will Apple prioritize edge/on-device AI or cloud services, and do you have sufficient DC capacity to support broad Siri adoption given you have not ramped capex like other hyperscalers?

A: Both on-device and private cloud are essential; it is not either-or. This dual approach differentiates our privacy-focused architecture. On capacity, demand sizing is difficult, but we have prepared as best we can, with capacity either in place or being deployed.

Q: Active devices are 2.5bn, but Apple Intelligence starts with iPhone 15 Pro. Roughly what share of iPhone or total active devices is AI-capable, and does this make the rollout more gradual?

A: We are not providing that number. As you would expect, the figure is growing within our installed base. We are encouraged by the number of devices with this capability, but will not quantify today.

Risk disclosure and statement: Dolphin Research disclaimer and general disclosures